Fast-growing companies whose revenue and earnings increase at a faster pace than the broader market can help investors generate market-beating returns. These high-growth companies can achieve impressive growth rates for a variety of reasons, including launching competitive products, dominating lucrative markets, expanding into new areas, or creating new markets.

Nvidia (NVDA 1.56%) is one such high-growth company that has been in impeccable form on the stock market in recent years. Its terrific returns have been fueled by its dominant stature in the artificial intelligence (AI) chip market. What’s more, Nvidia is trading at a really attractive valuation even after rising an incredible 655% over the past three years.

In fact, it may be the smartest growth stock to buy right now if you have just $200 in investible cash. Let’s look at the reasons why.

Image source: Nvidia.

Nvidia’s market-beating growth is set to continue

Nvidia recently released fiscal 2026 fourth-quarter results (for the period ending Jan. 25, 2026). Its annual revenue increased by 65%, while adjusted earnings were up by 60%. The company’s guidance makes it clear that it is poised to grow at a faster pace in fiscal 2027.

Today’s Change

(-1.56%) $-2.87

Current Price

$180.28

Key Data Points

Market Cap

$4.4T

Day’s Range

$179.94 – $186.10

52wk Range

$86.62 – $212.19

Volume

6M

Avg Vol

175M

Gross Margin

71.07%

Dividend Yield

0.02%

Nvidia’s $78 billion revenue guidance for the current quarter points toward a potential jump of almost 77% over the year-ago period’s reading. The company is also anticipating an increase of 3.7 percentage points in its non-GAAP gross margin, indicating that its earnings growth is likely to accelerate as well.

The company’s improving growth profile can be attributed to persistent investments in AI infrastructure, such as data centers, with major hyperscalers buying billions of dollars’ worth of Nvidia’s chips to run AI workloads in the cloud. Importantly, Nvidia continues to be a dominant player in this market, with a share of 81%, and it isn’t giving rivals much room to make any progress.

Nvidia’s focus on launching cutting-edge processors that can significantly reduce the cost of AI model training and inference, along with its solid control over the supply chain, are the primary reasons why it is the kingpin of the AI semiconductor ecosystem. It is set to become the largest customer of foundry giant Taiwan Semiconductor Manufacturing in 2026, supplanting Apple. Nvidia has reportedly told TSMC that it will have to double its capacity to meet its demands over the next decade.

Again, that isn’t surprising as investments in data centers are expected to increase at an annual rate of 40% through 2030, creating a potential addressable revenue opportunity of $3 trillion to $4 trillion for Nvidia.

Stronger growth should lead to more gains

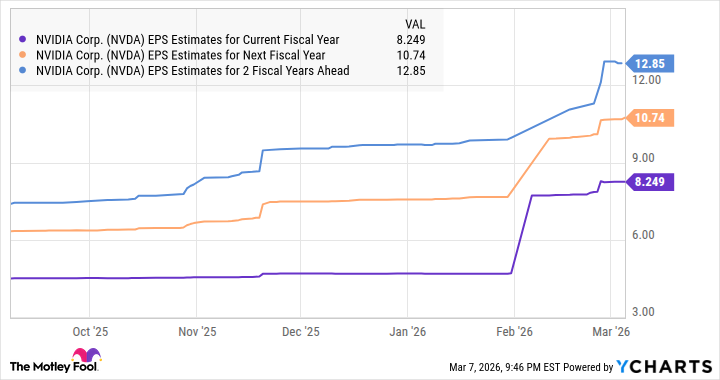

Analysts have significantly raised their earnings growth expectations for Nvidia following its latest report.

NVDA EPS Estimates for Current Fiscal Year data by YCharts

This impressive growth in Nvidia’s earnings is likely to be rewarded with more upside, especially considering that it trades at an attractive 22 times forward earnings. Assuming Nvidia stock trades at 24.4 times earnings after three years (in line with the tech-laden Nasdaq-100 index’s forward multiple), it could jump to $313 (based on the projected earnings of $12.85 per share as seen in the chart above).

That’s a potential jump of 76% from current levels, which makes Nvidia an ideal growth stock to buy right now with just $200 in investible cash.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, Nvidia, and Taiwan Semiconductor Manufacturing and is short shares of Apple. The Motley Fool has a disclosure policy.