This analysis is for information and educational purposes only and is not intended to be read as investment advice. Please click here to read our full disclaimer.

An extended fuel crisis could, in theory, provide the economic incentive for coalminers to transition away from diesel use. Higher diesel prices for 6–12 months would raise open-cut coalmine unit costs by more than they receive in diesel subsidies.

Until now, the incentive to retain diesel has been stark. Australia’s major coalminers received an estimated AU$1.27 billion in Diesel Fuel Tax Credits in FY2024–25 — a rebate on off-road diesel use. That year, their open-cut mines paid a combined AU$24 million in Safeguard Mechanism carbon costs. Per tonne of coal, that is AU$5.15 in diesel subsidies for every AU$0.14 in carbon penalty — a ratio of 37:1.

Some miners have recently disclosed the impact of elevated diesel prices in their Q1 2026 financial results. Whitehaven has reported its unit costs increase by about AU$10-11/t for every AU$1/litre increase over a year. Coronado’s Curragh mine uses 10 million litres a month or 120 million litres a year. For each dollar per litre increase in diesel, its monthly fuel bill has risen by AU$10m. On production of 10 million tonnes a year (MTPA), the annual cost impact is about AU$12/t. The fuel crisis is miners’ strongest financial incentive to move away from diesel. But strong barriers — capital cycle timelines, mine life alignment, lack of pilot trials — mean that incentive alone is unlikely to trigger rapid structural change.

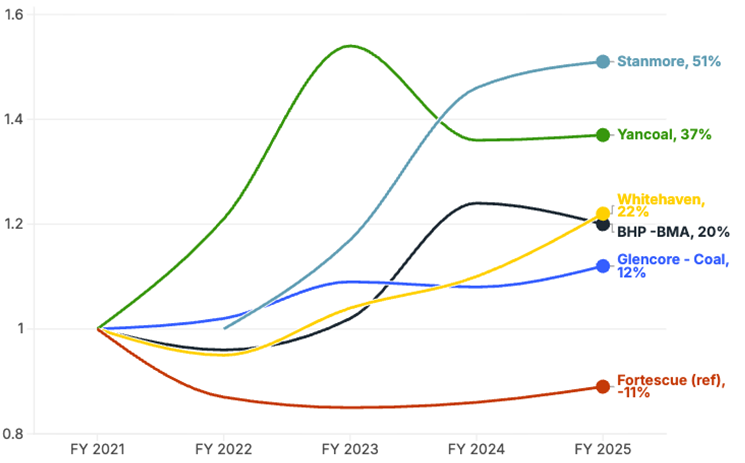

Every major Australian coalmining company is burning more fuel per tonne of coal produced. Since FY2020–21, fuel costs at BHP’s BMA operations have risen by 20%, Whitehaven’s by 22%, Glencore’s coal division by 12–14% and Yancoal’s by 37%. Since FY2021–22, Stanmore’s fuel costs have ballooned by 51%.

Mines are burning more fuel and producing less. Coalmining uses more diesel than all of agriculture, construction or the passenger diesel fleet, accounting for an estimated 3.9bn litres (151.4 petajoules/PJ) in FY2023-24.

The Safeguard Mechanism is designed to put a price on diesel combustion emissions, among other sources, and steer them on a downward trajectory. For coalmine diesel, the data suggests it isn’t working.

The Safeguard Mechanism: a 14¢ per tonne signal

The Safeguard Mechanism appears well designed, with baseline annual emissions intensity limits set to decline at 4.9% a year. For most open-cut mines, in practice, these baselines barely change — Safeguard data showed open-cut baseline emissions intensity increased by 1.3% in FY2024-25.

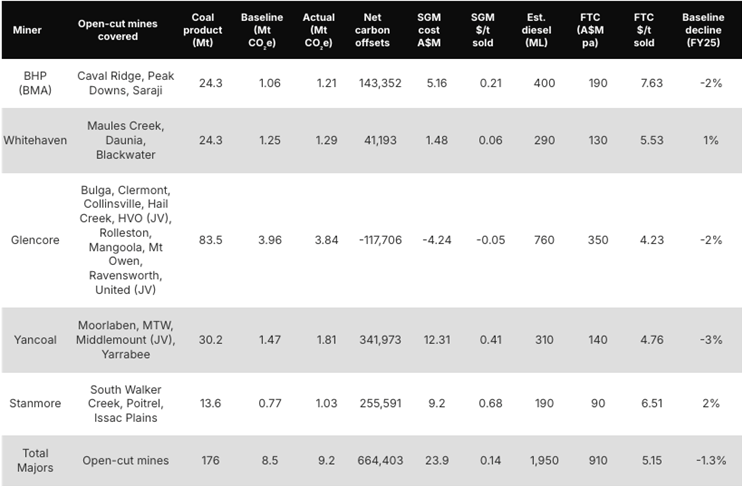

Across the major miners listed, about 176MTPA of open-cut coalmine production is covered by the Safeguard Mechanism (Table 1).

- Diesel accounts for about 60% of Scope 1 (direct) emissions from these operations.

- These mines exceeded Safeguard emissions baselines by an aggregate 664,000t of CO₂.

- Emissions increased by 1.4% in FY2024–25 against an increase in baseline intensity of 1.3%.

- The cost of compliance was AU$24m — or AU$0.14/t of coal produced.

- They consumed approximately 2bn litres of diesel. The cost of Safeguard compliance was 1.2¢/l — more than 40 times less than the 52¢/l diesel rebate.

- With baselines relatively flat, even if the cost of carbon offsets rose to AU$100/t, the Safeguard penalty would remain an order of magnitude lower than the Fuel Tax Credit (FTC).

Table 1: Safeguard Mechanism data for open-cut mines, FY2024–25

Sources: Clean Energy Regulator, IEEFA estimates. Notes: Australian Carbon Credit Unit costs assumed at AU$36/t. Baseline decline rate per baseline emissions intensity rates FY2024 to FY2025.

The incentive mismatch — a $5.15 credit against a $0.14 penalty — leaves miners with little reason to act. The Safeguard penalty is a mere rounding error against the diesel subsidy. The cost of diesel increases in the fuel crisis is of far greater magnitude for miners.

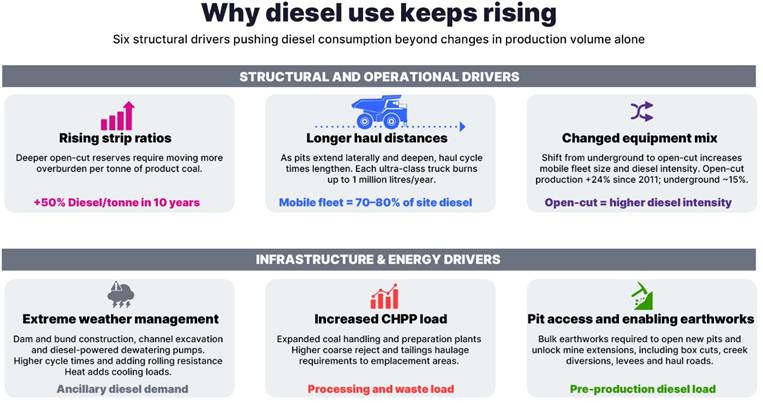

Coalmining’s diesel intensity problem

Diesel consumption per tonne of production across Australia’s major coalminers has been rising since FY2020–21. This contrasts with iron ore miner Fortescue, which is reducing it (Figure 1). What Fortescue demonstrates is that large-scale mining fleet decarbonisation is achievable; what it does not show is whether coalminers are as technically prepared.

Rising fuel intensity in coalmining stems from the prevalence of open-cut mining. This form of mining accounted for 84% of production in FY2024–25. At open-pit mines, the primary driver of this rise is increasing geological strip ratios — the volumes of dirt and rock removed to reach coal seams — as mines grow deeper and more extensive.

Figure 1: Miners’ indexed fuel intensity (base year FY2020–21)

Sources: Company sustainability reports, compiled from underlying ESG data. Notes: Fuel consumption intensity = gigajoules of fuel per run-of-mine tonne of coal produced. Glencore’s measure is energy intensity per tonne of copper equivalent (CuEq), from CY2022–24.

Secondary drivers emerge when individual miners are examined. For example, at Stanmore, strip ratios alone do not account for the rise in fuel intensity. Strip ratio increases also result in higher material transportation distances. The structural direction of fleet change at some open-cut coalmines runs the opposite way from electrification. As mines have matured, operators have replaced electric dragline diggers with more mobile truck and shovel operations, which consume more diesel. Introduction of electric shovels and excavators remain a near-term diesel reduction opportunity. (For more detail on individual miners’ fuel intensity see the Appendix.)

Extreme weather is another driver, with flooding affecting many mines. Wet weather has directly resulted in additional diesel-powered earthmoving — to build dams and drains — and pump out flooded pits. Indirectly, wet weather can slow mobile equipment, increasing cycle times and adding rolling resistance. Extreme heat also affects engine performance and adds to fan cooling loads. The East Coast Cluster climate change outlook report warns of higher temperatures and intensity of heavy rainfall events ahead.

Fuel efficiency measures

Miners have been focused on operational fuel efficiency measures. For instance, Yancoal noted several initiatives in its P4 Sustainability Report 2025, such as:

- At Moolarben, a new excavator with a 10% improvement in fuel efficiency was introduced in 2025; three older excavators were also replaced with more fuel‑efficient models.

- At Mount Thorley Warkworth, 10 new trucks, designed to reduce fuel consumption by about 5% compared with existing models, were delivered in FY2024–25.

- Fuel-calibration optimisation continued during 2025, following trials in 2024 that achieved a 2% reduction in fuel burn.

- Other initiatives, such as improved cooling fan performance and tyre-pressure monitoring, are aimed at reducing fuel consumption.

The emphasis is on optimising diesel, not replacing it. These initiatives may deliver short-term gains, or limit the increases, but lock miners into diesel for years to come.

Coalminers have been slow to adopt plans to curb rising diesel intensity, compared with some other sectors. Hunter Valley Operations (HVO) has focused on improving fuel efficiency, including: “operational control efficiencies such as minimising haul distances, optimising ramp gradients, payload management and scheduling activities to optimise equipment use”. Some miners are looking to AI and smart energy management systems to optimise energy consumption. Others have moved to autonomous vehicles to minimise operator variability. Meanwhile, Fortescue has embraced the decarbonisation opportunity by investing in electrification — a CEO-level commitment with no equivalent in the coal sector.

Fuel efficiency initiatives may limit diesel use but the trends are still heading in the wrong direction. While efficiency gains may offset some consumption, geology is working against them: more material must be moved as pits deepen, and haulage distances grow, increasing the diesel used per tonne of coal produced.

A number of mines have trialled or considered alternative fuels, such as biofuels including hydrotreated vegetable oil (HVO). Others have considered, gas-hybridisation — where on-site methane is harnessed as an energy source to power haul trucks.

Coalmining is a growing contributor to Australia’s diesel use. The fuel crisis provides the clearest economic incentive yet to move away from diesel. But incentive and capability are different things. An extended fuel shortage, with material increases to miners’ unit costs that exceed the Fuel Tax Credit benefits, may accelerate the strategic conversation or trigger electrification and alternative fuel trials. Otherwise, rising strip ratios and other structural factors will continue to lock in high fuel intensity rates through 2030 and beyond.