Germany has spent more than half a decade talking about its need to de-risk from China’s economy. Since 2023, this has been its official policy.

Meanwhile, numerous German companies have been expanding their operations in China’s market, while remaining heavily reliant on Chinese suppliers. Even where a company’s share of revenue from China has declined compared to other markets, their absolute exposure has often increased, such as in automotive manufacturing and semiconductor equipment.

The de-risking implementation gap is widely acknowledged in Germany. A lack of strategic action and resource constraints are mostly cited as its causes — the argument being that factors such as administrative lethargy, and a mismatch between the costs and benefits of de-risking, have caused a gap between knowledge and action.

But what if an outdated analysis is part of what is holding back Germany‘s de-risking efforts?

Failure to update our understanding of the China challenge to accurately represent Beijing‘s current economic ambitions will make diversification even harder than it already is. Germany’s de-risking strategy was based upon an understanding of risk as an overconcentration of dependencies in specific areas of the industrial supply chain.

Yet this analysis reflects the operating environment of a decade ago — the situation international companies faced when they entered into the Chinese market during the previous “golden era” of bilateral economic relations. German companies at the time saw China as a place to procure or assemble, while they retained the flanks of their production process — IP, design and high-margin services — back home.

Sourcing or producing in China was a way to increase margins. The resulting dependencies, though significant, were fairly limited in scope. They affected individual companies, which could, in theory, buy or produce elsewhere — it mainly being a question of cost and of access to the Chinese market.

During the past two years I have been representing German industry in Beijing, visitors from Germany of various backgrounds and political stripes have asked me a version of the same question: Why do German companies remain so engaged in this market?

It is a fair question. We at BDI, the German Industry Federation, regularly join the broader community of China analysts in highlighting the increasingly challenging operating environment for foreign companies. Last year, considerable effort was expended helping companies navigate the disruptive impact of China’s export controls. This year, new supply chain measures illustrate the increasing regulatory pressure companies face.

…the competitive overlap between foreign and Chinese companies is no longer confined to low-margin manufacturing, but extends into the high-margin, high-control parts of the value chain.

Meanwhile China’s previous double-digit growth has given way to an ongoing real estate crisis and below-average levels of domestic consumption. Critics point out that, given this backdrop, it should only be a matter of time before boardrooms back home reassess the China risk and perhaps even strategize their retreat.

The reality is quite different. Rather than prompting exit, the above-described pressures seem to have paradoxically pushed firms toward deeper localization, with more research, development, production, and decision-making moving into China.

A growing share of German subsidiaries now operates with substantial autonomy from headquarters, extending well beyond sales or sourcing. In sectors such as automotive technology, partnerships with Chinese firms increasingly reach into core areas such as software, chips, and systems architecture. In some cases, German firms are no longer the dominant technological partner.

The missing puzzle piece to this discrepancy is competitiveness.

The several thousand German companies in China that plan to maintain, if not double down on, their investments are no longer doing so purely for the benefits of manufacturing scale. Increasingly, their engagement reflects the growing competitiveness of domestic players. The old division of labor — “China makes; the West researches, designs, markets and sells” — no longer holds.

Many firms reason that if they relinquish their space in China’s factory floor, they effectively cede market share to strong local contenders. It would then become only a matter of time before they find themselves competing in third markets, and back home — but on an unlevel playing field, as their Chinese competitors benefit at home from China’s cost advantages and policy support.

The notable rise in local competitiveness in China is neither incidental nor cyclical, but rather the harbinger of a deeper structural transformation. The successes — and limitations — of industrial programs of the past decade are well documented, having focused on select sectors under the “Made in China 2025” initiative. With China’s fifteenth Five-Year Plan published this March, however, something fundamental has shifted, and it seems that many of China’s economic partners have not yet fully grasped the significance of this shift and the risks it entails.

The Chinese government is now deliberately unwinding the previous arrangement it had with industrialized trading partners such as Germany. Beijing wants to become a rule maker instead of a rule taker, cementing its industrial gains by securing the structural positions necessary for continued competitiveness.

Its industrial approach has undergone both an upgrade and an expansion, forming a party-state-industrial complex built upon the shoulders of a new Chinese entrepreneurial class — a demographic of dynamic, highly educated and talented private business owners, founders, and investors — and the deepest and most extensive supply chains of the world.

Beijing’s ambitions are no longer beyond grasp, due to its combination of scale and increasingly sophisticated innovation capabilities. It already accounts for roughly a third of global industrial output, leads global exports in automobiles, dominates battery manufacturing, and has become a major producer of advanced industrial equipment. In automation, China installs more industrial robots each year than any other country. Robot density in manufacturing has now reached — or surpassed — the levels seen in traditional industrial leaders.

The result is that the competitive overlap between foreign and Chinese companies is no longer confined to low-margin manufacturing, but extends into the high-margin, high-control parts of the value chain.

This cross-cutting industrial program now sits at the core of China’s development paradigm. The fifteenth Five-Year Plan aims to interlink education, research funding, industrial policy, and market creation. Large-scale state support is accelerating the diffusion of enabling technologies — industrial AI, advanced manufacturing systems, and clean energy — across the economy. China plans to offer what Europe is struggling to provide: large and predictable demand, integrated manufacturing ecosystems, patient capital, and policy continuity.

Time is not on our side. The Chinese government is not only building up the country’s innovation ecosystem, but also actively pursuing de-risking efforts of its own. Industrial capabilities and technological advances are embedded in a complementary tech-sovereignty framework. Beijing has long identified technological chokepoints — areas where reliance on foreign suppliers is seen as a strategic vulnerability — and has made their elimination a policy priority.

…Germany’s approach so far — focusing on discursive categories and the familiar tripartite framework of its relationship with China – has done little to turn the tide. On the contrary, it might even have distracted attention from the main arena of competition.

German firms feature prominently in this calculus, as many occupy highly specialized niches that are difficult to replicate, thanks to engineering complexity and tacit knowledge embedded across entire production ecosystems. Beijing’s goal is at once to reduce its existing vulnerabilities as well as to remain in tight control over any emerging domestic technological edge, translating Chinese advances into economic and geopolitical leverage.

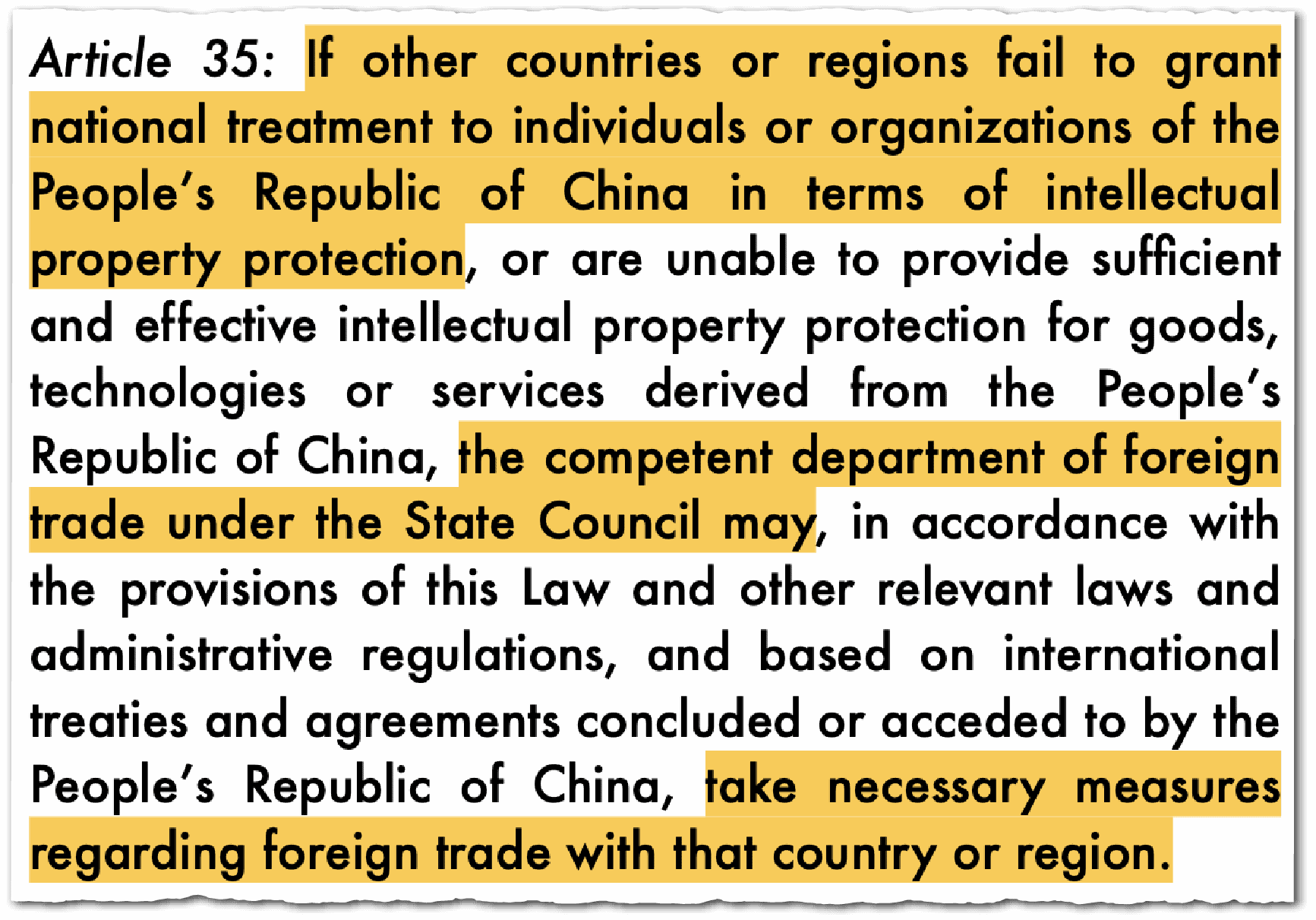

To this end, the Chinese government is building up its own toolbox of instruments to control access to intellectual property in desirable technologies and facilitate the localization of foreign technologies. It can now retaliate against foreign firms if their home country acts against Chinese intellectual property or trade interests. New regulations on industrial supply chains allow Beijing to counter any diversification efforts that harm Chinese commercial or national interests.

Updating our diagnosis of the challenge Germany faces to include a more accurate picture of current and future vulnerabilities, as well as existing strategic leverage, is, then, a matter of urgency.

Yet it is not, as some proponents of China’s system would have us believe, too late either. Despite the narrative of tech-solutionism, stability and superior capabilities pushed by Beijing and its proxies, China is not yet where it wants to be.

China’s scale is currently not fully matched by outcomes in quality, efficiency, and structural optimization. Reported labor productivity and manufacturing value-added rates remain significantly below frontier benchmarks. Several strategic emerging industries are suffering from overcapacity and severe margin compression. Even on innovation, the significant progress to date is not yet matched by depth in foundational principles and shared generic technologies that underpin frontier innovation. In critical technologies, China still has very real levels of self-identified dependencies on Western companies, which translate into geopolitical vulnerability.

Also, as elsewhere, success is not a given. China’s de-risking comes at significant cost. Beijing is struggling to reconcile the drive for technological sovereignty — reducing foreign dependencies, hardening resilience, and extending state control over strategic assets — with the need to remain innovative, commercially dynamic, and globally competitive.

That tension plays out not just in society, but across industrial policy, subsidy design, standards setting, and localization requirements. Chinese experts are well aware of the negative effects of prolonged subsidization, ranging from a dampening effect on innovation and inefficiencies to higher levels of corruption.

What do these constraints mean for China’s future trajectory? If the sovereignty logic dominates, foreign firms in China face rising localization pressure, tighter controls over knowledge flows, and the risk that “localization” becomes a euphemism for de facto technology transfer in sensitive areas. If competitiveness takes precedence, Chinese firms — having matured within a heavily state-supported incubatory environment — will emerge as even stronger global competitors, including in Europe itself. From a European perspective, neither outcome is comfortable.

What is clear is that Germany’s approach so far — focusing on discursive categories and the familiar tripartite framework of its relationship with China – has done little to turn the tide. On the contrary, it might even have distracted attention from the main arena of competition. An accurate assessment of Germany’s position requires a more granular focus on the fundamentals, the nitty-gritty of industrial production capabilities, innovation ecosystems, and the protection of critical technology. These are the areas in which de-risking efforts will have to pass muster in future.

Elisa Hörhager is the Chief Representative in China for the Federation of German Industries (BDI). She previously served as a diplomat at German embassies in Beijing and Brussels, as well as on international economic affairs in Berlin.