Doubling Down On Logistics And Banking Integration")

- In recent months, MercadoLibre reported past quarterly revenue of US$8.76 billion, growing about 44.6% year over year and beating analyst expectations, while simultaneously lowering free-shipping thresholds and expanding its delivery and advertising capabilities amid intensifying Latin American e-commerce competition.

- At the same time, the company has been pushing deeper into banking services for underbanked customers, a move that could reshape how its commerce, payments, and credit businesses reinforce one another across the region.

- Next, we’ll examine how MercadoLibre’s heavier investment in shipping perks and logistics affects its investment narrative and future profitability trade-offs.

Invest in the nuclear renaissance through our list of 91 elite nuclear energy infrastructure plays powering the global AI revolution.

MercadoLibre Investment Narrative Recap

To own MercadoLibre, you need to believe its e commerce, payments, and credit ecosystems can keep reinforcing one another across Latin America despite rising competition and margin pressure. The latest results show strong revenue and user growth, but also highlight the near term trade off between heavier logistics and shipping investments and profitability. For now, that investment focus does not change the main short term catalyst, which is continued monetization of its growing user base, or the biggest risk around credit and shipping economics.

The recent Q4 2025 report, with US$8.76 billion in revenue and modestly lower net income, is especially relevant here. It shows how lowering free shipping thresholds and scaling logistics can compress margins even as commerce and fintech volumes expand. That same quarter also underscored how MercadoPago and banking services for underbanked users could deepen engagement across the platform, reinforcing both the upside from higher transaction activity and the risk that rising fulfillment and credit costs might weigh more heavily than expected.

Yet investors should still be aware that rising logistics spend could collide with…

Read the full narrative on MercadoLibre (it’s free!)

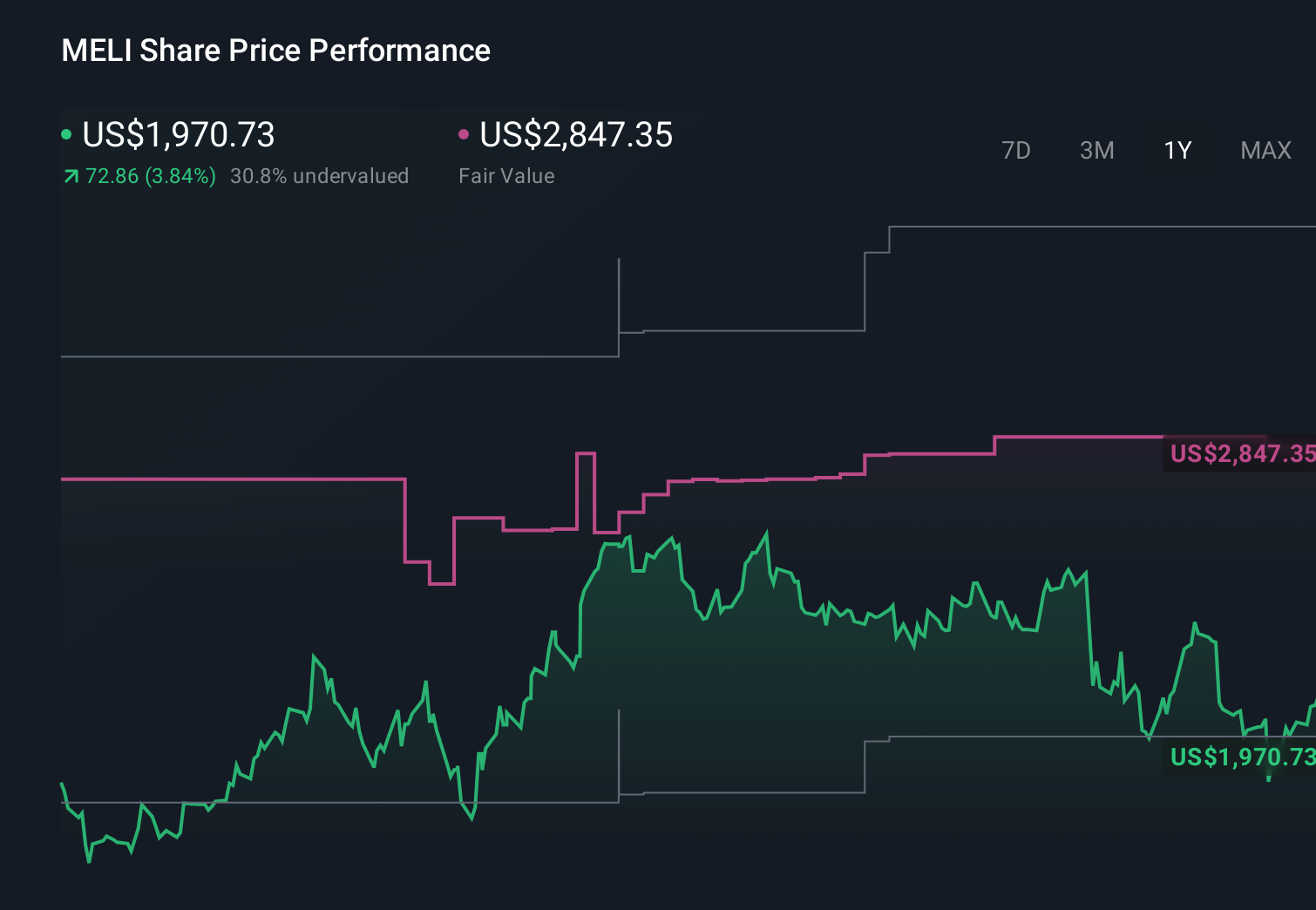

MercadoLibre’s narrative projects $46.9 billion revenue and $5.1 billion earnings by 2028. This requires 24.8% yearly revenue growth and a $3.0 billion earnings increase from $2.1 billion today.

Uncover how MercadoLibre’s forecasts yield a $2640 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were projecting revenue of about US$52.3 billion and earnings near US$5.9 billion by 2028, but this new step up in shipping benefits and logistics intensity could make those bullish margin and growth assumptions look either more achievable through scale or more stretched if costs bite harder, so it is worth comparing these upbeat views with more cautious takes on competition and credit risk.

Explore 28 other fair value estimates on MercadoLibre – why the stock might be worth just $1827!

Decide For Yourself

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Curious About Other Options?

Opportunities like this don’t last. These are today’s most promising picks. Check them out now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com