Commercial-real-estate debt is in a squeeze. Rates hover near decade highs, and every basis point stings. Basel III “endgame” rules now force large banks to hold 19 percent more capital against CRE loans, so many lenders are trimming commitments or quoting uneconomical spreads.

Small businesses feel it, too. The SBA’s 7(a) program closed FY 2024 with a $397 million deficit, resetting guaranty fees for 2026 deals.

Enter online marketplaces. One digital package pings dozens of lenders and returns quotes in minutes instead of weeks.

This guide ranks the top U.S. platforms, two data tools, and one cross-border option so you can fund your next project fast.

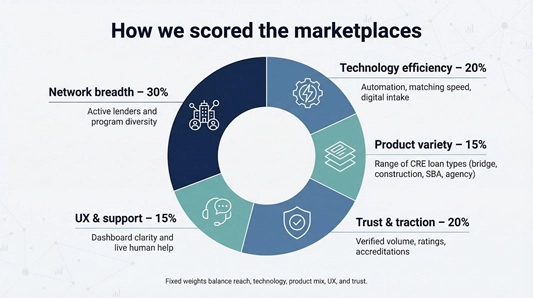

Methodology: How we scored the marketplaces

Transparency matters. You deserve to know exactly how we separated the hard-working platforms from the flashy also-rans.

We built a decision matrix, a scorecard based on what lenders, brokers, and borrowers say they value most: network reach, speed, product choice, support, and trust. Each factor has a fixed weight, so no single metric can skew the outcome.

Network breadth leads at 30 percent. A larger lender pool sparks competition and sharper terms for you.

Technology-driven efficiency carries 20 percent. Automated intake, real-time matching, and instant term sheets save days.

Product variety earns 15 percent. Platforms limited to agency debt trail those that handle bridge, construction, and SBA loans in one place.

User experience and live support split another 15 percent. A clear dashboard is nice; a quick human answer when underwriting questions surface is better.

The final 20 percent goes to trust and traction. We credit verified volume, public ratings, and independent accreditations where available.

Any platform missing data for three or more inputs fails our inclusion test. That rule trimmed a handful of niche sites before scoring started.

The outcome is a ranked Core-5 list you can use now, plus specialty picks for narrower needs. Simple, fair, and repeatable.

LoanBase: rank #1, scale meets speed

LoanBase tops our scoreboard for one reason: reach. The platform lists more than 7,500 active lenders across banks, credit unions, debt funds, and agency desks. That breadth turns a single upload into a nationwide bidding contest, giving you immediate pricing power.

LoanBase commercial real estate loan marketplace dashboard screenshot

LoanBase commercial real estate loan marketplace dashboard screenshot

What good is reach without speed? LoanBase’s matching engine returns preliminary quotes in as little as 24 hours, compressing weeks of calls into a single business day. We’ve watched borrowers upload on Monday morning and field three lender follow-ups before lunch Tuesday.

Technology drives the pace. After you finish a guided intake, the system sorts lenders by property type, geography, and loan size, then pushes your deal to the right subset with one click. You watch responses land in a clean dashboard instead of juggling email threads.

Loan types cover the stack: bridge and construction debt for ground-ups, conventional mortgages for stabilized assets, plus agency and SBA options when fixed rates matter most. That mix delivered a perfect score in our product-variety column.

Support feels human, not robotic. You get a named success manager who can nudge lenders for clarifications and walk you through a term sheet when legal language gets dense.

If you want the widest lender exposure and you want it fast, LoanBase is the marketplace to beat.

FinanceLobby: rank #2, a broker’s lead-gen machine

FinanceLobby caters to brokers who juggle multiple deals. Open the dashboard and the focus is clear: filters for debt yield, exit caps, and sponsor experience sit up front, helping you match complex multifamily or value-add profiles without a cold call.

FinanceLobby broker-focused CRE loan marketplace interface screenshot

Scale attracts users. The marketplace lists more than 1,000 actively quoting lenders, and its broader directory tops 4,000 when you include regional banks and specialty funds. A broker can market a 200-unit repositioning in Dallas and still shop a medical office refinance the same afternoon.

Speed follows scale. After you post a deal, FinanceLobby’s AI sorts the lender stack by terms, duration, and asset class. Soft quotes land in under 48 hours, maintaining momentum while you gather updated rent rolls.

Throughput builds trust. About 400 loans close on the platform every 30 days, proof that lenders are not window-shopping. An internal chat thread lets both sides address questions quickly and shortens the traditional blast-and-chase cycle.

If you thrive on steady deal flow and measure success by the reach of your lender list, FinanceLobby earns a spot on your home screen. It flips outbound dialing into inbound offers so you can focus on structuring.

CommLoan: rank #3, precision for multifamily deals

CommLoan feels like a custom-built shop for apartment lenders. Its AI engine, CUPID, reviews your rent roll and underwriting asks, then matches the file to a curated roster of about 900 banks, credit unions, and agency desks. You receive a short list of lenders already comfortable with your debt-yield math, so you avoid spraying deals into the void.

Turnaround impresses. Brokers report term sheets within hours, and CommLoan says the tool triples pull-through rates because only prequalified lenders see the package. That efficiency shines when you are juggling several refinances and have no patience for rewriting the same narrative five times.

Product depth starts with multifamily but now stretches to office, retail, and industrial, plus bridge and construction notes. Agency programs from Fannie, Freddie, and HUD sit in the same carousel, letting you toggle between fixed and floating quotes without leaving the dashboard.

Customer service scores well. An NPS in the mid-70s shows users come back, and the platform charges no subscription or posting fees; revenue comes from lenders, not borrowers. If you need fast certainty of execution on apartment assets, CommLoan provides a tightly engineered runway from quote to close.

Lendio: rank #4, small-business roots, CRE reach

Lendio built its name on SBA working-capital loans, so some investors overlook the real-estate channel. That is a miss. Today the marketplace routes commercial mortgage requests to more than seventy-five banks, credit unions, and non-bank lenders focused on owner-user or smaller investment properties.

The entry point is simple. A five-minute questionnaire collects the basics—property type, value, desired loan amount—then a soft credit pull sets the risk baseline. Lendio’s algorithm sends your deal to lenders that already price in your geography and ticket size.

Loan choices include conventional mortgages, SBA 504 and 7(a), bridge notes, and construction lines. Typical checks run from two-hundred-fifty thousand to five million dollars, a sweet spot for first-time or growing sponsors that do not need Wall Street size.

Funding averages four to eight weeks, faster than a hometown bank yet long enough for full appraisals and environmental due diligence. The platform’s CRE loan guide lists starting rates around 6.25 percent and breaks down required credit scores, down payments, and amortization schedules so you can learn more about your options.

Customer reviews back the experience. A 4.5 Trustpilot score and an A-plus BBB grade show consistent support from application to close.

If your next project is a three-million-dollar warehouse condo and you want to test both SBA and conventional lanes without paying a broker retainer, Lendio offers high convenience with low form fatigue.

StackSource: rank #5, data transparency for the detail-oriented

StackSource earns a top-five spot by treating market data as a product, not an afterthought. Open the platform and you see daily dashboards that track cap rates, lender spreads, and recent closings in your submarket. Live benchmarks help you spot outlier quotes before investing time in diligence.

The lender side stays partly opaque; StackSource vets every participant but does not publish a headline count. What we do know is that response quality beats raw volume. Lenders receive only deals that match their program filters, so you avoid ghosting from funds that never planned to bid.

Submitting a request feels like filling out a Bloomberg template. You enter property type, loan size, DSCR target, and exit horizon. The system then maps likely appetite so you can adjust the capital stack before you click send.

Because analysts and principals share the same view, conversations stay rooted in the numbers. If you enjoy digging into comps and want transparency built into the workflow, StackSource is worth your time, even if it trades breadth for depth.

Specialty segment: research-first tools

Not every capital hunt begins with “who will lend.” Sometimes you need to see who has already lent, on what terms, and where gaps remain before you build a pitch deck. Two platforms excel at that work.

Capitalize.io acts as both search engine and deal radar. Enter a street address or lender name and the database returns historical mortgages, maturity dates, and contact details. That insight lets you call a bank the month its last note rolls off, or reach an owner whose bridge debt balloons next quarter. With 100,000 lender profiles and more than 12 million recorded mortgages, the platform turns public filings into a living playbook.

RealAtom solves a different pain point: workflow. It functions like Salesforce for debt placement. Upload your package once and track every lender interaction, document request, and redline through closing. The reward is auditability. When a partner asks, “Who still needs to comment on the environmental report?” the answer is one click away.

RealAtom commercial real estate debt workflow platform screenshot

Neither site issues term sheets like the marketplaces we ranked earlier, so we do not grade them on network breadth or speed. Instead, we highlight them for what they are, focused tools that sharpen your strategy before the marketplace sprint.

International option: FinLoop for cross-border capital

U.S. balance sheets do not always tell the whole story. Maybe your syndicate owns assets in Berlin, or a Dutch investor wants to finance a Miami purchase with euro-based debt. FinLoop fits those situations.

Headquartered in Germany, the marketplace aggregates more than 4,500 European lenders, including universal banks, insurance portfolios, and private debt funds. Coverage spans senior, mezzanine, and construction loans from 500,000 to 200 million euros, squarely in institutional territory.

FinLoop European cross-border CRE lending marketplace screenshot

FinLoop European cross-border CRE lending marketplace screenshot

The workflow mirrors domestic marketplaces: digital intake, lender matching, and a document room for diligence. One big twist is cost. FinLoop charges borrowers no success fees; lenders pay an enterprise SaaS license instead, keeping basis points free for legal and hedging costs.

Funding cadence is quick by continental standards. Marketing rounds close in about three weeks, and fully underwritten term sheets often arrive before week four. A bilateral reach-out to five European banks can take twice as long just to confirm appetite.

If your CRE strategy crosses the Atlantic, FinLoop delivers a ready lender universe and preserves precious euros for closing friction.

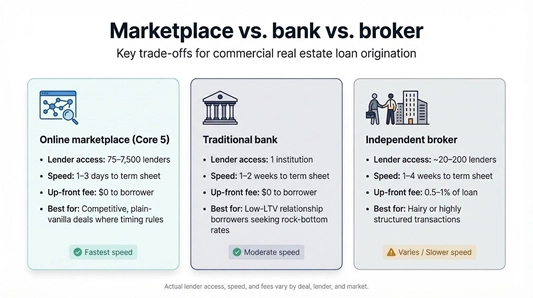

Marketplace vs. bank vs. broker: where each channel wins

Choice is power, but only if you understand the trade-offs.

Traditional banks still offer the lowest fixed rates, especially when you keep deposits with them. The catch? Credit committees meet weekly, and Basel rules force banks to cap loan-to-value or sidestep hair-on-fire asset classes such as suburban office.

Independent mortgage brokers excel when a deal needs story telling, like a busted condo conversion or land without income. Their Rolodex and negotiation skill can unlock a quirky file, but success fees and longer timelines add cost.

Online marketplaces sit in the middle. They pair data with automation to surface a wider lender pool in hours, not weeks, and most charge borrowers nothing. You swap the white-glove service of a full-service broker for speed and transparency.

Here is a quick scorecard that highlights the differences:

|

Channel

|

Lender access

|

Typical speed to term sheet

|

Up-front fee to borrower

|

Best for

|

|

Online marketplace (Core 5)

|

75–7,500 lenders

|

1–3 days

|

$0

|

Competitive, plain-vanilla deals where timing rules

|

|

Traditional bank

|

1 institution

|

1–2 weeks

|

$0

|

Low-LTV, relationship borrowers seeking rock-bottom rates

|

|

Independent broker

|

20–200 lenders

|

1–4 weeks

|

0.5–1 percent of loan

|

Hairy or highly structured transactions

|

FAQ introduction

Commercial real estate borrowers often have recurring questions about online loan marketplaces, from eligibility requirements to typical fees. Future updates will address these in detail.

Conclusion

If your capital stack is straightforward and the clock is ticking, marketplaces win on speed and lender diversity. Keep a trusted banker for deposit-anchored loans, and call a specialist broker when your project needs narrative finesse.