Upstart stock is way down from its 52-week high, but the sell-off might be overdone.

Banks have relied on Fair Isaac‘s FICO credit scoring system for over 30 years to help determine the creditworthiness of loan applicants. It considers five factors, including their repayment history and their existing debts. However, Upstart Holdings (UPST 1.44%) believes the FICO score is far too simplistic, causing banks to potentially pass over some high-quality customers.

Upstart has developed an algorithm that uses artificial intelligence (AI) to rapidly analyze over 2,500 data points for each applicant, providing what it claims is a better sense of the applicant’s ability to repay a loan. The company licenses the algorithm to a growing number of banks, credit unions, and other lenders, and it earns a fee every time a loan is successfully originated.

Upstart stock declined by 62% over the last 12 months, in part because investors are growing increasingly worried about a potential bubble in the AI space. However, Upstart is growing its revenue at a lightning-fast pace, and it’s one of the only pure-play AI companies actually turning a profit. That sets up a potential opportunity for investors.

Here’s why I predict Upstart’s stock price will double before the end of 2026.

Image source: Getty Images.

AI is the way forward for lending

During the fourth quarter of 2025 (ended Dec. 31), Upstart’s algorithm handled 91% of all applications autonomously with no human intervention. Since AI is doing the grunt work, approvals are typically determined instantaneously, whereas it would take a human loan assessor days or even weeks to analyze the same amount of data and come to a decision.

Upstart’s approach is proving extremely popular with both consumers and lenders. The company originated 455,788 loans during the fourth quarter, an eye-popping 86% growth over the year-ago period. Unsecured personal loans are Upstart’s specialty, accounting for $2.9 billion of its $3.2 billion in total originations during the period.

However, the company’s car and home equity line of credit segments both grew fivefold during the quarter, so although they are still small parts of the overall business, it won’t be long before they are making significant contributions.

The loans originated by Upstart’s algorithm already perform very well, but the company continues to improve the performance of its AI models, which will be the key to winning even more originations in the future. It introduced a series of updates during the fourth quarter that increased the algorithm’s accuracy while also reducing potential default rates even further, an attractive combination for banks.

Last year, Upstart chairman Dave Girouard said he expects AI to replace all human-driven credit assessment within the next decade. More than $25 trillion worth of loans are originated globally every year across all segments, and they generate roughly $1 trillion in fee income, so this is a substantial financial opportunity for Upstart.

Today’s Change

(-1.44%) $-0.46

Current Price

$31.51

Key Data Points

Market Cap

$3.1B

Day’s Range

$31.43 – $32.83

52wk Range

$29.61 – $88.69

Volume

160K

Avg Vol

4.9M

Gross Margin

97.62%

Upstart’s revenue and profit surged in 2025

Upstart generated a record $1.043 billion in revenue during 2025, topping management’s most recent forecast of $1.035 billion. The result represented a whopping 64% increase from the previous year, which marked an acceleration from the 24% growth the company produced in 2024.

Upstart increased its operating expenses by only 23% last year, so it also managed to convert its top-line momentum into a very strong outcome on the bottom line. The company generated $53.6 million in net income according to generally accepted accounting principles, a huge positive swing from its net loss of $128.6 million in 2024.

The result looks even better after one-off and noncash expenses are stripped out, with Upstart’s adjusted earnings before interest, tax, depreciation, and amortization surging by 2,074% to $230.5 million.

Upstart stock could double from here

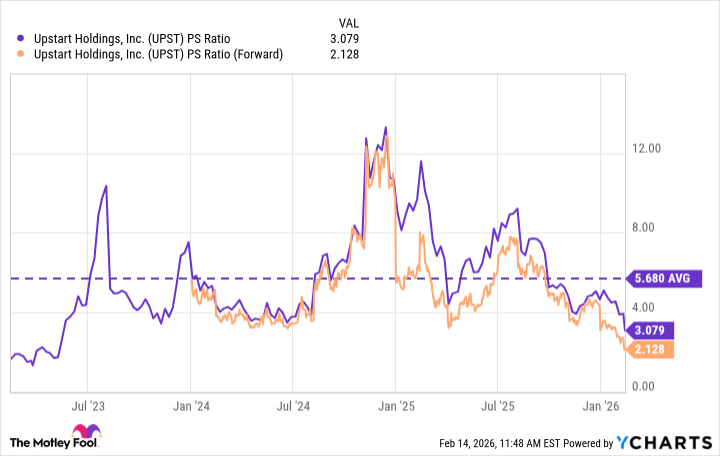

Based on Upstart’s 2025 revenue and its current market capitalization of $3 billion, its stock is trading at a price-to-sales (P/S) ratio of just 3.1, a steep discount to its three-year average of 5.7.

But the stock looks even cheaper when measured against its future potential revenue. Wall Street’s consensus estimate (provided by Yahoo! Finance) suggests Upstart could bring in $1.4 billion during 2026, placing its stock at a forward P/S ratio of just 2.1.

Data by YCharts.

That implies Upstart stock would have to soar by 171% before the end of 2026 just to trade in line with its three-year average P/S ratio of 5.7. I’m not suggesting that will happen, but the stock could fall way short and still double.

The stock was trading at $30.68 at the close on Friday, Feb. 13, so a gain of 100% would result in a price of $61.36. It was trading at that level as recently as September of last year, so it’s certainly a realistic potential outcome.

However, I would encourage investors to stay focused on the long term, because the stock might do even better if all loan assessment methods really are replaced by AI over the next decade as Upstart expects.