Introduction & Market Context

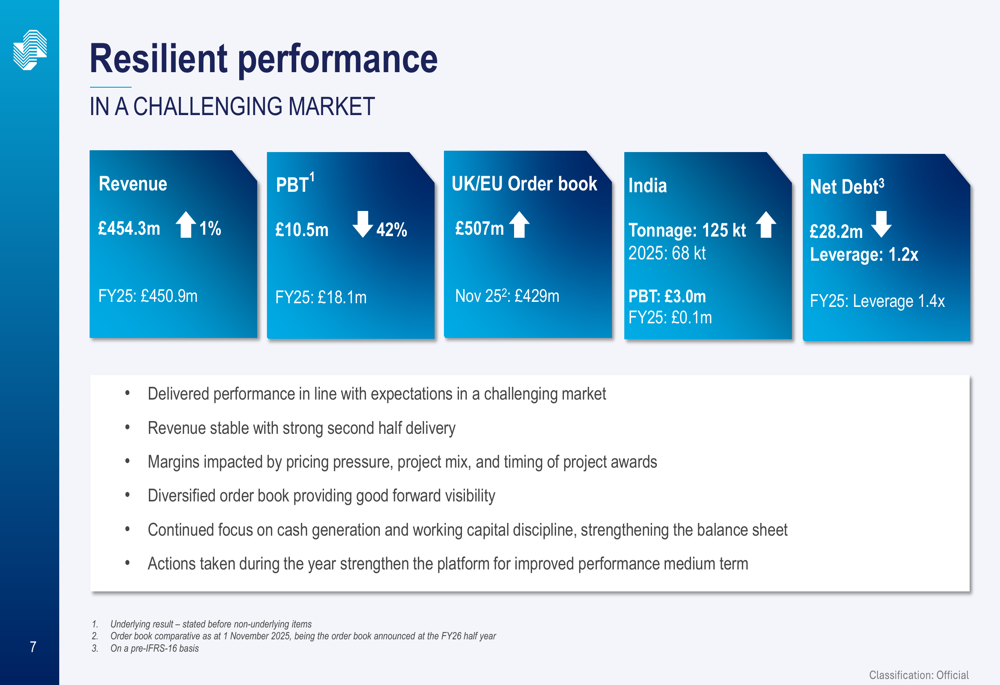

Severfield presented its full year 2026 results on June 23, revealing a challenging period marked by margin compression offset by strong cash generation and record performance from its Indian joint venture. The UK structural steel specialist reported revenue of £454.3 million, up marginally from the prior year, but underlying profit before tax fell 42% to £10.5 million as the company navigated competitive pricing pressure and a strategic transformation.

The company’s shares rose following the update, with the stock trading at $31.60, up 6.76% from the previous close of $29.60, suggesting investors are looking past near-term profit weakness toward the company’s restructuring efforts and medium-term targets.

Management characterized the year as one of “resilient performance in a challenging market,” pointing to subdued UK and European construction activity, steel price volatility, and competitive tendering as key headwinds. The presentation outlined six months of decisive action to strengthen the business platform and set ambitious medium-term targets of £40-50 million in underlying profit before tax.

Financial Performance Highlights

The company’s financial metrics for FY26 reflect a business in transition, with stable revenue masking significant margin deterioration. As illustrated in the following performance summary, several key indicators moved in opposite directions.

Revenue remained essentially flat at £454.3 million compared to £450.9 million in FY25, representing growth of just 1%. However, underlying profit before tax declined sharply to £10.5 million from £18.1 million, a drop of 42%. The company’s operating margin compressed to 2.8% from 4.8% the previous year—well below the FY22-25 average of 6.6%.

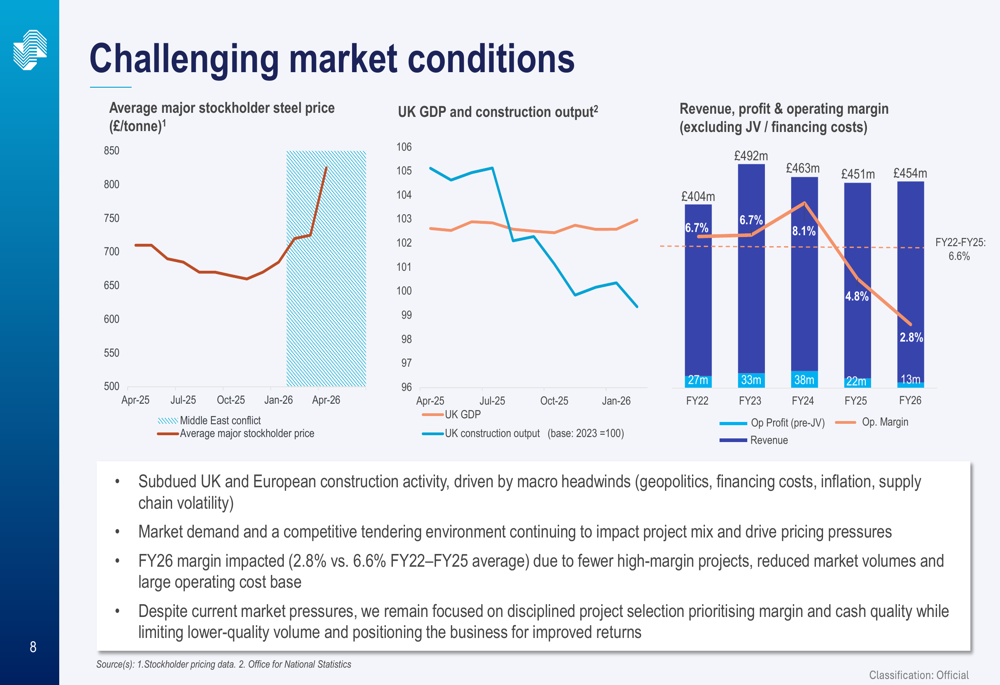

The margin pressure stemmed from multiple factors. As shown in the following analysis of market conditions, steel prices fluctuated between £650 and £750 per tonne during the year, with a notable dip during the Middle East conflict period. UK construction output declined from over 104 to below 98 on a base of 2023=100 between July 2025 and January 2026.

The company’s revenue, profit, and operating margin trends over the five-year period from FY22 to FY26 show a clear deterioration. Operating profit fell from £38 million in FY24 to just £13 million in FY26, while the operating margin dropped from a peak of 8.1% in FY24 to 2.8% in FY26.

Management attributed the margin compression to competitive pricing pressure, project mix weighted toward lower-margin work, and timing delays in major project awards. Chief Financial Officer Andrew Page noted that “the market is competitive, and this is something that has been developing over the last few years.”

The statutory results were significantly worse, showing a loss before tax of £39.9 million after £50.3 million in non-underlying costs. These exceptional charges included £12.6 million for the Modular Solutions closure, £5.7 million for bridge testing and remedial costs net of insurance, and £22.2 million in asset impairment charges.

Strategic Transformation and Decisive Action

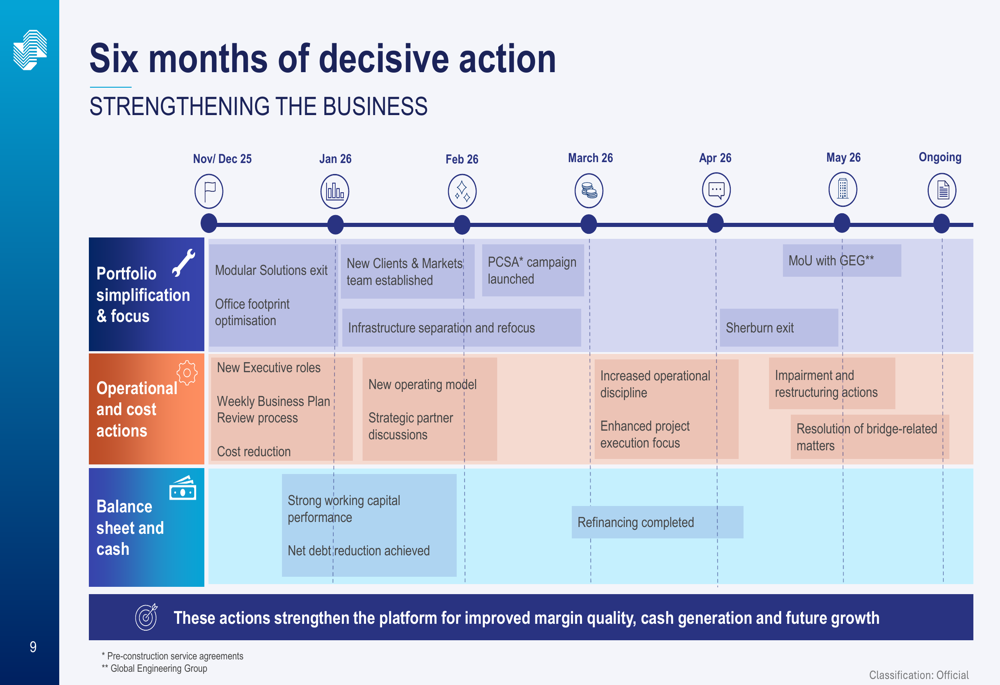

Facing margin pressure, Severfield executed a comprehensive restructuring program over the six months leading up to the results. The timeline of actions demonstrates management’s urgency in repositioning the business.

The transformation encompassed three main areas: portfolio simplification, operational improvements, and balance sheet strengthening. Key actions included exiting the sub-scale Modular Solutions business, optimizing the office footprint, establishing a new Clients & Markets team, and separating and refocusing the infrastructure division.

Chief Executive Paul McNerney emphasized the strategic shift: “We need to sharpen our focus on quality of earnings, prioritizing margin, cash generation, and therefore shareholder value.” The company is moving away from a volume-led model toward higher-margin, more selective work in complex projects across the UK, Europe, and India.

The presentation outlined a clear strategic framework showing how the company’s services, geographies, and transformation programs align to deliver sustainable shareholder returns. The strategy centers on four service areas—project management, delivery, design and engineering, and manufacturing—supported by four transformation programs: Clients & Markets Focus, Manufacture 360°, Engineering Excellence, and Performance & Productivity.

India Joint Venture Reaches Tipping Point

While UK margins contracted, the company’s Indian joint venture JSSL delivered record performance across all metrics. The following charts illustrate the dramatic growth trajectory.

Tonnage output surged to 125,000 tonnes in FY26 from 64,000 tonnes in FY25, nearly doubling year-over-year. Revenue reached £140 million, up from £103 million, while profit before tax jumped to £7.8 million from just £0.3 million. The group’s 50% share after tax contributed £3.0 million, compared to £0.1 million in the prior year.

Perhaps most impressive was the order book growth, which reached a record £344 million in June 2026, up from £286 million in November 2025. The order book showed increasing diversification into higher-margin sectors including data centers, commercial buildings, and infrastructure projects.

Management described the joint venture as having “reached a tipping point,” with capacity expansion underway in Gujarat. Current capacity of 7,000 tonnes is planned to increase to 50,000 tonnes by FY27 and 150,000 tonnes by FY29. The partnership with JSW Steel provides access to scale and steel supply as JSW expands its own capacity from 35.7 million tonnes per annum to 62.0 million tonnes by FY32.

Major projects in India include the Iron Mountain data center in Navi Mumbai (14,000 tonnes), the Amaravati government office building (15,000 tonnes featuring India’s first dia-grid design), and the TEL semiconductor factory in Dholera (11,000 tonnes).

UK and Europe Order Book Strengthens

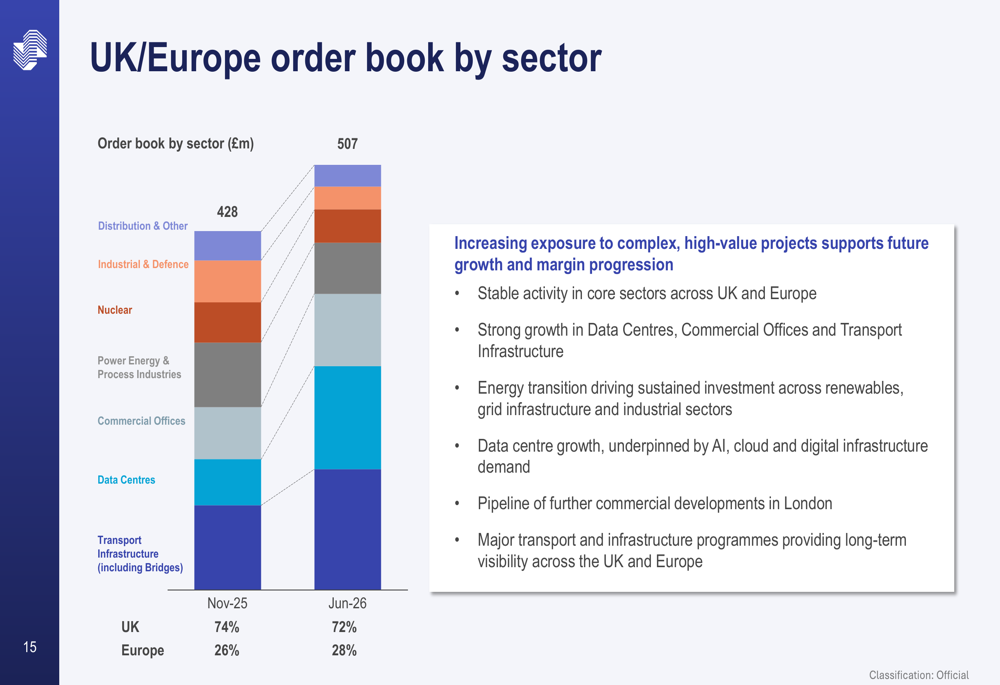

Despite the challenging market, the UK and Europe order book grew to £507 million from £429 million in November 2025. The composition of the order book shows strategic progress toward higher-value sectors.

The order book breakdown reveals growing exposure to data centers, commercial offices, and transport infrastructure—all areas where Severfield can leverage its engineering expertise and command better margins. Data center work has become a particular growth driver, underpinned by AI, cloud computing, and digital infrastructure demand.

Geographically, the UK represented 72% of the order book with Europe at 28%, showing modest expansion in the European footprint. Major projects include the Agratas electric vehicle battery facility (22,000 tonnes delivered in just 26 weeks), INEOS Project ONE (7,500 tonnes utilizing both UK and European fabrication), and various bridge and infrastructure projects.

The company emphasized its focus on “complex, high-value projects” where engineering capability matters more than price. Page noted that Severfield is trying to “differentiate ourselves in the higher quality, high-margin work” rather than compete on price in commodity segments.

Balance Sheet Strengthening and Cash Generation

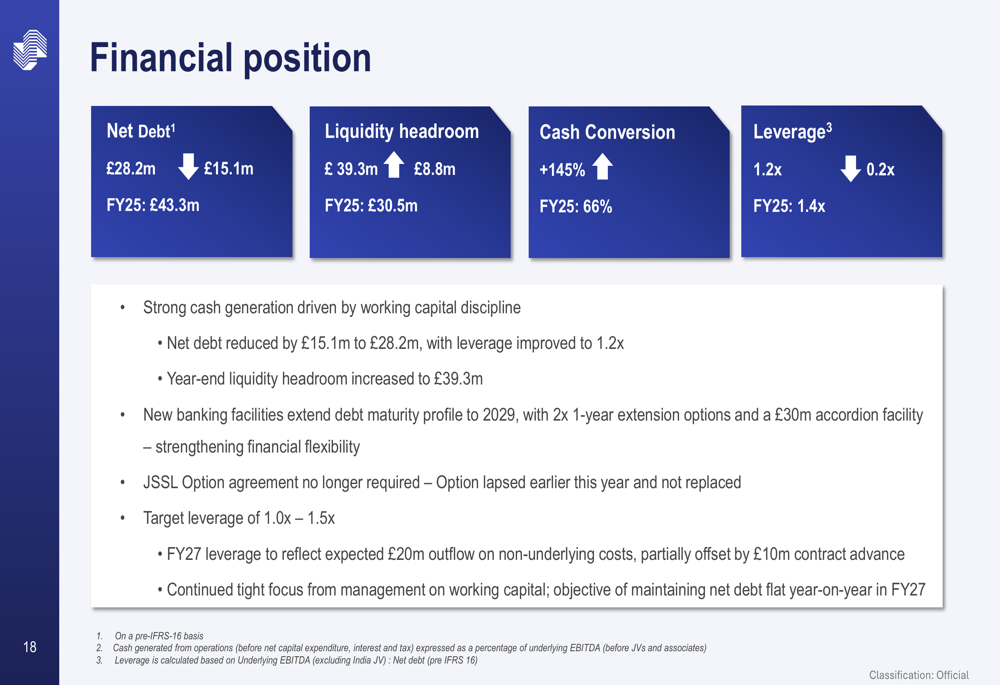

A bright spot in the results was the company’s cash performance and balance sheet improvement. Despite the profit decline, Severfield generated strong cash flow and reduced leverage.

Net debt fell by £15.1 million to £28.2 million, bringing leverage down to 1.2x from 1.4x—well within the company’s target range of 1.0-1.5x. Liquidity headroom increased to £39.3 million from £30.5 million, and cash conversion reached 145% compared to 66% in the prior year.

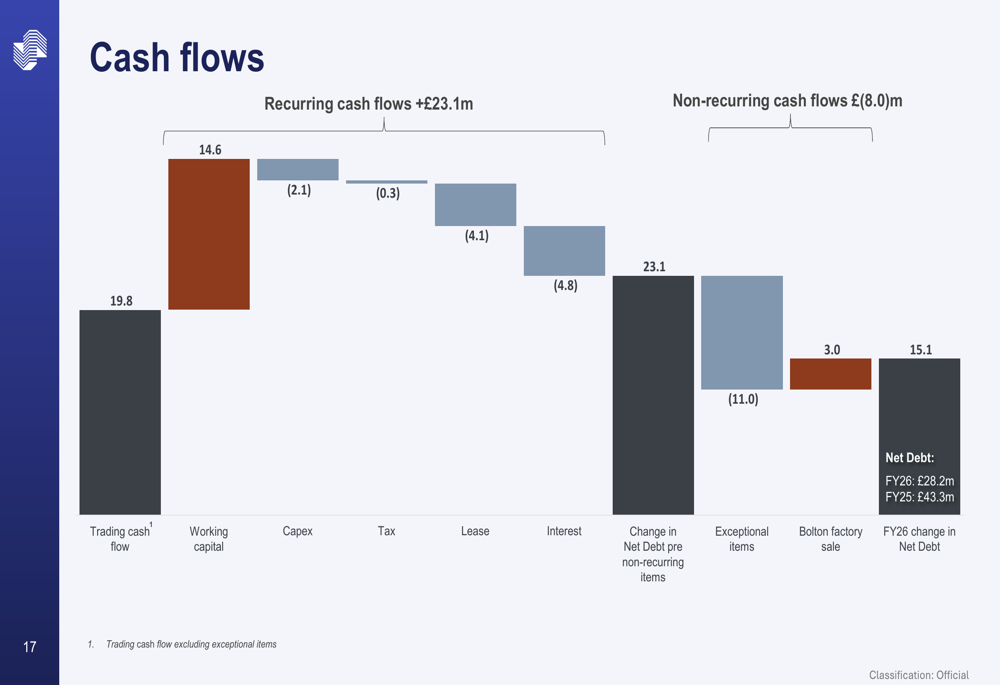

The cash flow performance was driven by disciplined working capital management. As shown in the detailed cash flow analysis, working capital contributed £14.6 million to cash generation, offsetting the lower operating profit.

The company completed a refinancing during the year, extending its debt maturity profile to 2029 with two one-year extension options and a £30 million accordion facility. This provides financial flexibility as the company executes its turnaround plan.

Management expects net debt to remain broadly flat in FY27, with an anticipated £20 million outflow related to non-underlying provisions partially offset by a £10 million contract advance already secured. The company targets leverage of 1.0-1.5x over the medium term.

Forward Outlook and Medium-Term Ambition

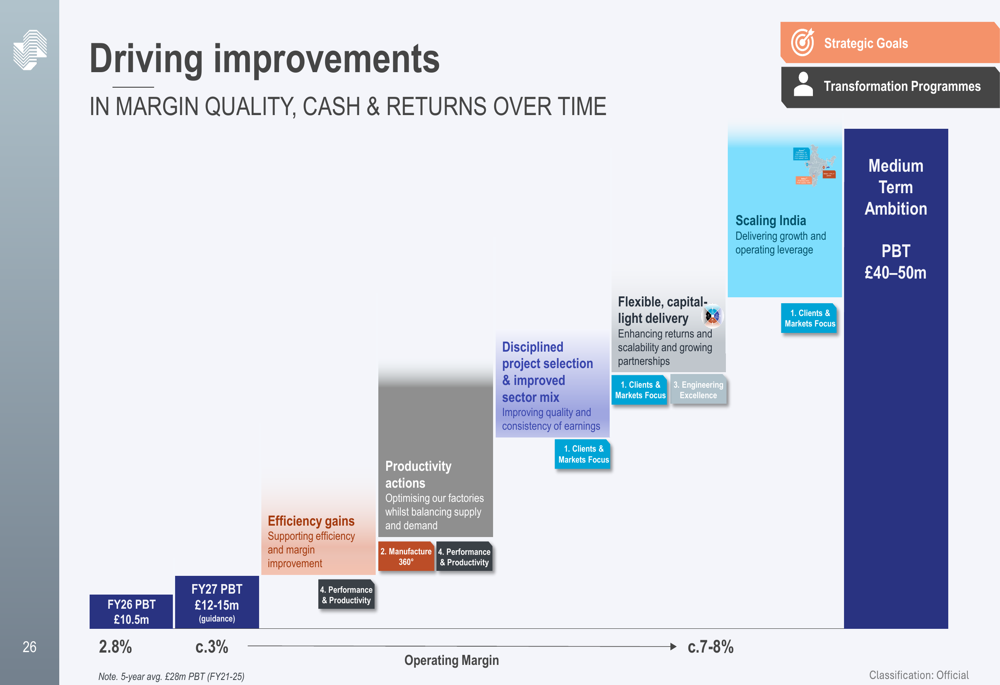

Looking ahead, management characterized FY27 as a “transition year” and provided guidance for underlying profit before tax of £12-15 million. This represents an improvement from FY26’s £10.5 million but acknowledges continued near-term headwinds as older, lower-margin contracts roll off.

The more significant message came in the company’s medium-term ambition. The following roadmap illustrates the path from current performance to target levels.

The company aims to reach £40-50 million in underlying profit before tax with operating margins of 7-8%, representing a substantial improvement from the current 2.8%. The strategy to achieve this involves five key pillars: efficiency gains, productivity actions in manufacturing, disciplined project selection and improved sector mix, flexible capital-light delivery models, and scaling the India business.

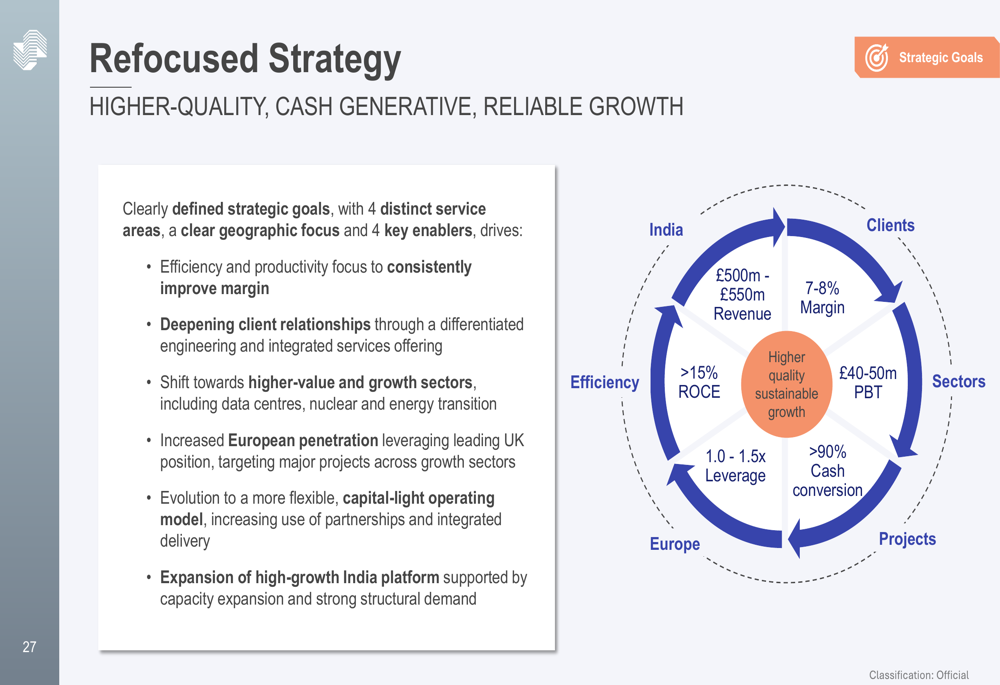

The comprehensive financial targets for this medium-term ambition are presented in the company’s strategic framework.

The targets include revenue of £500-550 million, profit before tax of £40-50 million, operating margin of 7-8%, cash conversion above 90%, leverage of 1.0-1.5x, and return on capital employed above 15%. India is expected to contribute approximately £10 million of underlying profit in the medium term, up from £3 million in FY26.

McNerney emphasized the geographic diversification strategy: “We’re not at the mercy of any one economic backdrop in one country,” noting that the mix of UK, Europe, and India should reduce volatility in earnings and cash flow.

Strategic Repositioning and Capital Allocation

The company outlined a clear capital allocation framework balancing growth investment with debt reduction and eventual dividend restoration. Operating cash flow will be directed toward growth capital expenditure meeting strict return criteria (IRR greater than WACC), loan repayments, and working capital discipline.

Management emphasized a “capital-light” growth model, expanding through strategic partnerships and integrated delivery rather than heavy fixed asset investment. Capital expenditure in FY26 was just £2.1 million, well below the typical maintenance level of around £8 million, reflecting the constrained investment environment.

On dividends, management stated a “future intention to reinstate dividend, subject to sustainable cash generation and financial framework.” No timeline was provided, but the focus remains on strengthening the balance sheet and demonstrating consistent profitability before returning cash to shareholders.

The company’s transformation programs—Clients & Markets Focus, Manufacture 360°, Engineering Excellence, and Performance & Productivity—are designed to drive efficiency, improve project execution, and enhance margins without requiring significant capital deployment.

Market Reaction and Analyst Perspectives

The stock’s positive reaction suggests investors are willing to look past the near-term profit weakness and focus on the strategic repositioning and India growth story. The 6.76% gain puts the stock at $31.60, within its 52-week range of $21.60 to $40.20 but still well below the high.

Analysts forecast earnings per share of $0.04 for FY27, marking a return to profitability after the company posted a loss of $0.16 per share over the last twelve months. The modest FY27 guidance of £12-15 million underlying profit before tax appears achievable given the £507 million UK/Europe order book and India’s momentum.

Key questions from analysts centered on order book firmness, competitive dynamics, and India’s contribution trajectory. Management expressed confidence in the order book, highlighting projects such as Vista in London, Old Oak Common transport infrastructure, and data center developments as likely to proceed.

The medium-term targets of £40-50 million profit before tax represent nearly a quadrupling from current levels, requiring successful execution across multiple fronts: margin improvement in the UK through better project selection, European expansion, India scaling, and operational efficiency gains. While ambitious, the targets appear grounded in specific initiatives rather than broad market assumptions.

The company’s focus on “quality over volume” represents a significant strategic shift for a business that historically competed across a broad range of structural steel work. Success will depend on whether Severfield can consistently win the complex, high-value projects where engineering expertise commands premium pricing, while avoiding the temptation to fill capacity with lower-margin work during market downturns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.