When US and Israeli forces struck Iran on February 28, 2026, the Gulf’s commercial aviation network nearly collapsed overnight. Emirates, Qatar Airways, and Etihad temporarily suspended operations, forcing passengers to seek alternative arrangements. Private jets quickly became one of the only dependable options, and prices reflected that shift almost immediately.

According to CNN, a group of twelve passengers flying from Muscat to Istanbul paid $145,000 for the trip, more than double the pre-conflict rate for the same route. Charter demand, according to Mayfair Jets chairman Ahmed Elhawary, surged between 200% and 300% within days of hostilities beginning.

More than a month after the onset of the crisis, flight tracking data captured at DWC on 8 April showed the airport continuing to see a varied business aviation mix, albeit in smaller numbers than usual: a San Marino-registered Gulfstream G450, a FlyAlliance Gulfstream IV, and an Embraer Lineage 1000 — one of the largest purpose-built private jets in commercial service — all recorded within 72 hours, when there would typically be at least a dozen movements during peacetime.

The busiest BizAv routes out of DWC ran to Hong Kong, Shanghai, and Karachi. With 416 total movements recorded over seven days, which is considerably more than other notable HNWI hubs like Paris-LBG, which sees an average of 32 daily movements. It is possible that this number does not reflect the true picture, however, as GPS jamming has made accurate readings challenging for services like FlightRadar24.

A Market That Was Already Popular Before the War

Before the war, the region showed signs of sustained demand. At the 2024 edition of MEBAA, the organisers had this to say about the market:

“As a leading hub for private jets, the Middle East and North Africa witnessed a record number of movements last year (16,657 aircraft movements in 2023), while the average net worth of private jet buyers in the Middle East is more than USD 1 billion. With the continued inflow of HNWIs into the UAE and Saudi Arabia, and increasing appreciation for luxury travel, the strategic importance of the region for business aviation is growing. In Saudi Arabia specifically, the market has witnessed record growth, with an 11% increase in private jet travel since 2020, and it’s expected to increase exponentially by 2030. Vista has already recorded strong growth in the Kingdom, seeing a 59% year-on-year increase.”

To respond to that increase in passenger traffic, Comlux and ExecuJet both unveiled new FBO terminals during MEBAA Show 2024.

New FBO openings are the reflection of a successful VIP scene; companies simply wouldn’t invest in new facilities if they couldn’t project a significant surge in traffic.

Dubai World Central and The Infrastructure Bet

In the UAE, the longer-term future is all about Al Maktoum International Airport, also known as Dubai World Central, where those two new FBO terminals are located. At the 2025 Dubai Airshow, the government announced a $34.8 billion expansion that would eventually give the airport five parallel runways and capacity for 260 million passengers annually, making it the largest aviation facility in the world by passenger capacity.

For business aviation, that kind of infrastructure commitment is a signal in itself. Operators and charter companies make long-term fleet and basing decisions based on exactly this sort of government intent, and the scale of the investment makes Dubai’s position as the region’s dominant BizAv hub difficult to challenge for the foreseeable future.

Saudi Arabia: The Underdog of BizAv in the Middle East

Under Vision 2030, the General Authority of Civil Aviation has set a target of growing the general aviation sector’s contribution to GDP tenfold, reaching $2 billion by 2030, with private charter and corporate aviation explicitly named as part of that plan. The broader Saudi aviation strategy is backed by $100 billion in public and private funding. Together with massive entertainment facilities like Six Flags Qiddiya, World Cup facilities, and car racing, the KSA is trying to replicate what was successful in Dubai. All of this will result in an increase in private aviation movements.

Where the Market Goes From Here

In April 2026, a two-week ceasefire between the US, Israel and Iran came into force, brokered by Pakistan and formalised as the Islamabad Accords. For the Gulf’s business aviation sector, the return of political stability is likely to mean a return of demand, but the timeline is harder to call than the infrastructure figures suggest.

Paradoxically, it was as a result of the 2003 invasion of Iraq that the region entered one of its most sustained economic booms, with Dubai at the forefront. For the Sheikhs of the UAE, the bet was that relative stability in an unstable region is an asset.

In 2026, the optics changed. This time, the missiles landed in the UAE itself. An Iranian drone struck an Amazon Web Services data centre in Dubai. Jebel Ali, the port that tripled its throughput in the two decades after 2003, suffered significant damage. No FBO terminal and no $34.8 billion airport expansion changes what those images have already done to the reputation of Dubai, and it will take years for trust to be restored.

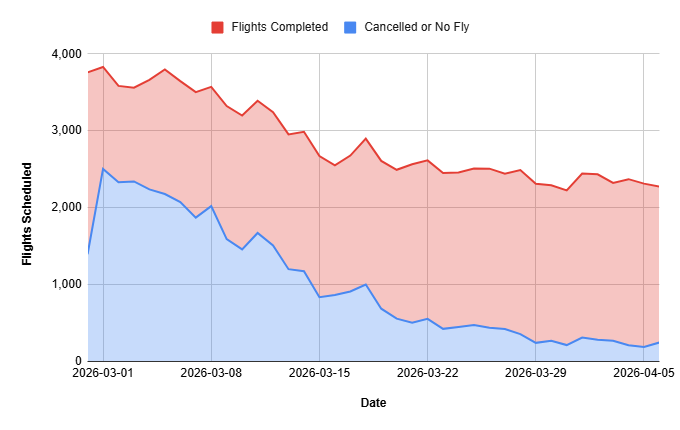

Completed vs. Cancelled Flights from Middle-East Airfields

Saudi Arabia, on the other hand, may recover faster. Riyadh and the major population centres were largely spared direct IRGC strikes during the worst of the crisis, and Vision 2030 seems largely unaffected. This will help the development of cities like the Red Sea, which are poised to become direct competitors to Dubai and Abu Dhabi.

It is important to note, however, that the situation continues to evolve rapidly at the time of publishing and that it is realistically impossible to accurately predict where private aviation will be in the GCC in the short to medium term.