AlphaStreet Newsdesk powered by AlphaStreet Intelligence

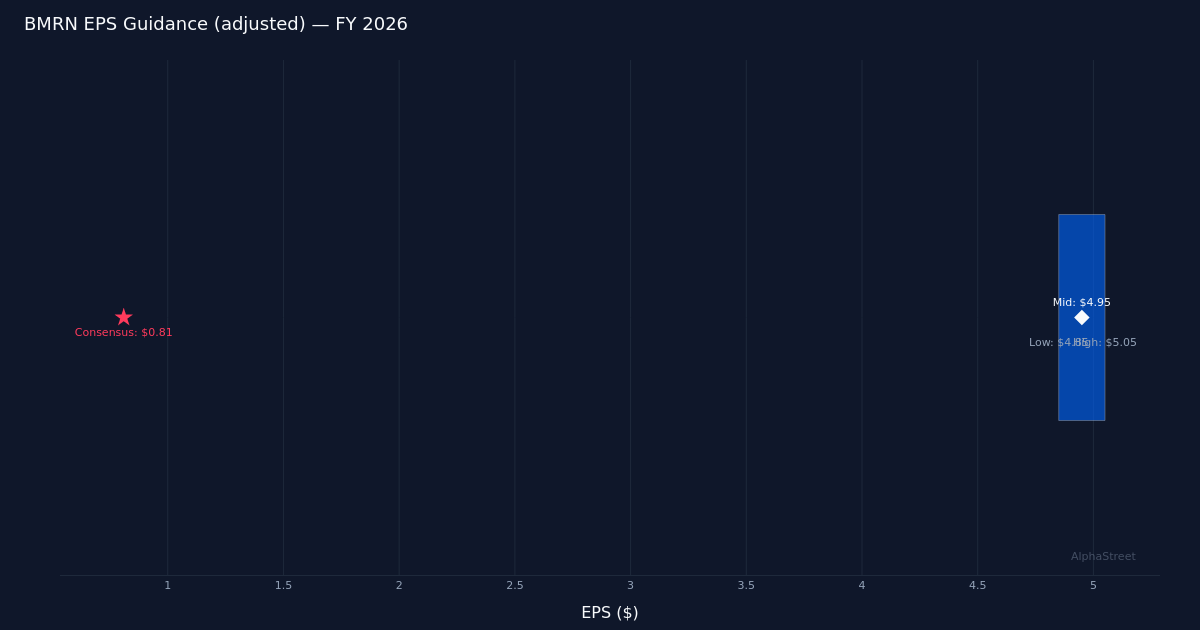

Guidance adjusted $4.85 – $5.05|Stock $55.46 (+2.6%)

EPS YoY -20.0%|Rev YoY +2.8%|Net Margin 13.8%

BioMarin Pharmaceutical’s Q1 2026 results reveal a troubling divergence: revenue beat expectations by 1.8% while adjusted earnings per share of $0.76 missed estimates by 20.8%, missing the $0.81 consensus. The biotechnology company posted net income of $105.5M on revenue of $766.2M, but profitability metrics deteriorated sharply from year-ago levels, raising questions about the sustainability of BioMarin’s margin profile despite growing demand across its key franchises.

The earnings quality story tells a concerning tale of margin compression overwhelming top-line gains. While revenue advanced 3.0% year-over-year from $745.1M, net margin contracted by 15.9 percentage points to 13.8% from 29.7% in Q1 2025. Net income fell by more than half, dropping from $221.0M a year ago to $105.5M this quarter. Operating margin of 16.9% and operating income of $129.6M suggest the compression occurred at multiple levels of the income statement, not merely from one-time tax or interest items. This pattern indicates BioMarin’s growth is coming at significant cost, with expenses rising faster than revenue—a dynamic that undermines the quality of the top-line beat and explains why the market focused on the earnings miss despite the revenue outperformance.

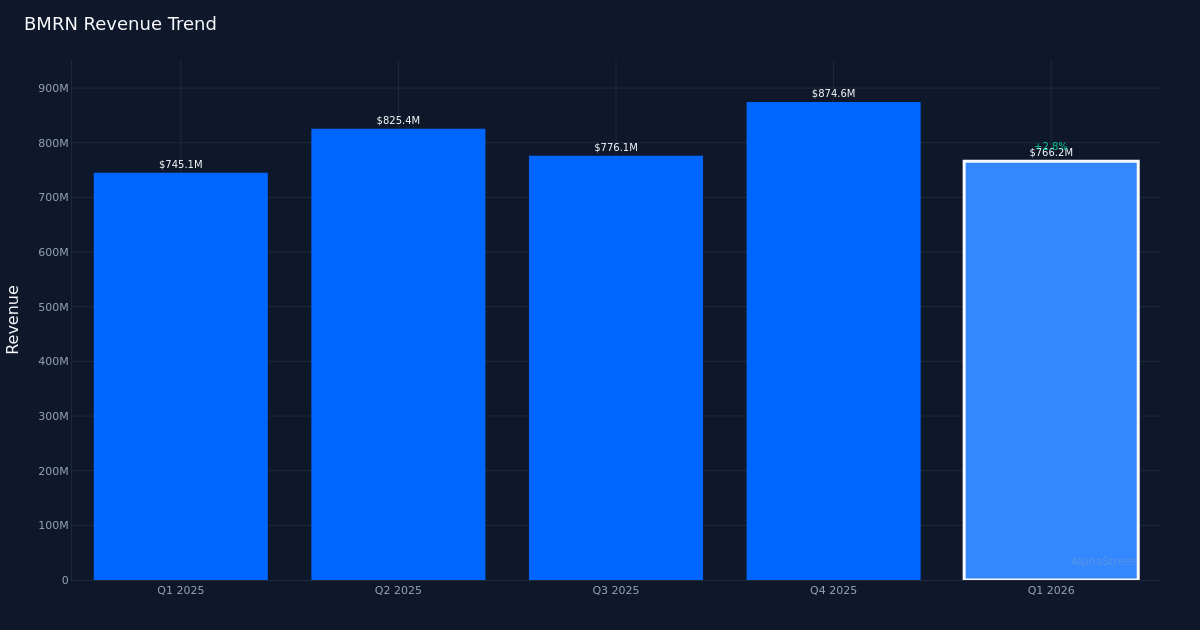

The four-quarter revenue trajectory shows erratic momentum rather than sustained acceleration. Quarterly revenue bounced from $825.4M in Q2 2025 to $776.1M in Q3 2025, then spiked to $874.6M in Q4 2025 before settling at $766.2M this quarter. This volatility complicates trend analysis, though the company maintained positive year-over-year growth of 2.8% last quarter and 3.0% this quarter. More telling is the profitability pattern: net income swung from $282.0M in Q2 2025 to $22.0M in Q3 2025, recovered to $89.0M in Q4 2025, and reached $105.5M in Q1 2026. The sequential improvement in net income provides some reassurance, but the wild swings across 2025 suggest operational volatility that management has yet to smooth out.

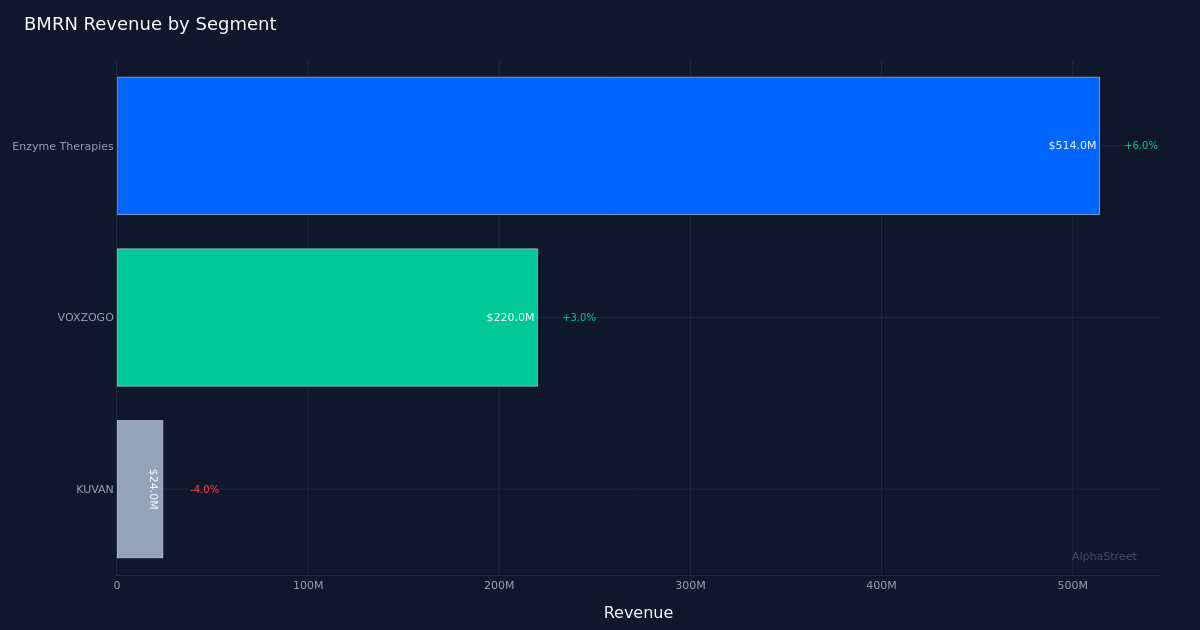

Segment performance reveals a stark mismatch between patient growth and revenue conversion, particularly in the VOXZOGO franchise. Enzyme Therapies delivered the strongest growth at 6.0% to reach $514.0M, representing two-thirds of total revenue and providing the foundation for the quarter’s performance. Management noted that “Total revenues in the first-quarter were $766 million and increased year-over-year, supported by increased patient demand across both Enzyme therapies and VOXZOGO.” However, VOXZOGO revenue of $220.0M grew only 3.0% despite a 20.0% increase in children treated with the therapy. This dramatic gap between patient volume growth and revenue growth demands explanation—either pricing pressures, payer mix shifts, or dosing changes are suppressing revenue per patient. Management acknowledged the disconnect, with one executive asking during the call to “help us bridge the disconnect between the 20% year-over-year patient growth in 1Q versus a 3% revenue growth.” KUVAN posted the weakest performance with $24.0M in revenue, down 4.0%, though its modest size limits overall impact.

Full-year guidance projects a dramatic acceleration that acquisition activity will drive rather than organic momentum. Management raised full-year revenue guidance to a range of $3.83B to $3.92B, with adjusted EPS guidance of $4.85 to $5.05 representing a midpoint of $4.95. The company emphasized that “The acquisition accelerates our anticipated year-over-year 2026 revenue growth to 20% at the midpoint of today’s updated guidance.” Management commentary during the call referenced that the guidance “increased by $500 million” and estimates “generated around $450 million in revenue for Galafold and POMOP in the comparable eight months last year and that implies low double-digit growth, around 11%.” The reliance on inorganic growth to hit the 20% target raises questions about the underlying health of the base business, particularly given the modest 3.0% organic growth this quarter and the margin pressure evident in the results.

The company’s execution track record provides little confidence, with zero earnings beats in the last quarter measured. BioMarin posted a 0% beat rate over the last one quarter on record, and year-over-year EPS declined 20.0% from $0.95 to $0.76. Operating cash flow of $220.7M provides some comfort regarding cash generation capability, but investors must weigh this against the profitability deterioration. The full-year EPS guidance midpoint of $4.95 implies significant improvement from the current quarterly run rate, requiring either margin recovery or meaningful contribution from acquired assets to achieve.

The market’s 2.6% positive reaction to a substantial earnings miss appears disconnected from fundamental results. The stock price of $55.46 moved higher despite the 20.8% EPS miss, suggesting investors are looking through near-term profitability challenges to focus on the revenue guidance raise and acquisition-driven growth narrative. This reaction may prove premature if the margin compression persists or if the VOXZOGO patient-to-revenue conversion issue reflects structural pricing pressure rather than temporary mix effects.

What to Watch: The critical metric for Q2 is whether net margin stabilizes or continues contracting—another quarter of margin compression would suggest structural cost issues rather than temporary factors. VOXZOGO’s revenue per patient trend will indicate whether the 20.0% patient growth can translate to meaningful revenue acceleration or if payer dynamics are capping monetization. Management must demonstrate that acquired assets can deliver the $450 million in revenue without adding proportional costs that further pressure margins. Finally, Enzyme Therapies must sustain mid-single-digit growth to offset weakness elsewhere, making franchise-level patient retention and pricing power essential to monitor.

This content is for informational purposes only and should not be considered investment advice. AlphaStreet Intelligence analyzes financial data using AI to deliver fast and accurate market information. Human editors verify content.