The Media and Entertainment (M&E) sector in India experiences a fundamental change that moves away from traditional broadcasting methods toward modern platforms that provide viewers with on-demand content. Over many years, television set out the norms that governed the distribution of the content, its monetization, and the manner in which the television program would be watched. Indian over-the-top (OTT) providers are creating new definitions when it comes to the production, distribution, consumption, and monetization of content. The shift reflects significant changes in digital ecosystems, evolving consumer preferences, and technological advancements.

The industry is evolving rapidly, moving away from traditional scale-led broadcasting models towards digitally enabled, data-driven, and personalised distribution ecosystems. The focus has shifted to delivering tailored content experiences that align with evolving consumer preferences.

Strategic Impact of the Television-to-Streaming Shift

The shift from television to streaming is crucial for finances and strategic planning. The shift from traditional television to streaming platforms is driven by key factors as mentioned below.

Primarily, sources of revenue are changing. According to PwC India’s Entertainment & Media Outlook 2024–28, digital advertising and online video are among the fastest-growing segments of the industry. Consequently, they are weakening television’s traditional stronghold while altering how revenue is generated across media.

Secondly, the economics of content are evolving. As opposed to conventional TV where advertising forms the main source of revenue, the streaming platforms base their economic considerations on user data.

The KPMG Digital First Journey report shows that OTT platforms need a different approach to digital technology. Broadcasters require both data analysis skills and appropriate technology stacks to implement their operations. Streaming services have created fewer restrictions which enable content to reach wider audiences. Regional and independent creators no longer need to rely on traditional TV broadcasters to distribute content widely.

Market Outlook & Industry Overview

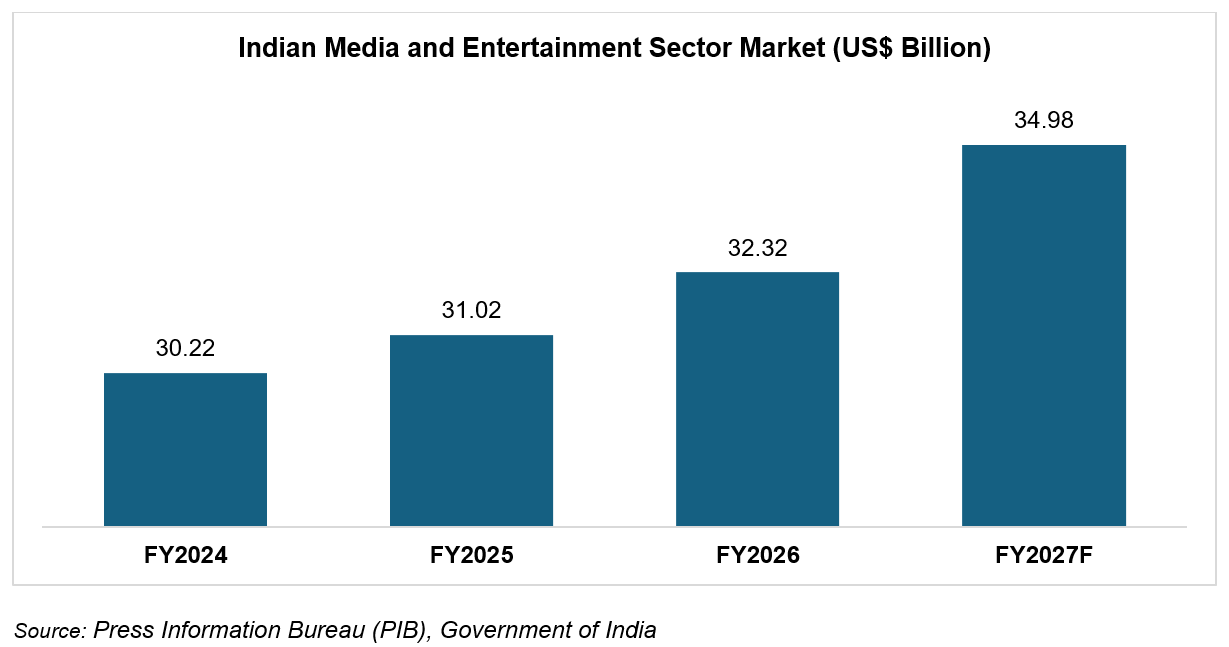

India’s media and entertainment (M&E) sector stands as the fifth largest worldwide which reaches a market value of US$ 30.22 billion (Rs. 2,50,200 crore) in FY24 and is expected to grow at a compound annual growth rate of 7% until it reaches around US$ 35 billion (Rs. 3,06,700 crore) in FY27 through ongoing structural development.

The growth of digital media is primarily driven by increasing smartphone adoption and the availability of affordable data plans for streaming content. OTT services are now used across all age groups; however, younger, mobile-first users represent the largest customer segment.

Scale economics, sports rights, and monetisation sustainability are changing the competitive dynamics, with platforms adopting a hybrid subscription–advertising model.

Television maintains its dominant status because it reaches more viewers than any other medium, especially in rural and semi-urban regions. The growth parameters for the M&E sector get enhanced with the advent of online gaming and advertisements, thus placing India among the fastest growing M&E markets globally.

Digital infrastructure and Regulatory Policy Framework

The development of India’s digital media sector started through policy initiatives which created essential Infrastructure while providing support for monetisation and establishing formal governance structures for over-the-top streaming services.

The Digital India initiative has accelerated broadband penetration and digital inclusion across the entire country. The BharatNet project delivers high-speed fibre connectivity to remote villages through its network which extends internet access to areas outside of major cities thus increasing potential viewers and users for video streaming services and over-the-top platforms.

India’s digital payments architecture has further strengthened monetisation pathways. The Unified Payments Interface (UPI), part of India Stack, now processes over 64 crore transactions daily, accounting for more than half of India’s digital payments. The payment system enables streaming platforms to handle subscription billing and recurring payments and hybrid revenue models without any operational disruptions.

The Information Technology (Intermediary Guidelines and Digital Media Ethics Code) Rules, 2021, framed by the government under section 87 of the Information Technology Act 2000, provided for guidelines that govern digital media and OTT platforms. These rules provide for the regulation of content classification norms, redressal of grievances and due diligence under a light-handed approach of self-regulation.

India’s streaming industry now benefits from three essential factors which include infrastructure growth, advancements in digital payment systems and clear regulatory frameworks.

Key Growth Drivers Shaping India’s Media Evolution

The Road Ahead

The shift from TV to streaming in India has entered the stage of consolidation, where the importance of scale and viable business models are becoming significant in terms of competitiveness. According to the PwC India Entertainment & Media Outlook 2024-28, profitability would be based on efficient monetization models, a greater regional footprint, and the effectiveness of digital advertising measurements. However, there are certain structural hurdles, such as piracy, absence of standardized metrics, and regulatory compliance. In the long run, there would be no clear difference between the TV and digital sectors as broadcast channels go digital and streaming platforms transform into media groups.

FAQs

Is streaming replacing television in India?

No. Television retains a strong reach, particularly in rural and mass segments. However, streaming is capturing younger and digitally native audiences, leading to coexistence and convergence.

What is the biggest driver of OTT growth in India?

Affordable mobile data, smartphone penetration and regional content investments are primary drivers.

How are platforms monetising in a price-sensitive market?

Through hybrid Advertising Video on Demand (AVOD)– Subscription Video on Demand (SVOD) models, telecom bundling and advertising-supported tiers.

Why is regional content critical?

Most new internet users prefer vernacular languages, making localisation essential for growth.

What are the main risks facing streaming platforms?

Piracy, digital ad fraud, measurement challenges and high content acquisition costs.