Eli Lilly (NYSE: LLY) has been an exceptional growth stock to own in recent years. Its popular GLP-1 treatments, Zepbound and Mounjaro, have been in high demand, and they are amassing billions in revenue for the business. Investors and analysts continue to expect much more growth from them in the future.

However, with Eli Lilly’s valuation at around $900 billion today, expectations are also sky-high. That can make it difficult for the stock to impress investors and generate strong returns in the future. Is Eli Lilly’s stock priced at too much of a premium to be a good buy right now, or is there still room for it to rise even higher?

Image source: Getty Images.

Why have investors been willing to pay so much for Eli Lilly stock?

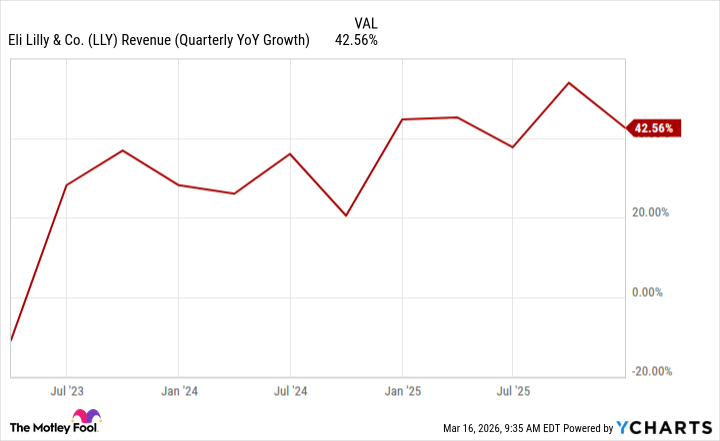

Investors have become extremely bullish on Eli Lilly in recent years due to its incredible growth potential. The company has been delivering fantastic results, as is evident in the chart below, which shows a sharp acceleration in its growth rate compared to where it was just a few years ago.

LLY Revenue (Quarterly YoY Growth) data by YCharts

The company plans to launch a GLP-1 weight loss pill this year, which could give it yet another fast-growing product to add to its portfolio. With such excitement and optimism, it’s not much of a mystery as to why this is the most valuable healthcare company in the world, and why investors remain bullish. According to the consensus analyst price target of around $1,230, Eli Lilly’s stock could still rise by around 24% from where it is today.

Today’s Change

(0.21%) $2.12

Current Price

$987.20

Key Data Points

Market Cap

$929B

Day’s Range

$975.80 – $998.17

52wk Range

$623.78 – $1133.95

Volume

49K

Avg Vol

3.1M

Gross Margin

83.04%

Dividend Yield

0.63%

Eli Lilly’s stock isn’t cheap, and that adds risk for investors

In just five years, Eli Lilly’s stock has skyrocketed by more than 400%, and today, it trades at more than 40 times its trailing earnings. For some investors, that might seem like an appropriate multiple to be paying for the business given its fantastic growth story and the potential it still possesses to get even bigger in the years ahead.

The problem, however, is that it also assumes a best-case scenario for the company and that it will continue to dominate the GLP-1 space. The reality, however, is that there will be more competition in the future, and other healthcare companies may chip away at its market share over time. Paying such a high price gives investors little to no margin of safety should those problems arise.

Eli Lilly still looks like a good long-term buy, but there could be some volatility in the short term, particularly due to its high valuation; the stock is down around 8% this year.