One number suggests you’re not too late to buy.

Amid all the volatility silver prices have seen in 2026, they are still up by double digits for the year as of early February. Shares of Wheaton Precious Metals (WPM +3.88%) are up 11.4% year to date, and zooming out over the last 12 months, they have returned 98%.

Looking at the precious metals company’s rise, it’s natural to wonder if its rally is over. The stock’s price-to-earnings (P/E) ratio of 59 certainly makes it look expensive at first glance, considering that the average S&P 500 company is priced far more cheaply with a P/E ratio of 29.6. ‘

Yet there’s one good reason to think that this stock is actually much cheaper than it appears. Not only that, it’s even cheaper than it was a year ago, before its near-100% rally.

Today’s Change

(3.88%) $5.08

Current Price

$135.98

Key Data Points

Market Cap

$62B

Day’s Range

$133.01 – $137.33

52wk Range

$66.44 – $160.36

Volume

2M

Avg Vol

2.1M

Gross Margin

68.52%

Dividend Yield

0.49%

Putting Wheaton Precious Metals’ valuation in context

To understand this company’s valuation, you need to know its business model. Wheaton Precious Metals doesn’t mine silver, gold, or any other metal. Instead, it provides financing for mining projects in return for the right to buy portions of the mines’ future output at heavily discounted prices.

Image source: Getty Images.

For instance, the company’s 2023 deal with Waterton Copper entitles it to buy hundreds of thousands of ounces of silver from the latter’s Mineral Park Mine in Arizona for a whopping 82% discount to spot price in return for $300 million in up-front financing. As another example, it bought the right to buy up to 18 million ounces of future silver production from the Blackwater mine in Cariboo, Canada, at an 82% discount to spot price, all for $141 million in financing that would be paid gradually, in tranches.

Obviously, a company that has rights to buy troves of gold and silver from mines around the world at discounts of up to 82% will be able to dramatically outperform precious metals’ returns over time. It’s no surprise, then, that as of early 2026, Wheaton Precious Metals shares had outperformed both gold and silver over one-year, three-year, five-year, and 10-year periods, often dramatically.

With the advantages of its business model, then, it makes sense that investors would be willing to pay a premium for shares amid a historic precious metals rally. But how big of a premium is justified? The P/E ratio offers a clue, but because it only takes current earnings into account, it’s only a snapshot in time.

To get a more complete picture, I look at the company’s price-to-earnings-growth (PEG) ratio. Calculated by dividing the P/E ratio by the rate of growth in earnings per share, it offers insight into whether earnings are growing fast enough to justify buying a stock that looks expensive based on its P/E ratio alone.

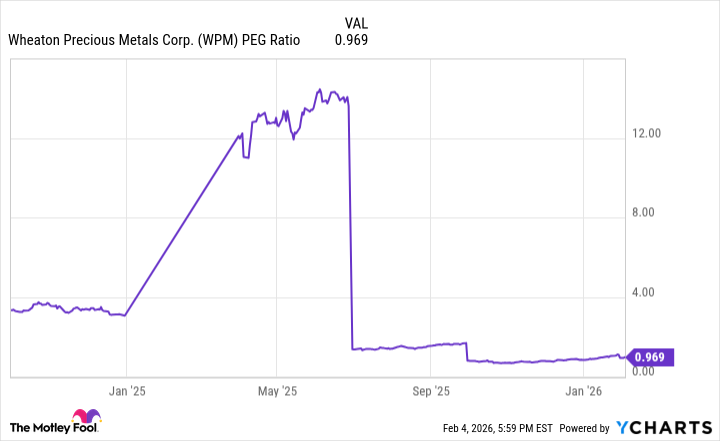

Over the last 12 months, here’s how the stock’s PEG ratio has trended.

Data by YCharts.

As you can see, the PEG ratio plummeted in mid-2025, when the company announced that Q2 net income had more than doubled from a year ago. While shares rallied on the news, they didn’t soar 100%, making the stock much cheaper by this metric.

Today, the PEG ratio is below 1, putting it right at the threshold of what’s considered desirable. The question of whether to buy shares likely comes down to which direction you believe gold and silver are headed. While anything can happen, there are three reasons to think that silver, incredibly, may have still more upside in 2026 and beyond.