Thank you for opening your Chartbook email.

Caroline Walker, Theatre (2021)

Source: National Galleries

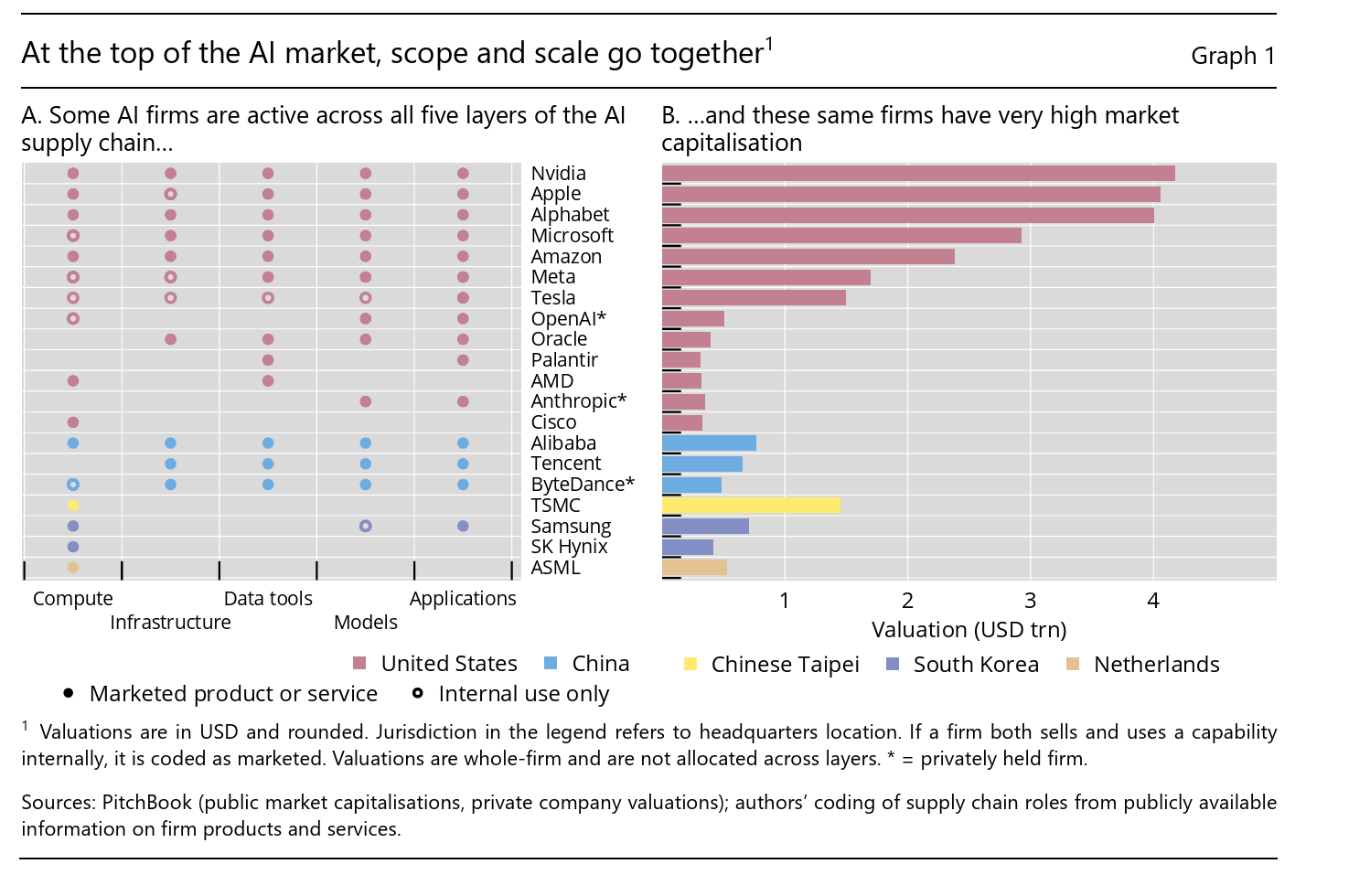

Alibaba and Bytedance are the only major non-US AI players that are present across all five layers of the AI stack.

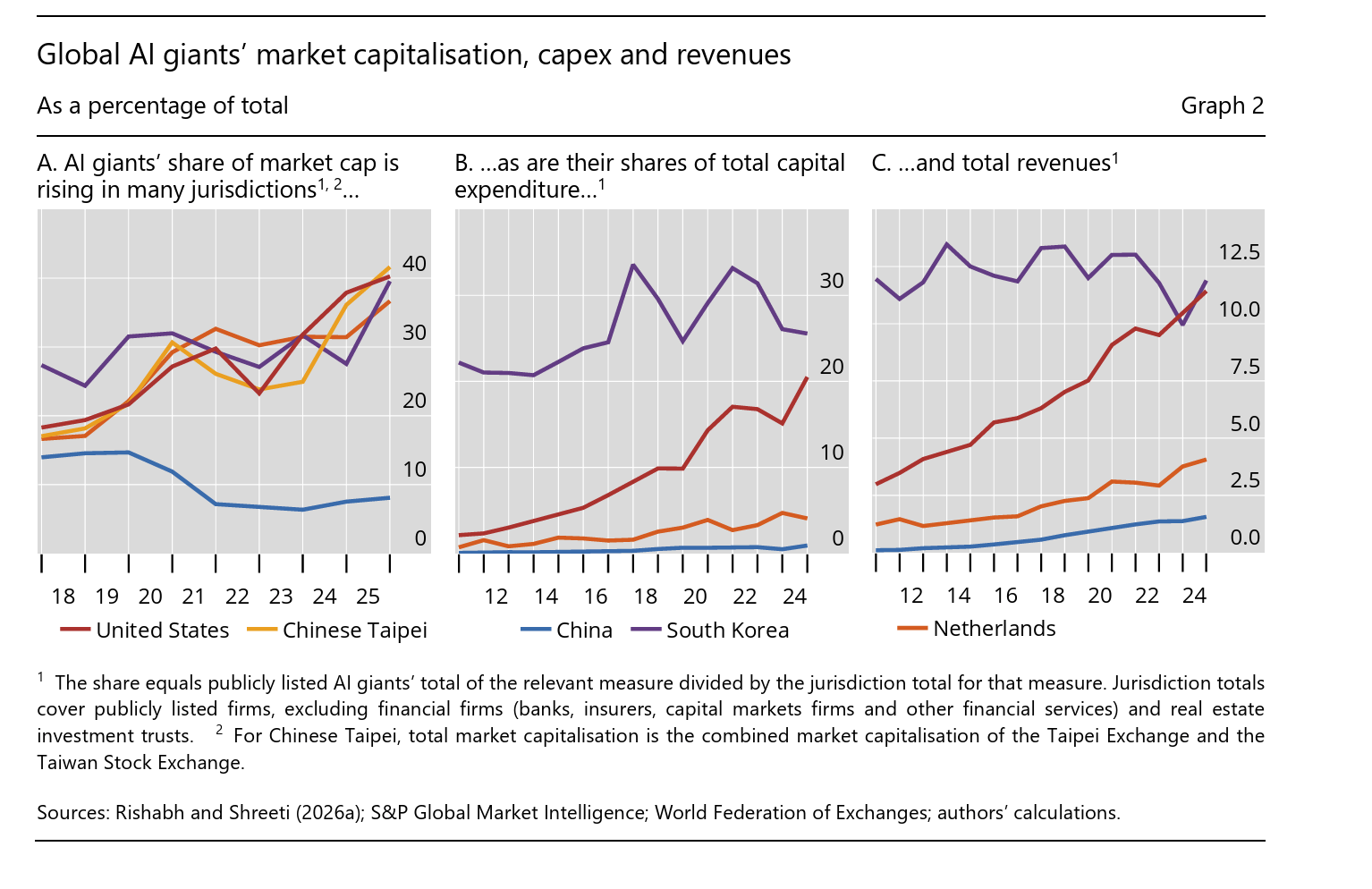

The difference between the US and China in the significance of AI in market cap, capex and revenues is increasingly dramatic.

Source: BIS

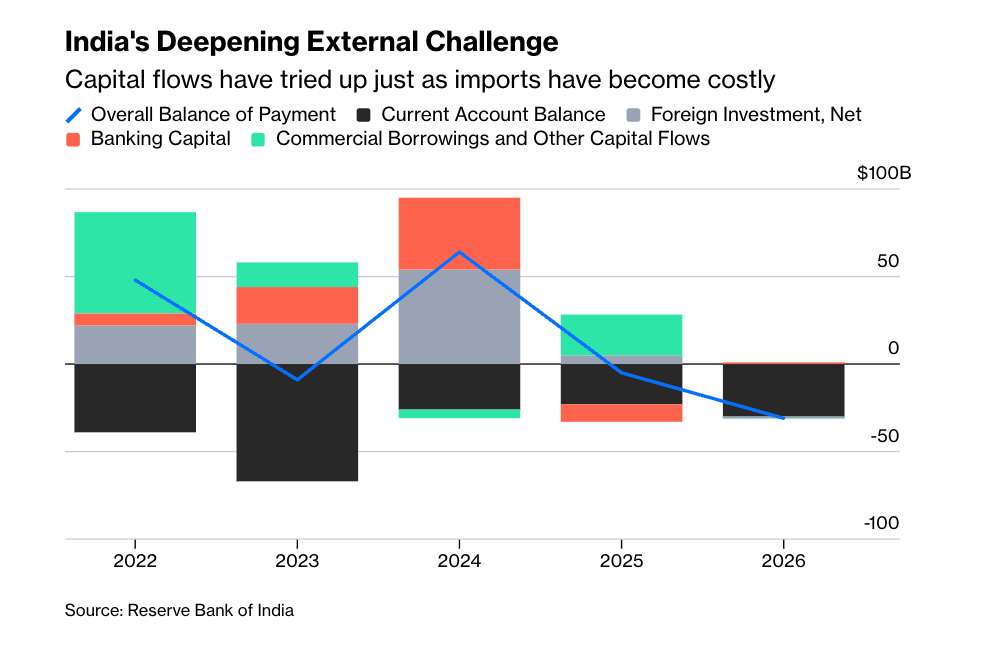

India is facing some seriously unpaletable choices

Money is leaving India at an alarming pace. Investment flows from overseas have dried up just as the Iran war has exploded the trade deficit. The rupee has taken a thrashing; official reserves are getting drained. A policy package to ward off a full-fledged currency crisis is on its way. Or at least that’s the market expectation, though there is considerable disagreement over exactly what should be in it. Taking cues from history, some have advocated overseas fundraising. State-run lenders have borrowed on New Delhi’s behalf during past external crises.

For instance, they scooped up $34 billion during the Federal Reserve’s 2013 taper tantrum, including $26 billion from the Indian diaspora abroad. Since the hole in this fiscal year’s balance of payments may be bigger than that entire package, why not run the program again? …

Where that history stops rhyming is in the cost of the cure. In the summer of 2013, five-year US interest rates had just climbed above 1%. So the 4% to 5% that the Reserve Bank of India allowed local banks to offer to nonresident Indians was attractive. (Wealthy NRIs further juiced up those returns by leveraging their bets — banks in Singapore, Hong Kong, London, and New York lent them funds to bail out their home country.)

Those benign conditions no longer exist. If New Delhi permits banks to pay even a 200 to 250 basis-point spread over US yields to incentivize the diaspora, the coupon rates would touch 6% to 6.5%, double State Bank of India’s current standard rate of 5-year dollar deposits. As for the really rich NRIs, sure they would still love some leverage — but to subscribe to the upcoming $75 billion public offering from SpaceX. It’s just a very different world from 2013.

Even if state-run lenders are somehow persuaded to raise expensive hard currency, what comes next may be too bitter a pill for them to swallow. Adding an annual 4.5% hedging cost to protect against a weaker rupee over three to five years would be a showstopper. They can raise money far cheaper at home. This problem was even bigger in 2013. Raghuram Rajan, who took over as RBI governor in September that year, engineered a controversial solution.

The central bank absorbed the risk of rupee depreciation so that commercial lenders’ future dollar repayments didn’t become too onerous. That’s what made the lenders go out and raise money hand over fist. If Sanjay Malhotra, the current central bank chief, tries to replicate the strategy — which Rajan himself later said he neither invented nor believed in — the RBI’s balance sheet will be exposed to a multi-billion-dollar loss upon maturity.

Shifting political realities may have dulled the appetite to take on such risks today. In 2013, Prime Minister Manmohan Singh’s government was resigned to losing power in less than a year. It could afford to leave future problems to the next administration. In contrast, Prime Minister Narendra Modi’s Bharatiya Janata Party, fresh off a string of important victories in state polls, is looking to rule for many more years. It has to be wary of costs that may come back to bite. … That leaves conventional solutions like raising interest rates. Low Indian rates are at the heart of the weak-rupee problem.

Because state-run refiners have still not been allowed to fully pass on the cost of fuel to consumers, domestic inflation is benign at 3.5% — nowhere near the double-digit levels of 2013. But why wait? A defensive rate hike or two could allay investors’ concerns that higher-for-longer borrowing costs later will bleed corporate profit margins. …

Malhotra and Modi need to get creative. It’s simply not politically palatable to let the exchange rate drop past the crucial psychological level of 100 to the dollar. To save the rupee, authorities may have no choice but to bite the bullet on domestic interest rates, and offer just enough tax sweeteners to keep global capital from slamming the door on its way out.

Source: Bloomberg

HEY READERS,

THANK YOU for opening the Chartbook email. I hope it brightens your day.

I enjoy putting out the newsletter, but tbh, what keeps this flow going is the generosity of those readers who clicked the subscription button.

Photo by Jakub Dziubak on Unsplash

If you are persuaded to click, please consider the annual subscription of $50. It is both better value for you and a much better deal for me, as it involves only one credit card charge. Why feed the payments companies if we don’t have to.

It’s all about derisking…

For contributing subscribers only.

Caroline Walker Picture Window

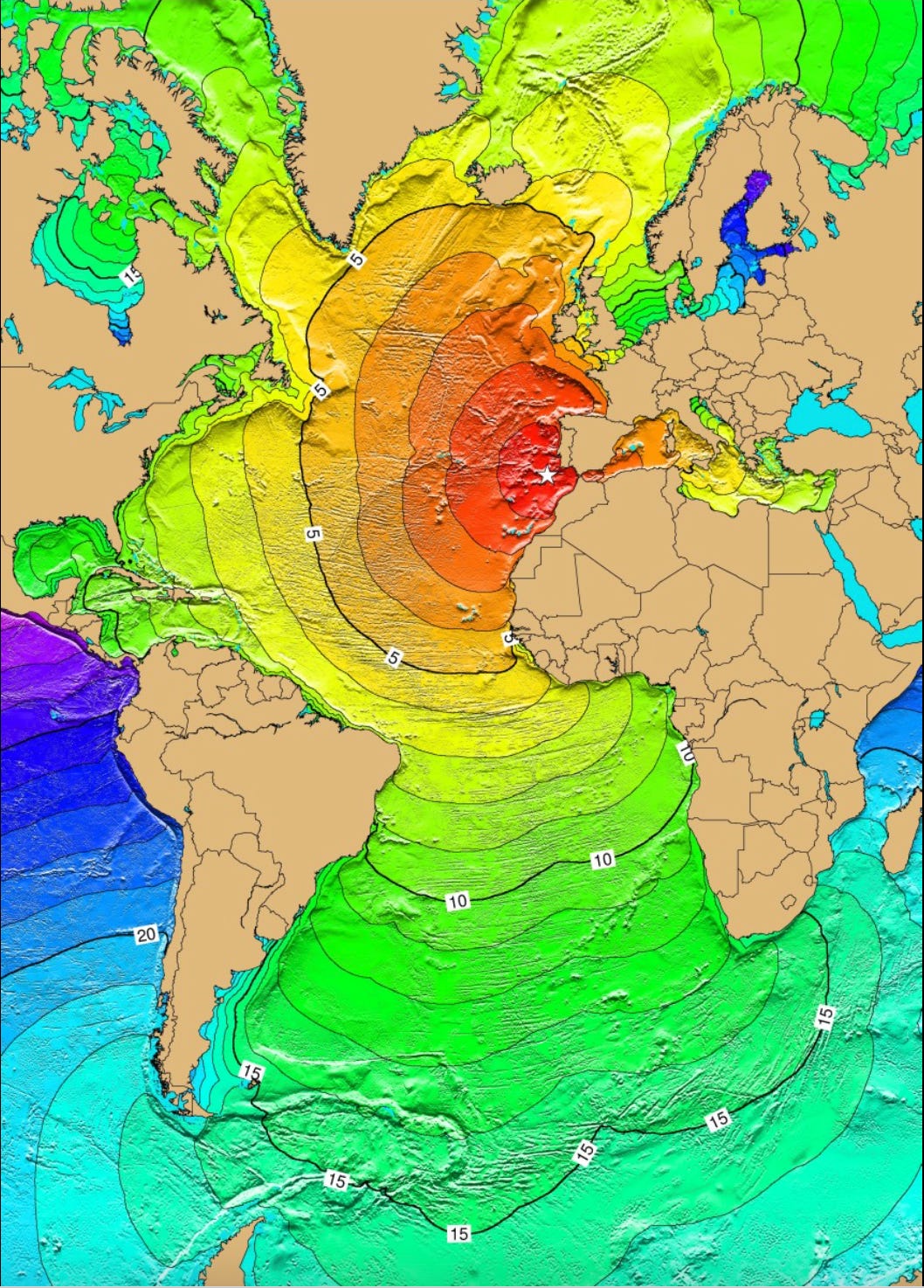

The “Lisbon earthquake” of 1 November 1755 was very much a Moroccan earthquake too, devastating the entire shoreline, including the town that would later become famous as Casablanca.

For some incredible Tsunami simulations see this fascinating paper:

This is really fascinating about Russia’s missile hardware.

Long Nights

By Jenny Xie

Ice, entire cakes of it.

Crows feed on sand.

So poor is this season

the ground steals color

from the tree-shadows.

•

Can it be that nothing

is as far as here?

Just look!

How much past we have

to cover this evening–

•

Come to think of it

don't forget to pick

off this self and that self

along the way.

Though that’s not right–

you spit them out like pits.

•

If there is a partition between

the outer and inner worlds,

how is it that some water in me churns

between the mountain ranges?

How is it we are absorbed so easily

by the ground—

•

Long nights for simple words.

•

Slant rhyme of current thinking

and past thinking.

A chewed over hour, late.

Where the long ago past

and the future come

to settle scores.

•

Traveling and traveling,

but so much interior

unpicked over by the eyes.

•

Nothing is as far as here.

Caroline Walker. A Scattering, 2011

If you’ve scrolled this far, you know you want to click: