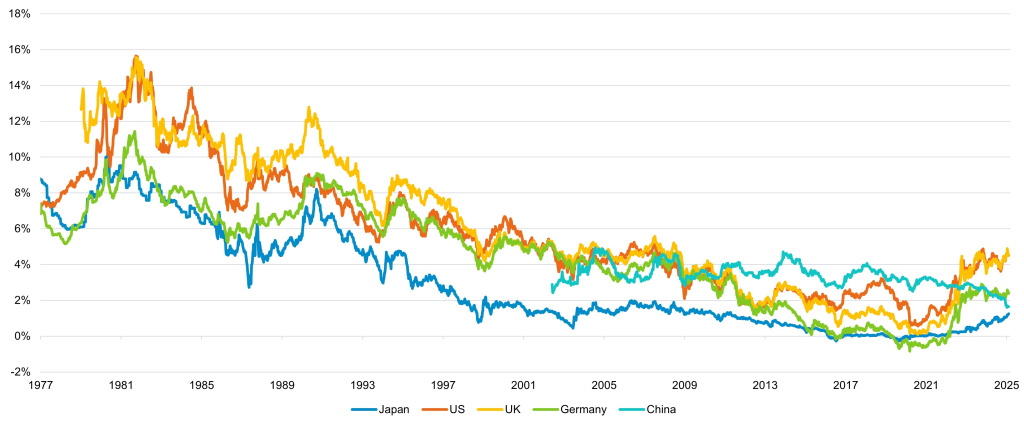

For my entire 20+ year career, Japanese government bond (JGB) yields have widely been considered as the global government bond yield anchor.

For my entire 20+ year career, Japanese government bond (JGB) yields have widely been considered as the global government bond yield anchor.

But the fact that Japan now appears to be emerging from decades-long disinflation could upset this balance and be another factor that pushes global bond yields structurally higher, alongside de-globalisation and rising tariffs.

Government bond investors have already suffered several years of negative returns. However, they should not get too disheartened. The perceived Japanification of China’s economy could mean that Chinese government bonds replace JGBs as the anchor for global yields.

Ever since Japan’s economic bubble burst in the early 90s, the country’s anaemic growth and inflation reliably placed Japanese government bond yields below those of other developed market government bonds.

Despite repeat government efforts to end the stagnation, growth never returned. The Bank of Japan (BOJ) kept loosening monetary policy, even to the point of setting negative policy rates, and JGB yields kept falling.

‘Japanification’ entered the lexicon to describe a deflationary spiral caused by weak demand and an ageing population.

Betting that economic growth would re-emerge and interest rates would rise by shorting JGBs became such a famous quixotic trade that it was bestowed its own grim moniker – the widow-maker.

Japanese yields lead the way down

10y yields

JGBs have served as the anchor of global government yields for as long as most investors can remember, with the BOJ reliably the least likely major central bank to deliver a hawkish surprise.

There was always the faint concern that if JGB yields were to rise significantly, investor psychology and the pressure to keep interest rate differentials constant could trigger a ripple effect, leading to higher government yields globally. But the BOJ would never actually raise rates, would they?

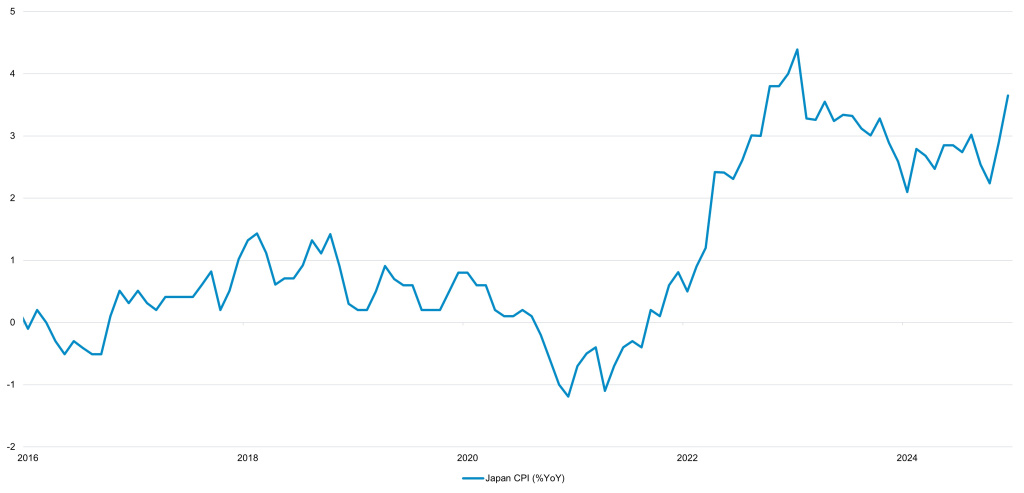

Now, recent developments in Japan’s inflation dynamics suggest that the BOJ is finally able to plot a path to normalising interest rates.

Slowly but surely, after years of battling deflation, the trajectory of inflation in Japan has turned upwards. As inflation begins to take hold, the implications for Japanese monetary policy, JGBs, and, by extension, global government yields, could be profound.

BOJ set to gradually raise rates as inflation returns

This change has already started. In August 2024, the BOJ surprised markets by adopting a more hawkish stance than expected in response to greater inflationary pressures.

But instead of causing global yields to rise, as financial theory might predict, they fell.

Hawkish BOJ led to counterintuitive yield fall in august

However, we believe that this reaction was in fact an anomaly rather than a sign of things to come. The BOJ’s surprise precipitated a negative shock for markets, causing carry trades to unwind and equity market sell-offs that led to a flight to the safety of government bonds.

This was exacerbated by a cocktail of negative news at the time including weakening US data and the conflict in the Middle East deteriorating.

Inflation dynamics in Japan mean that the BOJ will continue to gradually raise rates. The next time it delivers a hawkish surprise, we believe that JGB yields are likely to move higher.

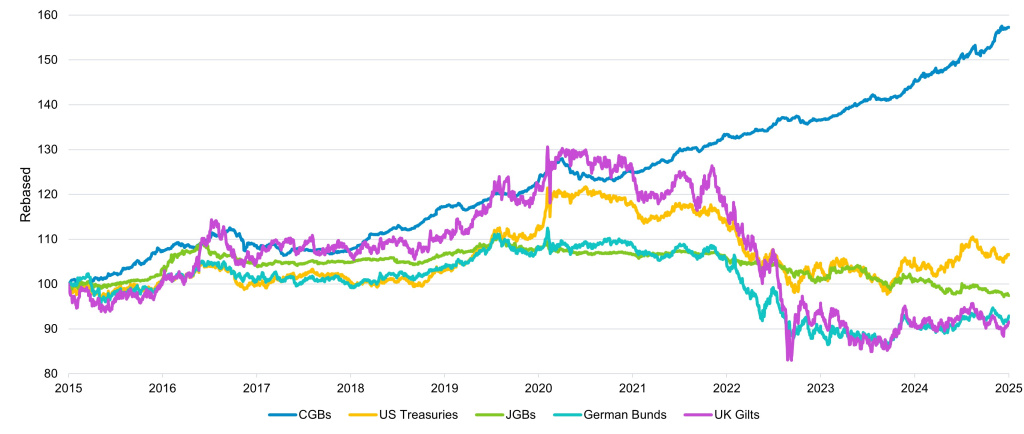

However, we do not necessarily think this will cause all government bond yields to follow suit. If JGBs do lose their status as the global rates anchor, we believe that Chinese government bonds (CGBs) could step in to replace them.

Over the past five years, CGBs have emerged as one of the best-performing and least volatile bond markets. China’s disinflationary trends, driven by structural economic factors, have created a supportive environment for its bond market.

Additionally, the ownership structure of CGBs, with a significant portion held domestically, mirrors that of JGBs. This provides a buffer against external shocks and adds to market stability.

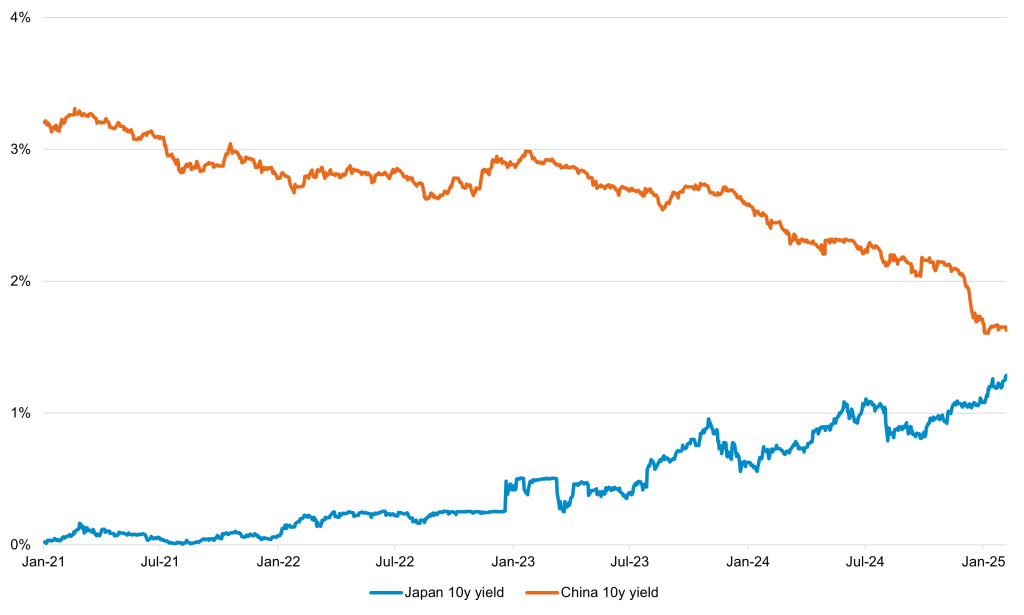

The similarities between Japan and China extend beyond bond market dynamics. China’s economy has stalled in the last few years as a result of numerous structural reforms, most notably the deleveraging of the property sector.

Furthermore, demographic trends in China reveal a rapidly ageing society. China is routinely touted as the next region to succumb to ‘Japanification’.

CGBs have offered stability in recent years

All this suggests that CGBs could potentially take over from JGBs as the global rates anchor. Major government bond yields are much higher now than they have been for much of the past decade – a boon for income investors who were forced to move down the quality scale in search for yield in the years before the pandemic.

However, the worry that higher JGB yields could cause all bond yields to rise has left many investors hesitant to invest too heavily in government bonds.

However, despite some differences, we believe that there are enough similarities between the two to assume that CGBs will indeed exert a downward pull on global bond yields in future in the same way JGBs have done for much of the past three decades.

Passing the baton?

The global bond market is at a crossroads. There are several valid reasons at present why investors might think twice about allocating to government bonds, including the potential that the new US administration’s fiscal and trade policies will be inflationary and the fact that bonds offer less diversification benefits now that equity-bond correlations have become more positive.

Some might consider the potential that JGBs will no longer act as a global-rates-anchor as another reason to be cautious. However, we believe investors should not be too worried that Japan’s inflation dynamics will in turn lead to higher global government bond yields.

CGBs, with their strong performance and structural similarities to JGBs, could take up the mantle of the global yield anchor. The evolving economic landscapes of Japan and China could therefore play a crucial role in shaping the future of global government bond markets.

We have not been alarmed by the rise in JGB yields, which has allowed us to stick to our existing approach in the global multi-asset growth and income strategy of being tactical and dynamic with our government bond positioning.

In practice, this has involved taking advantage of the recent duration sell-off that lasted until mid-January 2025, bringing the duration of our portfolio to an all-time high of 3.4 years, and then aggressively selling duration when government bonds subsequently rallied. This has helped us deliver stellar returns so far in 2025.

George Efstathopoulos is multi-asset portfolio manager at Fidelity International