Labor Peace and ESG Push Hint at a Sharper Strategic Focus?")

- Orla Mining recently resolved its outstanding 2025 productivity bonus dispute with employees and the union at the Camino Rojo Mine, formalizing the agreement before the Mexican Labour Authority and reaffirming the existing Collective Bargaining Agreement.

- The company also released its 2025 Sustainability Report, underscoring progress on ESG-linked goals, Indigenous education partnerships, emissions intensity, and safety performance, which reinforces its responsible mining profile.

- With the Camino Rojo labor agreement in place, we’ll now explore how this development influences Orla Mining’s existing investment narrative.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

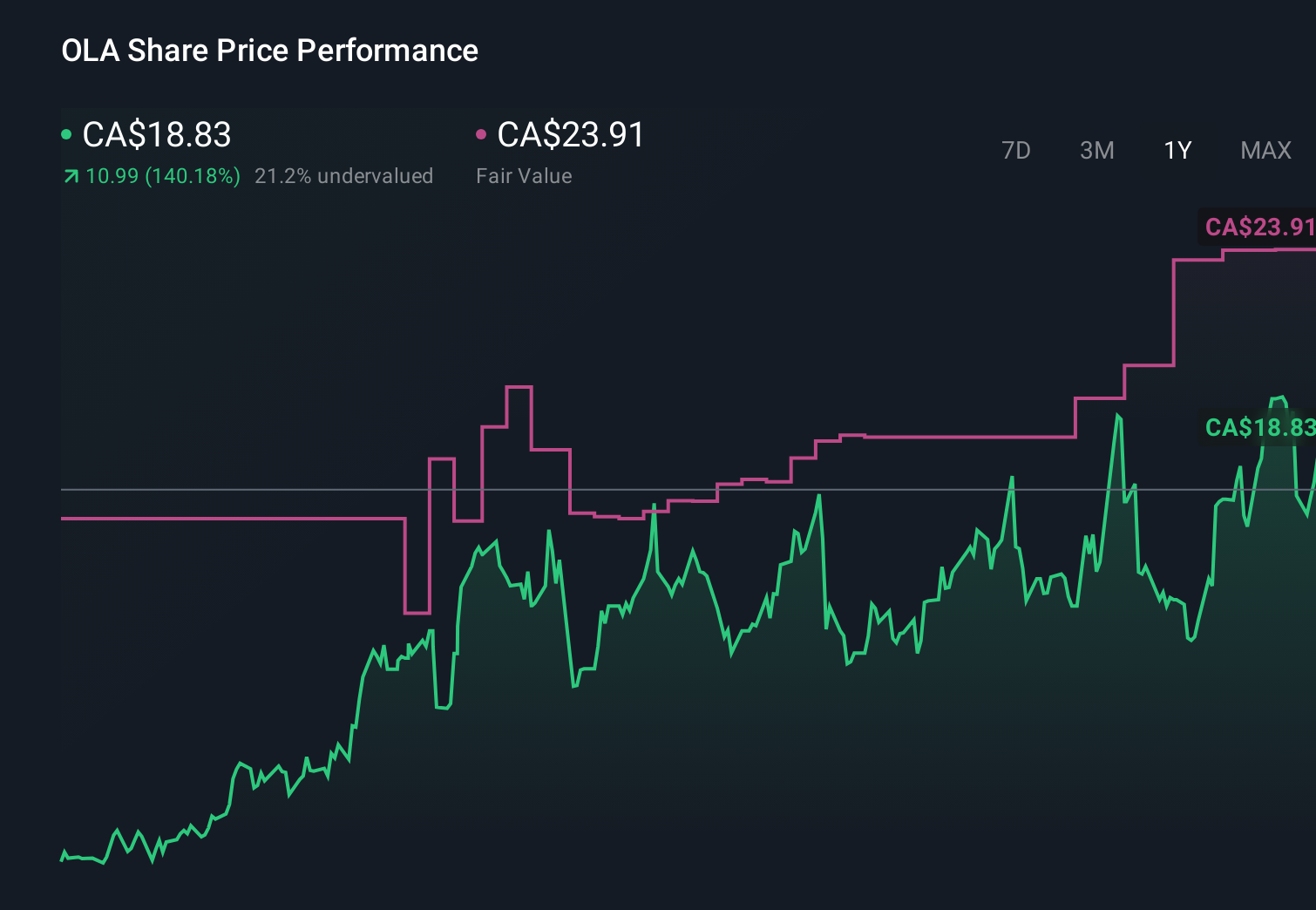

Orla Mining Investment Narrative Recap

To own Orla Mining, you need to believe in its ability to keep Camino Rojo running reliably while advancing its broader North American growth pipeline. The recent resolution of the 2025 productivity bonus dispute at Camino Rojo reduces near term labor uncertainty, but does not materially change the core near term catalyst, which remains stable production and cost control at Camino Rojo, nor the key risk around operational and jurisdictional disruption at this flagship asset.

The 2025 Sustainability Report release sits closely alongside the Camino Rojo labor agreement, as both touch on how Orla manages people, communities, safety, and environmental performance at its operations. In my view, this ESG disclosure is most relevant to the long term catalyst that depends on permits and community support for Camino Rojo’s expansion and South Railroad, because credible progress on emissions, safety, and Indigenous partnerships can influence access to capital and stakeholder confidence in future projects.

Yet while the bonus dispute is now resolved, the broader risk around future labor tensions and jurisdictional stability at Camino Rojo is something investors should be aware of…

Read the full narrative on Orla Mining (it’s free!)

Orla Mining’s narrative projects $2.1 billion revenue and $1.1 billion earnings by 2029.

Uncover how Orla Mining’s forecasts yield a CA$31.98 fair value, a 122% upside to its current price.

Exploring Other Perspectives

Before this labor news, the most optimistic analysts were assuming Orla could reach about US$1.8 billion in revenue and roughly US$960.6 million in earnings by 2028, which is far more bullish than the consensus view. Those forecasts leaned on smooth execution at projects like Camino Rojo Underground, so this recent labor development could either support their thesis or prompt a rethink, depending on how you weigh the risk of further disruptions.

Explore 7 other fair value estimates on Orla Mining – why the stock might be worth just CA$17.26!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Orla Mining research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Orla Mining research report provides a comprehensive fundamental analysis summarized in a single visual – the Snowflake – making it easy to evaluate Orla Mining’s overall financial health at a glance.

Curious About Other Options?

Don’t miss your shot at the next 10-bagger. Our latest stock picks just dropped:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com