Author | Jian, WuBlockchain

Summary

The JPEX incident is regarded as the largest crypto collapse in Hong Kong’s history. After the Securities and Futures Commission (SFC) issued a public warning in September 2023 about its unlicensed operations and the platform subsequently froze withdrawals, a surge of investor complaints and police arrests followed within days. Two years later, in November 2025, police formally charged 16 individuals and issued Red Notices for 3 core members, bringing total arrests to 80 and involving more than HKD 1.6 billion. The case exposes systemic risks stemming from unlicensed platforms and deceptive promotions, and has accelerated Hong Kong’s transition into a new phase of virtual asset regulation.

This article reviews the full scope of the incident, outlining its background, timeline, and impact, with the aim of offering a cautionary reference for investors.

On September 17, 2023, JPEX abruptly froze withdrawals. The Hong Kong Securities and Futures Commission (SFC) publicly warned that the platform was operating without a license, triggering widespread panic and a surge of police reports from investors. Just two days later, police made the first round of arrests, detaining eight individuals, including KOL Joseph Lam (over 150,000 followers on Instagram). Lam was suspected of luring people into investing in JPEX between July and September 2023 through false claims, including statements that the platform had obtained licenses in multiple jurisdictions and that he possessed exclusive insider information about JPEX, thereby inducing investors to deposit funds.

On September 22, 2023, Joseph Lam held a press conference regarding his alleged involvement in the JPEX cryptocurrency fraud case. Photo credit: HKFP.

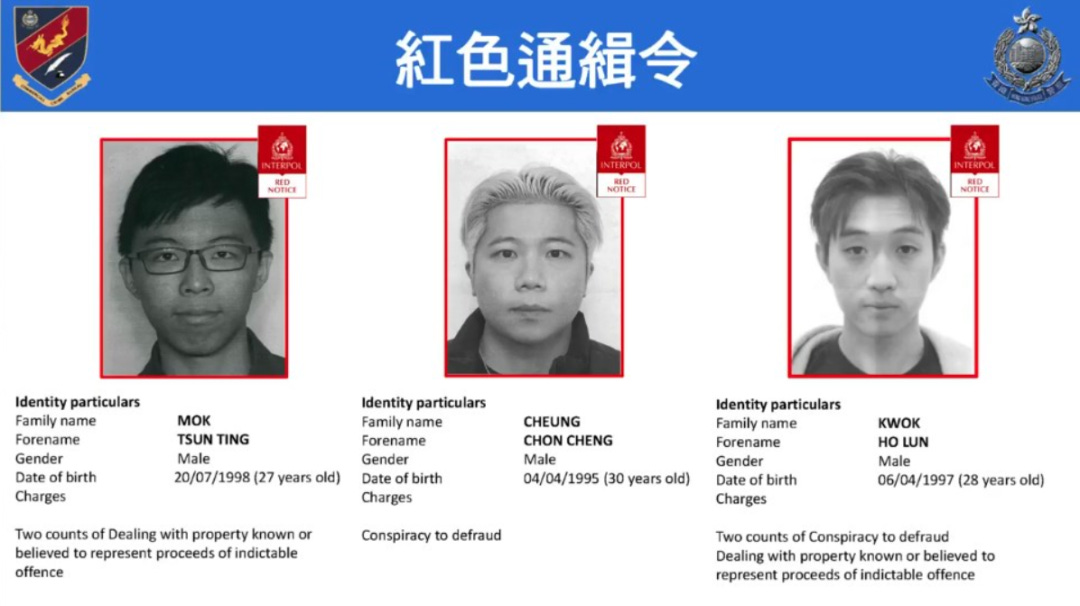

Two years later, on November 5, 2025, Hong Kong police formally charged 16 individuals, including Joseph Lam and YouTuber Chan Wing-yee (with over 100,000 followers), with conspiracy to defraud, money laundering, and obstruction of justice. Among them were six core JPEX members, seven OTC operators and KOLs, and three nominees who held accounts on behalf of others.Interpol issued Red Notices for three fugitives — 27-year-old Mo Chun-ting, 30-year-old Cheung Chun-shing, and 28-year-old Kwok Ho-lun — who have been identified as masterminds and have fled overseas.To date, the case has resulted in a total of 80 arrests, involving more than 2,700 victims and losses exceeding HKD 1.6 billion (approximately USD 206 million). Police have frozen HKD 228 million in assets, including cash, gold bars, luxury vehicles, and virtual assets. The incident exposed widespread misconduct in promoting unlicensed platforms and prompted regulators to tighten virtual asset oversight.

The Rise and Illusion of JPEX: High Returns, Fake Licenses, and Aggressive Promotion

Founded in 2020 and headquartered in Dubai, JPEX described itself as a “global cryptocurrency trading platform”. In Hong Kong, it aggressively promoted itself through large-scale advertising campaigns across MTR stations, bus bodies, and shopping mall façades, with some ads even labeling it as a “Japanese cryptocurrency exchange”.The platform claimed to hold financial licenses from the United States, Canada, Australia, and Dubai’s VARA. However, SFC investigations revealed that these “licenses” were limited to foreign exchange services and were not valid for virtual asset trading. Both Japan’s Financial Services Agency and Dubai VARA also clarified that JPEX was not authorized to operate.

JPEX’s main appeal came from its “Earn” products, which promised returns such as 20% APY on BTC, 21% on ETH, and 19% on USDT — extremely attractive yields that drew in large numbers of investors. The platform relied heavily on OTC shops and social media KOLs to create a “low risk, high return” narrative.Early SFC warnings showed that JPEX had already been suspected of making false statements as early as July 2023, yet its promotional activities continued up until the collapse

Regulations and Crisis: The Disorder of Unlicensed Operations Under Hong Kong’s New Regime

In June 2023, Hong Kong introduced the Virtual Asset Trading Platform (VATP) licensing regime, requiring all platforms to obtain approval from the Securities and Futures Commission (SFC) before offering services to retail investors. The framework was designed to balance innovation with risk control, yet JPEX never applied for a license and continued to operate illegally.

Beginning in July 2023, mainland Chinese users started reporting withdrawal difficulties. On Hong Kong’s popular forum LIHKG, complaints from mainland users about failed cash-outs began circulating, with some posts claiming that victims were lured to Hong Kong to “resolve issues in person” and were then ambushed.Police later confirmed an incident: a mainland Chinese man surnamed Yu, after failing to withdraw funds, was invited to a Hong Kong OTC shop to “resolve the issue”. After he entered Hong Kong, he was ambushed and assaulted on July 18 near Cambridge Plaza at the junction of San Wan Road and Cheung Yun Street in Sheung Shui. He suffered abrasions to his forehead and nose.Police subsequently listed four suspects as wanted: one Chinese national who was the head of an investment company, and three other Chinese men aged around 30 to 40, each around 1.7 meters tall, wearing black shirts and black pants, with no further details available.These incidents spread quickly, fueling collapse rumors as early signs of liquidity problems emerged behind the platform’s high-return promises. Internal SFC investigations showed JPEX was suspected of making false statements, yet its promotional campaigns continued until the eve of its downfall.

Mr. Yu, a JPEX user, was assaulted by multiple individuals (photo provided by the interviewee). Photo credit: hk01.com

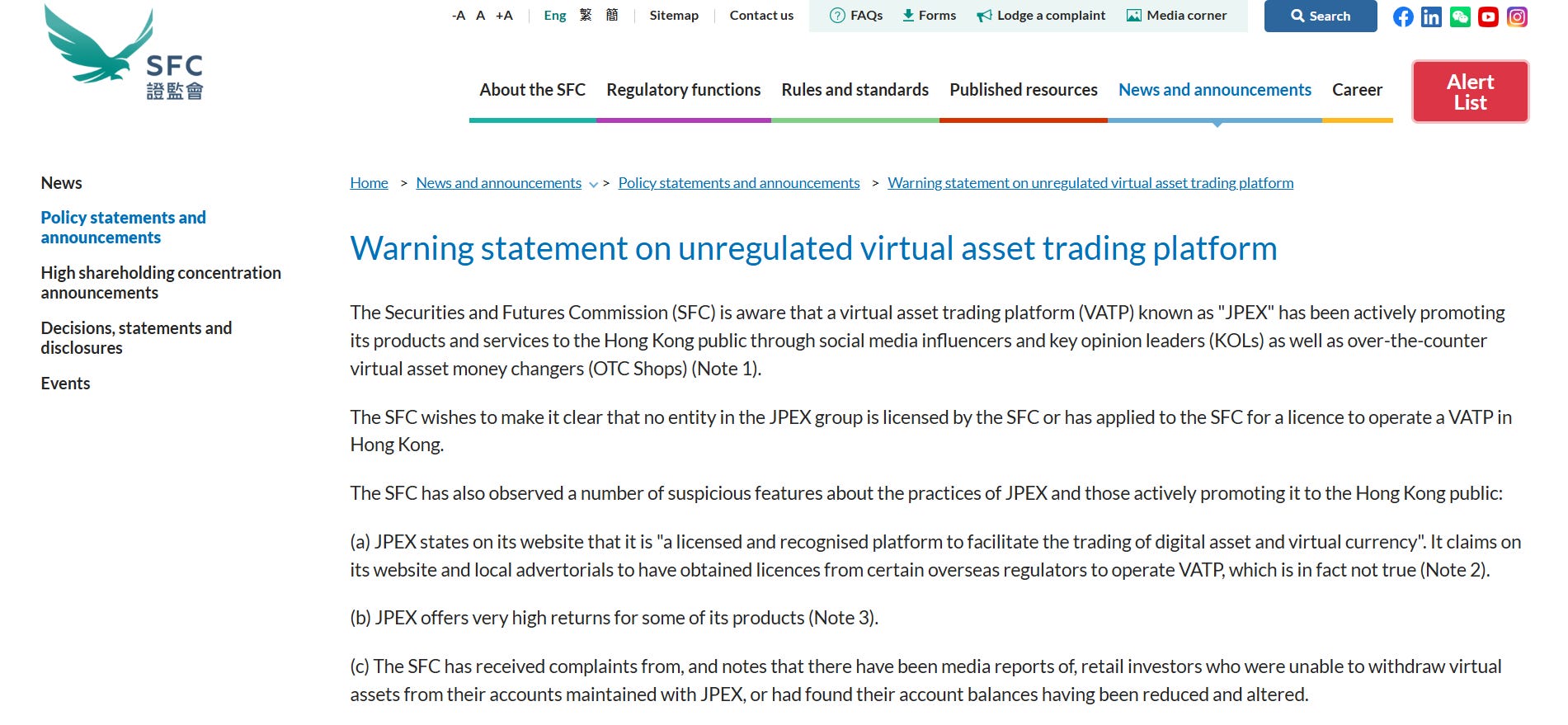

On September 13, 2023, the Hong Kong Securities and Futures Commission (SFC) issued a public warning concerning JPEX, titled “Warning Statement on Unregulated Virtual Asset Trading Platform”. The statement directly pointed out that JPEX was operating without a license, violating the VATP licensing regime that came into effect on June 1. It highlighted that JPEX had falsely promoted itself through social media influencers and KOLs (such as Instagram sponsored posts) as well as OTC shops, claiming to hold financial licenses from the United States, Canada, Australia, and Dubai’s VARA.SFC investigations showed that these “licenses” were in fact limited to foreign exchange services and were not valid for virtual asset trading.The statement emphasized that JPEX had already been placed on the SFC’s Alert List on July 8, 2022. Its products, such as the Earn service — which promised returns of 21% APY on ETH, 20% on BTC, and 19% on USDT — were suspected of being “deposit/return” arrangements, amounting to potential illegal fundraising. Numerous retail investors had also lodged complaints regarding failed withdrawals or financial losses.The SFC instructed all KOLs and OTC shops to immediately cease promoting JPEX and all related services and products.

Photo credit: Hong Kong Securities and Futures Commission (SFC)

Within hours of the statement’s release, JPEX quickly issued a response on its official website and blog, claiming that the SFC’s actions “have unfairly pressured us to consider withdrawing our licence application in the Hong Kong region and to adjust our future policy development accordingly. The SFC should bear full responsibility for undermining the prospects of cryptocurrency development in Hong Kong”.In a blog post, JPEX asserted that it had publicly announced as early as February 2023 its intention to apply for a cryptocurrency trading licence in Hong Kong, describing the city as a key market. However, it claimed that the SFC’s warning “conflicts with Web3 policy”, and that it was considering withdrawing its Hong Kong licence application and adjusting its regional strategy.This response further heightened investor panic. The number of complaints surged from several hundred before the SFC statement to more than 1,600, and many users rushed to OTC stores seeking assistance. This made the platform’s liquidity crisis fully visible, marking the moment when the incident shifted from regulatory warning to the brink of collapse.

On September 17, 2023, JPEX published an announcement on its official blog stating that its third-party market makers had “maliciously frozen” the platform’s funds, further intensifying the liquidity crisis. The announcement accused Hong Kong regulators of “unfair treatment”, claiming that regulatory pressure and negative news coverage prompted market makers to demand additional information, restrict liquidity, and significantly increase operating costs, which in turn caused operational difficulties.JPEX stressed that the issue did not originate from the platform itself but was the result of external factors. It pledged to restore liquidity and gradually adjust fees. The announcement also confirmed that its Earn services — high-yield products in which users deposited assets to earn returns (such as 20% APY on BTC) — would be fully delisted from trading on September 18, and users would no longer be able to place new orders.This move signaled the shift from an SFC regulatory warning to a public meltdown, intensifying user panic and confirming that the crisis had entered a critical stage.

More notably, JPEX raised the USDT withdrawal fee from the original 10 USDT to 999 USDT (with a maximum withdrawal limit of 1,000 USDT), meaning users were effectively able to withdraw only 1 USDT. This move was widely viewed as a “de facto freeze” of user assets, sparking strong dissatisfaction and heated discussion across social media, with many describing it as “an indirect rug pull”.JPEX claimed that the adjustment was made to “respond to business changes”, but provided no timeline for when normal withdrawal fees would be restored.

Screenshot from a JPEX user showing the USDT withdrawal fee raised to 999 USDT (with a maximum withdrawal limit of 1,000 USDT)

Full Collapse and Police Crackdown: KOL Arrests and Asset Freezes

On September 18, 2023 — five days after the SFC issued its warning — the Commercial Crime Bureau (CCB) of the Hong Kong Police launched a coordinated operation codenamed “Iron Gate”, arresting the first batch of eight individuals. Those arrested included Instagram KOL Joseph Lam (with 150,000 followers, a former Oxford-trained lawyer turned insurance agent), investment YouTuber Chan Wing-yee (with over 100,000 followers, a former TVB actress turned investment content creator), and OTC shop operators such as Felix Chiu (owner of Coingaroo).Police raided 20 locations, seizing cash, computers, and documents. By that day, 1,641 victims had filed police reports, with losses totaling approximately HKD 1.2 billion.According to police, JPEX constructed an image of being “safe and easy to use” through KOLs and OTC shops, while user funds were transferred through multiple wallets for laundering. Police alleged that between July and September, Joseph Lam falsely claimed through Instagram posts, seminars, and livestreams that JPEX was “safe and licensed” (including supposed regulatory approvals from several jurisdictions) and that he possessed “exclusive insider information”, inducing investors to deposit assets and ultimately suffer losses.The arrests marked the escalation of the incident into a full criminal investigation. The SFC praised the police operation and reiterated that KOLs must perform due diligence on the platforms they promote.

In October 2023, the number of arrests in the JPEX investigation conducted by Hong Kong police increased to 28, including 28-year-old KOL Henry Choi Hiu-tung, founder of Hong Coin. Choi was accused of conspiracy to defraud by promoting JPEX’s high-return Earn products through his social media pages “Hong Coin” and “TungClub”, and by collaborating with OTC shops to funnel user funds onto the platform.By October, the number of reported victims had exceeded 2,530. The SFC highlighted serious loopholes in KOL-driven promotions, noting that many influencers, including Choi, failed to conduct due diligence on the platform’s qualifications, yet repeatedly claimed that JPEX was “safe and licensed”, in violation of the SFC’s disclosure requirements.The case also extended to Taiwan, triggering cross-border discussion. Taiwanese police interviewed multiple KOLs and began cooperating with Hong Kong’s SFC to trace the flow of funds.

Latest Development: First Formal Prosecutions and Red Notices in the JPEX Case

On November 5, 2025, the Commercial Crime Bureau (CCB) of the Hong Kong Police formally charged 16 individuals, marking the first official prosecutions in the JPEX case in two years and signaling the start of criminal proceedings.The defendants include six core JPEX members, seven OTC operators and KOLs, as well as public figures such as Joseph Lam and Chan Wing-yee. At a press conference, Chief Superintendent Ernest Wong stated that this was the first round of prosecutions in the JPEX investigation, with charges involving conspiracy to defraud, money laundering, obstruction of justice, and inducing others to invest in virtual assets through fraudulent means or with reckless disregard for the consequences.The prosecution focuses on allegations that the defendants used false advertising and an OTC network to induce more than 2,700 investors to deposit funds, while the platform operated without a licence and was involved in laundering illicit proceeds.

On the same day, the International Criminal Police Organization (Interpol) issued Red Notices for three fugitives who were identified as masterminds and core members of the operation and had already fled overseas: 27-year-old Mok Tsun-ting, 30-year-old Cheung Chon-cheong, and 28-year-old Kwok Ho-lun.Police stated that the three individuals orchestrated fund transfers and money-laundering activities, and that their related assets had already been frozen. The Red Notices call on all Interpol member countries to assist in their arrest.To date, the JPEX case has resulted in 80 arrests, with more than 2,700 victims and total losses amounting to HKD 1.6 billion.

On November 6, 2025, the 16 defendants — including Joseph Lam and Chan Wing-yee — appeared at the Eastern Magistrates’ Courts. Fourteen of them were granted bail, with amounts ranging from HKD 20,000 to HKD 100,000; both Lam and Chan were each granted HKD 300,000 bail. All defendants were required to surrender their travel documents and report to police regularly.This case is one of Hong Kong’s largest fraud cases in recent years in terms of both the number of victims and the scale of losses. Authorities have frozen HKD 228 million in assets, including cash, gold bars, luxury vehicles, and virtual assets.

Follow us

Twitter: https://twitter.com/WuBlockchain

Telegram: https://t.me/wublockchainenglish