The criticism that “Hong Kong stablecoins cannot rely solely on licenses” is not a sign of pessimism, but rather highlights the key areas that need to be addressed in the next phase.

Article by Farmer Frank

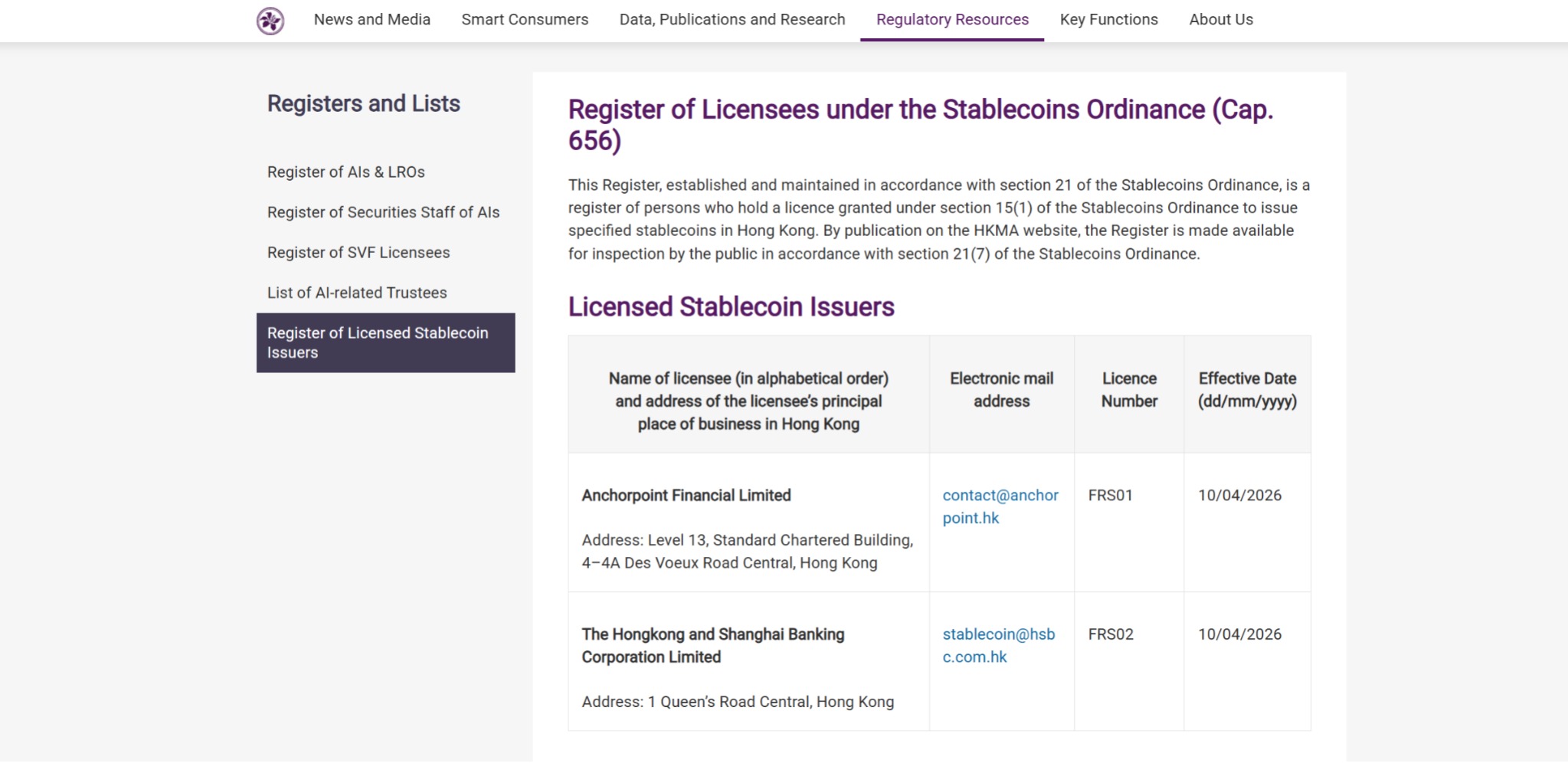

On April 10, 2026, the Hong Kong Monetary Authority officially granted the first stablecoin issuer licenses to AnchorPoint Fintech Limited and The Hongkong and Shanghai Banking Corporation Limited. With this, Hong Kong has become one of the first financial centers globally to complete the full regulatory cycle of “legislation—review—licensing,” marking the formal transition of stablecoin regulation from policy design to licensed operation.

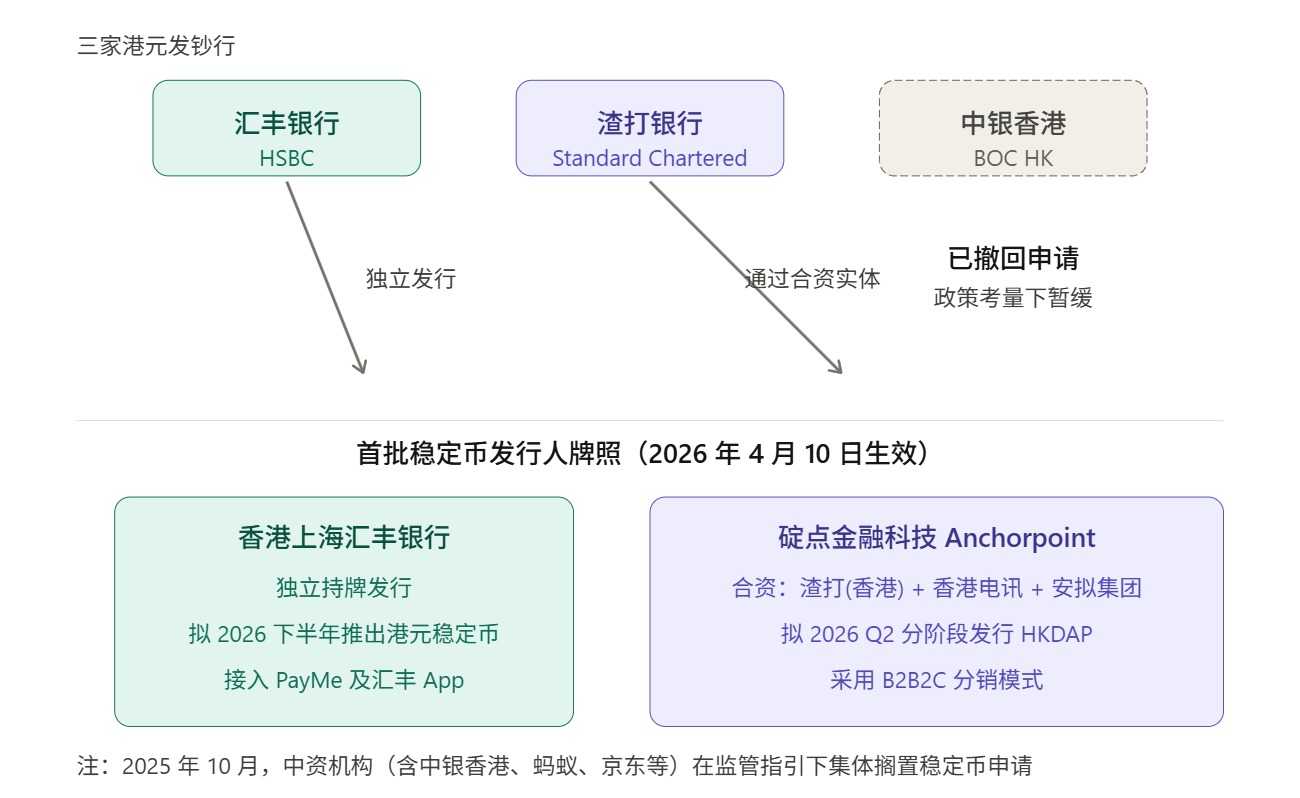

Amid the flood of news, many have noticed a telling signal: the first two companies to receive licenses are HSBC, holding its license independently, and Dianrong Financial, backed by a joint venture between Standard Chartered (Hong Kong), Hong Kong Telecom, and Animoca Brands.

In other words, among the first entrants, HSBC and Standard Chartered are two of Hong Kong’s three note-issuing banks.

What does this mean?

I. From “Issuer of Currency” to “Stablecoin Issuer”

To be frank, it is not surprising that the first licenses went to HSBC and Standard Chartered, but the policy signals behind this choice are well worth careful interpretation.

This requires returning to Hong Kong’s own unique currency issuance system. It is well known that under Hong Kong’s current banknote system, commercial banks are primarily responsible for issuing banknotes, with the exception of the HK$10 note, which is issued directly by the Hong Kong government (the Monetary Authority). The HK$20, HK$50, HK$100, HK$500, and HK$1000 banknotes are issued by three authorized banks: HSBC, Standard Chartered, and Bank of China (Hong Kong).

In other words, on issues of currency and financial infrastructure, Hong Kong has long adhered to a clearly defined institutional arrangement: front-line issuance functions are carried out by highly regulated commercial institutions, while regulators maintain system stability through rules, reserve requirements, and prudential standards.

Viewed within this framework, granting the first stablecoin licenses to the consortium led by HSBC and Standard Chartered essentially continues the approach of starting with the most reliable entities, consistent with Hong Kong’s own monetary traditions.

For a new category that has just entered a formalized phase, the initial issuance of licenses aimed at stability, control, and avoiding mistakes is a perfectly normal approach for financial regulators.

This is actually not hard to understand.

Although stablecoins wear the guise of “virtual assets,” once they enter a formalized phase, regulators will never first focus on the story—they will focus on the most traditional and fundamental financial questions: whether the reserve assets are genuine, whether the redemption mechanism is clear, whether risk isolation is adequate, whether fund flows are controllable, and whether anti-money laundering and traceability mechanisms are reliable.

But following this logic, another question naturally arises: why is Bank of China (Hong Kong) absent from the three note-issuing banks?

This matter clearly goes beyond a simple issue of qualifications or capabilities. In fact, Bank of China (Hong Kong) was widely regarded as an active participant among the first applicants in August–September 2025, until a joint statement from central authorities in October 2025 further clarified policy boundaries, imposing stronger constraints on private stablecoins—particularly RMB-pegged stablecoins. As a result, several Chinese institutions originally planning to participate—including Bank of China (Hong Kong), Bank of Communications (Hong Kong), China Construction Bank (Asia), as well as major internet companies like Ant and JD—put their related plans on hold.

Source: Fudan Research Institute

This also means that granting the first licenses to two note-issuing banks reflects Hong Kong’s institutional logic of prioritizing stability in its early stages, as well as a practical response to the current cross-border policy environment. Whether Hong Kong’s stablecoins can succeed in the long term ultimately depends on who can truly scale this system in the next phase.

And this is precisely the aspect most discussions tend to overlook.

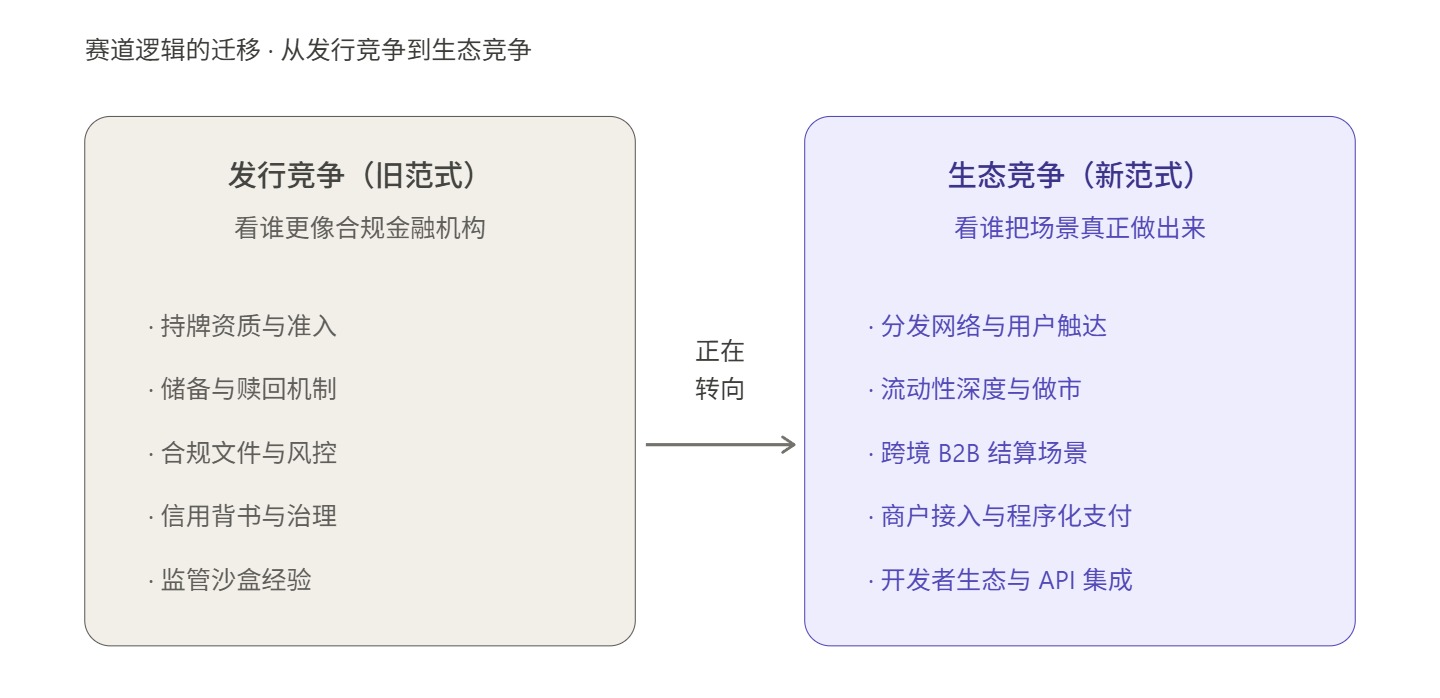

Two: Compliance is important, but a “license” does not equal an “ecosystem”

When analyzing the prospects of Hong Kong’s stablecoins, an unavoidable point of reference is the development journey of Hong Kong’s virtual banks.

In 2019, the Monetary Authority issued virtual bank licenses to eight institutions, at which time market expectations were high, and many believed the new licensing framework would automatically create a new competitive landscape and enhanced financial experiences; by 2024, the Monetary Authority released a review report indicating that the market had responded positively to the products and services offered by the eight virtual banks, but also clearly stated that the current number of virtual bank licenses was appropriate and no new licenses would be issued for the time being.

This is a very typical case study. Looking back, virtual banks have certainly achieved some results, but the license did not automatically translate into market dominance, nor did it automatically lead to a sustainable business model. This reveals a practical reality: in a financial system with established profit pools, mature customer relationships, and well-developed clearing channels, there is often a long gap between regulatory openness and market adoption.

In short, a license can solve access issues, but it cannot solve problems related to user habits, scenario coverage, business efficiency, or network effects.

The same applies to stablecoins, and the difficulty will only be greater.

After all, unlike virtual banks, it must not only compete with the traditional financial system but also contend globally with established players like USDT and USDC, which are deeply embedded in exchanges, on-chain protocols, and wallet systems.

Ultimately, obtaining a license does not automatically grant you market adoption. A license only addresses whether you are permitted and trusted to issue a stablecoin, but it does not solve several more difficult questions: Why would users choose your stablecoin? Why would exchanges, wallets, merchants, market makers, and corporate financial systems accept your stablecoin? Why would capital be willing to remain, circulate, and accumulate within your system, ultimately creating network effects?

In other words, issuance is a supply-side qualification, while the ecosystem is the demand-side solution.

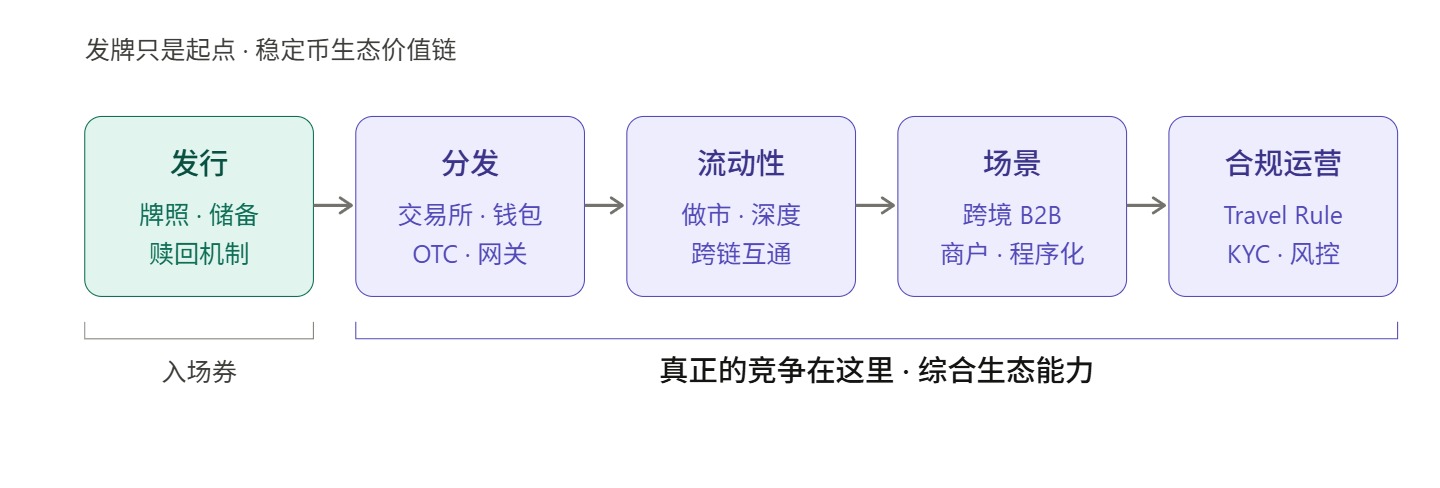

From a market competition perspective, the real test only begins at the moment of licensing, as the stablecoin competitive chain encompasses at least five stages:

- Issuance addresses the question of “whether it exists.”

- Distribution addresses the question of whether it reaches the user.

- Liquidity addresses the question of whether you can enter and exit with low friction.

- The scenario addresses the question: “What else can you do besides holding?”

- Operations address the question of “how to ensure compliance, clearing, risk control, identity verification, and user experience run stably over the long term.”

And among these five steps, issuance is only the first.

This is why the external criticism that “Hong Kong stablecoins can’t just be about licensing” should not be simply interpreted as pessimism; on the contrary, such criticism highlights the essential next steps Hong Kong stablecoins must address—after obtaining a license, without sufficient distribution capabilities, liquidity organization, and use case adoption, Hong Kong stablecoins may remain merely institutionally sound but struggle to achieve commercial success.

Today’s global stablecoin market is no longer one where compliance labels alone can win users; user habits, entry points, trading depth, settlement efficiency, wallet integration, fiat on/off-ramp capabilities, and developer APIs are the key variables that determine whether a stablecoin truly comes to life.

Looking at the development path of overseas markets, this shift in focus is already very clear.

After completing its acquisition of Bridge, Stripe no longer treats stablecoins as a peripheral payment capability, but instead integrates them deeper into corporate treasury management and global payment systems—for example, with the 2025 launch of Stablecoin Financial Accounts for businesses in 101 countries, followed by Open Issuance powered by Bridge, all aimed at elevating stablecoins from a supported alternative asset to a “payment capability embeddable within corporate financial systems.”

Circle’s actions are equally representative. Over the past period, Circle has consistently advanced USDC toward a more “programmatic payment” direction: on one hand, it has publicly promoted autonomous payments based on x402, enabling AI agents to use USDC to automatically pay for APIs, computing power, data, and content; on the other hand, it is also working to standardize the capability of making extremely small, machine-to-machine payments.

This indicates that, in the eyes of the most sophisticated players in payment infrastructure, the focus of stablecoin competition has long moved beyond mere issuance eligibility to who can turn it into a financial底层 that businesses can invoke, settle, and manage.

Hong Kong has previously had similar practices: ahead of the official implementation of Hong Kong’s Stablecoin Ordinance last year, the licensed OSL Group launched three new products fully targeted at institutions: the compliant stablecoin management platform StableX, the asset tokenization service Tokenworks, and the enterprise-grade crypto payment solution OSL BizPay. In 2026, it further launched USDGO, an enterprise-grade compliant USD stablecoin that complies with U.S. federal regulations and can be legally distributed in Hong Kong, primarily focusing on areas such as cross-border e-commerce, bulk trade, and interactive entertainment.

Looking at Hong Kong in this context reveals a more critical issue: the first batch of licenses addresses “who gets safe entry,” but whether Hong Kong can build a truly competitive stablecoin ecosystem depends on who steps in to complete the next four tasks.

Three: Issuance is not the end goal; ecosystem collaborators are key.

From the structure of the global stablecoin market, the division of ecological roles has become increasingly clear.

The most prominent feature is the high concentration on the issuance side. For example, USDT and USDC together account for over 86% of the total stablecoin market cap, but the issuing entities’ scale advantage does not inherently equate to ecosystem control. The true competitiveness of stablecoins often depends less on issuance volume and more on liquidity depth, channel coverage, and scenario penetration.

Like USDC, which has only 42% of the market cap of USDT, its activity on-chain, in institutional payment use cases, and within the developer ecosystem is significantly higher—this is driven by distribution networks and use case adoption, not merely issuance volume; similarly, while PYUSD is legally issued by Paxos, its expansion is primarily fueled by PayPal’s account distribution network.

This shows that the issuers of stablecoins and the builders of their ecosystems are now two distinct combinations of capabilities:

- The issuer is responsible for reserve management, compliance and risk control, and the redemption mechanism—core functions of the issuance layer;

- Ecosystem partners are responsible for distribution channels, liquidity aggregation, scenario integration, and business operations—core tasks of the “application layer.”

There is not a substitutive relationship between the two, but rather a collaborative upstream-downstream relationship.

If the stablecoin ecosystem is compared to a building, then obtaining a license for the issuer is merely securing the permit to lay the foundation; what truly determines how high the building can rise are the load-bearing structures of each subsequent floor—distribution channels, trading liquidity, payment networks, use case integrations, and compliance capabilities are precisely some of these load-bearing elements.

So the real test for Hong Kong stablecoins may never have been “who can get a license,” but rather “who can actually put it to use after getting the license.”

This is why, in the next phase, what Hong Kong’s stablecoin ecosystem truly needs may not just be new issuers, but rather ecosystem platforms capable of handling distribution, trading, payments, liquidity, and compliant operations.

In fact, even the first licensed institutions themselves are demonstrating this through action. According to reports, Anchor Finance plans to partner with selected companies as distribution partners to offer its stablecoin to the public; HSBC is preparing to reach users through the PayMe and HSBC HK Mobile Banking apps.

In other words, even for the first issuer to obtain a license, the immediate reaction upon launch is not “I can finally issue a coin,” but rather “How do I distribute it?” This itself demonstrates that stablecoins are not a business that can be completed by the issuer alone, but rather a systemic endeavor requiring multi-layered ecosystem collaboration.

It is in this sense that what Hong Kong will truly lack in its next phase may not be just new issuers, but ecosystem platforms capable of handling distribution, trading, payments, liquidity, and compliant operations.

This is the most noteworthy position in this round of discussion—a comprehensive capability platform that can connect the issuance, circulation, and usage sides may truly determine the height of Hong Kong’s stablecoin ecosystem.

OSL, the licensed local Hong Kong player mentioned above, has clearly stated its intention to actively collaborate with licensed stablecoin issuers in Hong Kong, leveraging its strengths in distribution, liquidity, and infrastructure to facilitate the deployment of related products and use cases—indicating that it is proactively positioning itself as a service provider laying the “capillaries” for this broader stablecoin network.

Objectively speaking, for a nascent market that inherently requires multi-party collaboration, the scarcity of such roles may be no less than that of issuing licenses themselves.

But this is the key variable that will determine whether Hong Kong’s stablecoins can secure a place in global competition.

In conclusion

From a broader perspective, the situation facing Hong Kong stablecoins today is indeed challenging.

Looking at the mainland, policy guidelines are unlikely to loosen in the short term; looking overseas, barriers from user habits and network effects are already very high. Under this landscape, if Hong Kong’s stablecoin ecosystem remains confined to the level of “licensing—issuance—compliance,” it risks repeating the fate of virtual banks—appealing regulations and solid metrics, yet a broader ecosystem fails to emerge.

But conversely, this is precisely Hong Kong’s window of opportunity.

The global stablecoin market is undergoing a profound paradigm shift: stablecoins are no longer merely transactional mediums within the crypto ecosystem; they are being reimagined as the next-generation infrastructure for global payments and settlements. In this new paradigm, compliance capability is no longer the sole competitive dimension—distribution networks, payment use cases, technological infrastructure, and ecosystem operational capabilities have become equally, if not more, critical.

As an international financial center, Hong Kong inherently possesses advantages in institutional design and compliance governance. However, to truly transform these advantages into competitiveness in the stablecoin ecosystem, first-round licenses alone are insufficient. It also requires payment companies, technology platforms, compliance middleware, Web3-native enterprises, and local licensed institutions to progressively execute the more challenging and authentic tasks of distribution, liquidity, use cases, and operations.

The road ahead after licensing is long; the real competition for Hong Kong stablecoins has only just begun.