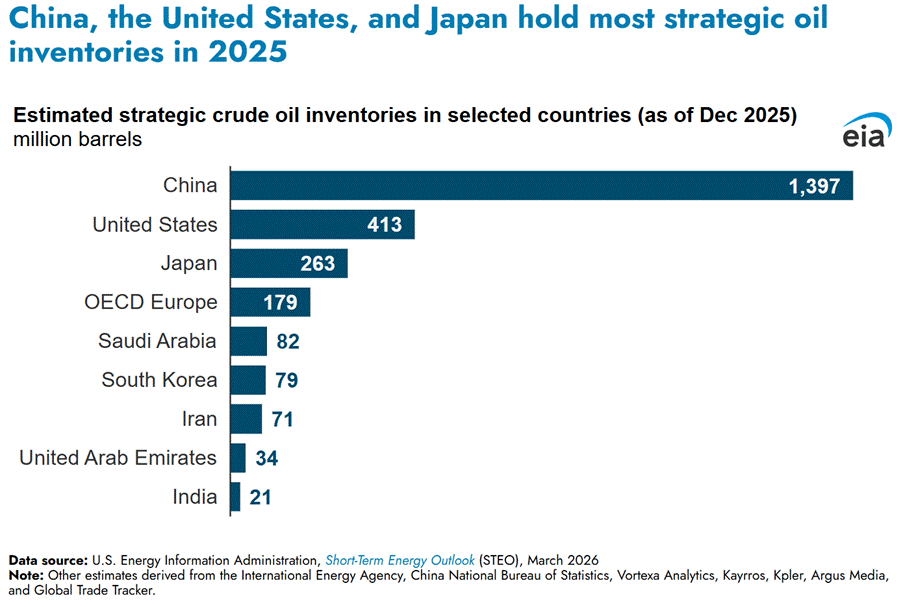

With the Strait of Hormuz effectively closed, India’s roughly 21 million barrels in reserves barely register against its exposure. China has nearly 1.4 billion.

The Strait of Hormuz is effectively closed. In March 2026, the International Energy Agency (IEA) triggered an emergency release of strategic oil stocks across member countries in response to the Iran conflict. For countries that import most of their oil and route most of it through that narrow waterway, this is a direct test of preparedness.

According to the U.S. Energy Information Administration (EIA), China, the United States, and Japan hold the world’s largest strategic oil inventories. The chart below is drawing much attention, especially in India. For two of the biggest oil importers, China and India, the crisis arrived at very different moments of preparedness. The longer Hormuz stays closed, the worse it gets for India.

China and India recognized the same vulnerability at roughly the same time in the early 2000s. Both made similar initial decisions. Their outcomes did not converge.

In 2004, the government approved India’s strategic petroleum reserve programme. It created a dedicated entity, the Indian Strategic Petroleum Reserves Limited (ISPRL), chose the sites, selected the technology, and secured the financing. By 2008, the government had already concluded that Phase I would not be sufficient and began planning a Phase II, identifying new locations at Chandikhol (Odisha) and Bikaner (Rajasthan), with expansion at Padur.

Building underground rock caverns for crude storage is complex. Building the institutional system to deliver them is harder. By the early 2010s, the caverns at three sites, Visakhapatnam, Mangalore, and Padur, were well advanced (90%+ complete). But they were not operational. Pipelines were incomplete and power connections lagged.

Visakhapatnam finally opened in 2015. Mangalore in 2016. Padur, the largest, in 2018. Together, this constituted Phase I – 5.3 million tonnes, or about 39 million barrels – of storage. Nearly fifteen years after the original decision.

Meanwhile, China was ploughing ahead. China began its program at roughly the same time. The first facility, at Zhenhai, was operational by late 2006. Three more, at Zhoushan, Huangdao, and Dalian, followed within two years. Together they held 102 million barrels, about a 33-day supply at the time. Analysts called it a drop in the bucket. China’s own stated ambition was 90 days of net imports, roughly 400 million barrels.

But China kept going. Phase II added 168 million barrels, with construction beginning in 2009. Notably, China shifted some sites inland, to Lanzhou in Gansu and Shanshan in Xinjiang, reducing dependence on coastal facilities vulnerable to disruption. When oil prices fell sharply in 2014-16, it accelerated purchases. By 2017, China reported nine operational sites. Phase III targeted a further 204 million barrels, with sites at Tianjin, Caofeidian, and Chongqing. By 2025, Beijing’s internal ambition had moved again. Now they want to build reserves of up to 2 billion barrels.

But India was stuck in a different gear – the slow one. If you think that 15 years to establish about 40 million barrels storage capacity is slow, Phase II is slower still. It remains in the planning stage, land acquisition remains painfully slow and the earliest India hopes to add meaningfully to its Phase I capacity is by 2030. This won’t be in time for the current crisis. According to ISPRL’s own data, India had 21.4 million barrels in its strategic reserve as of March 2025. For a country that imports more than 85 percent of its crude, that is a buffer measured in days.

The EIA estimates that China added an average of 1.1 million barrels per day to its inventories in 2025, reaching close to 1.4 billion barrels by December that year. That is more than three times its original stated ambition.

ISPRL’s annual reports tell the story. India treated Phase I as a celebratory milestone. Every annual report, including the 2025 one, starts with a discussion of the three sites commissioned between 2015 and 2018. For China, Phase I was the foundation for achieving enormous scale in subsequent years.

Filling the first cavern does not deliver energy security. That comes when capacity matches exposure. With the Strait of Hormuz effectively closed, India’s roughly 21 million barrels in reserves barely register against its exposure. China has nearly 1.4 billion. The gap between building and scaling is no longer a policy debate. It is the bill for not keeping pace.

Salman Soz is an economist, author, and deputy chairman of the All India Professionals’ Congress.

This article first appeared on the author’s Substack and has been republished with permission.

This article went live on April twenty-eighth, two thousand twenty six, at forty-one minutes past two in the afternoon.

The Wire is now on WhatsApp. Follow our channel for sharp analysis and opinions on the latest developments.