Chinese DRAM maker plans massive capacity expansion, but analysts say technology gaps and heavy reliance on domestic demand remain major hurdles

China’s ChangXin Memory Technologies is throwing its hat into the ring with a roughly $8.5 billion initial public offering as it seeks to challenge the dominance of Samsung Electronics, SK hynix and Micron Technology.

Set to list on Shanghai’s STAR Market on July 27 in the largest flotation by a Chinese chipmaker, CXMT is using the offering as a global debut, billing itself as China’s largest and the world’s fourth-largest DRAM maker by capacity despite a far smaller market share than the industry’s top three.

Priced at 8.66 yuan ($1.30) a share, the IPO is expected to raise 57.9 billion yuan, or up to 66.6 billion yuan with a 15 percent overallotment option, valuing CXMT at about $85.2 billion.

The haul, nearly double the 29.5 billion yuan in projects outlined in its prospectus, will fund a rapid capacity expansion, a push into higher-value memory, and efforts to narrow the technology gap with global rivals.

Analysts say CXMT needs a 15 percent share of global DRAM bit shipments to secure a stable position among top-tier suppliers and sustain investment in next-generation technology.

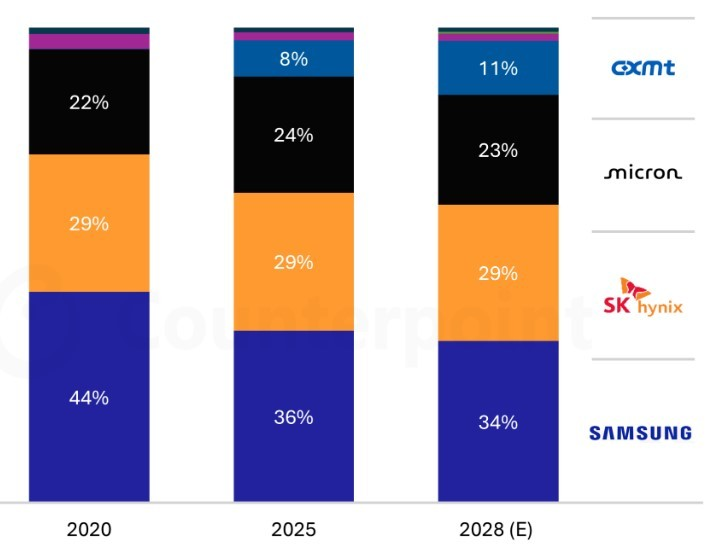

The fast-growing company currently holds about 9 percent and is projected to reach 11 percent by 2028, according to Counterpoint Research.

Hwang Min-seong, a research director at Counterpoint says the 15 percent market share is a “threshold CXMT must cross,” citing Taiwan’s DRAM makers as a cautionary example. After their combined share fell below that level in 2008, they struggled to finance advanced fabs and eventually retreated to about 3 percent of the market as niche suppliers.

By revenue, CXMT has also gained ground rapidly, with its global DRAM share rising from 4.1 percent in the first quarter of 2025 to 7.6 percent a year later, according to TrendForce. Samsung Electronics, SK hynix and Micron held 38 percent, 29 percent and 22 percent, respectively, in the latest quarter.

The IPO will fund a broad expansion aimed at sustaining that growth. CXMT plans to invest in its fifth-generation G5 DRAM process, 12-layer HBM3 and new production facilities, while improving yields for the more advanced server DDR5 and mobile LPDDR5X chips and developing DDR6.

Monthly wafer capacity is projected to rise from about 320,000 to 420,000 by 2027 through new fabs in Shanghai and Beijing as well as a large manufacturing cluster in Hefei. The company aims to double capacity by 2030 and triple it by 2035 while shifting toward higher-value products, with LPDDR5 and DDR5 expected to account for about 75 percent of output.

Risks, opportunities ahead

The global memory shortage has created favorable conditions for CXMT’s expansion. As DRAM prices rise, the company has grown into a major supplier of commodity DRAM chips such as DDR4 and LPDDR4, which the industry leaders have increasingly moved away from to focus on higher-margin chips, such as HBMs.

Price offers another advantage. CXMT’s chips are estimated to be 5 to 10 percent cheaper than those of Samsung, SK hynix and Micron, potentially attracting more buyers as supplies tighten. Apple, one of the world’s largest memory customers, is reportedly seeking greater regulatory clarity from Washington while considering the use of CXMT chips in devices sold only in China.

Even so, CXMT remains well short of challenging the industry’s entrenched Big Three.

Its technology gap is generally estimated at two to three years. CXMT began mass-producing LPDDR5 and DDR5 only late last year, products long established among the three leaders, while yields are still considered unstable.

The gap is wider in high-bandwidth memory, the key AI chip component driving profits at Samsung, SK hynix and Micron. While the market leaders have kicked off sixth-generation HBM4 and are moving with sampling for HBM4E, CXMT remains at an earlier stage of development for fourth-generation HBM3 and is set for mass production of HBM3E next year.

CXMT is heavily reliant on domestic sales, with overseas sales accounting for just 2.79 percent of revenue. Its largest customers — including Alibaba Cloud, ByteDance, Xiaomi and Honor — are predominantly Chinese, while the top five generated about two-thirds of core business revenue.

The sharp rise in server DRAM sales, from 8.39 percent of revenue in 2024 to 26.51 percent last year, appears driven more by China’s AI infrastructure localization push than by broader global adoption.

Restricted access to advanced lithography equipment poses another long-term obstacle. CXMT is responding by accelerating alternative technologies, including vertical channel transistors and wafer-on-wafer bonding.

“Ironically, restrictions on CXMT could create an opportunity for it to leapfrog the incumbents,” said Neil Shah, vice president at Counterpoint Research, noting that established suppliers may be slower to adopt new architectures as they seek returns on existing equipment.

“CXMT could turn the constraints of export controls into a catalyst for narrowing the gap and potentially surprise its rivals,” he added.

herim@heraldcorp.com