The United States’ decision to tighten restrictions again on Russian seaborne oil may seem like another chapter in the sanctions battle over the Ukraine war. But beneath the headlines lies a much larger story — one that directly affects India and much of the developing world.

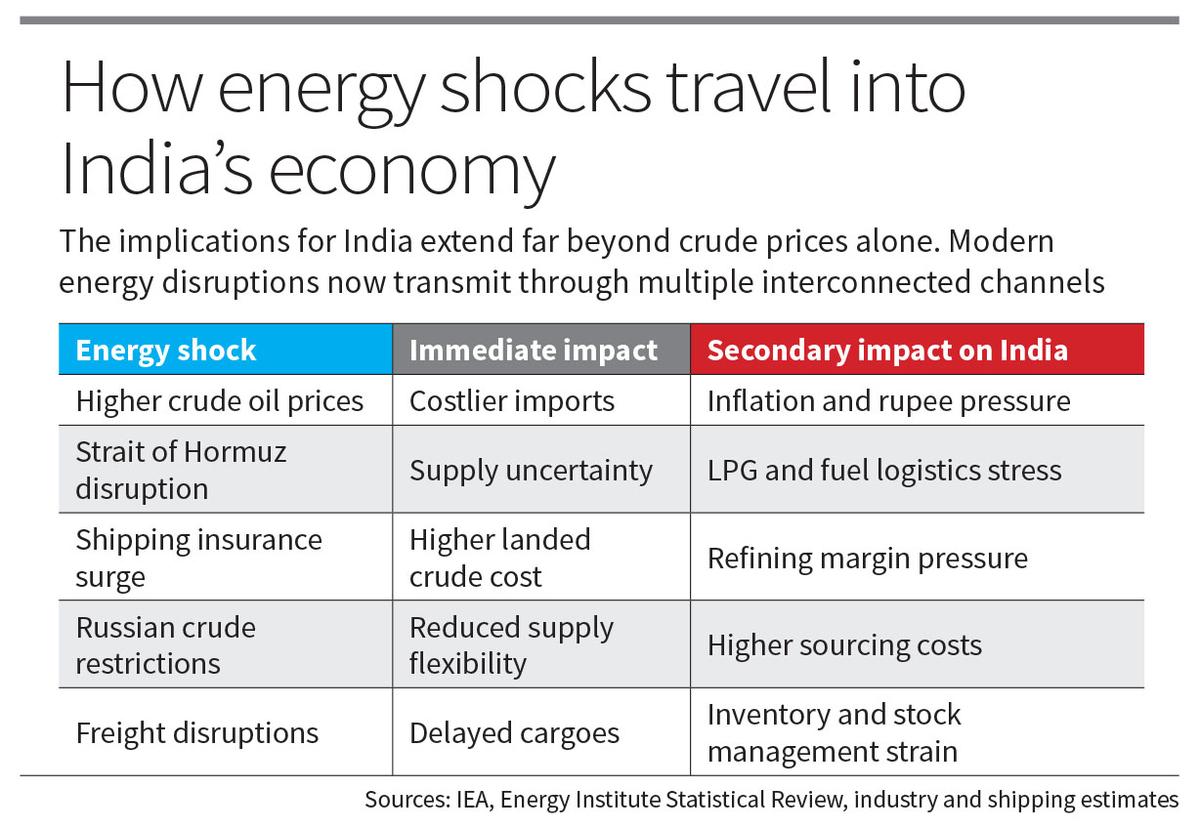

The issue is no longer just Russia. It is whether the global energy system can withstand simultaneous geopolitical shocks without causing prolonged inflation, supply insecurity and economic instability across Asia. For over three years, the world has attempted an unprecedented balancing act: keeping one of the largest oil exporters under heavy sanctions while trying to maintain stable energy prices. That balancing act is becoming increasingly fragile. The latest restrictions come at a sensitive moment. Oil markets are already unsettled by conflict in West Asia, persistent disruptions in maritime trade routes and growing concerns over the Strait of Hormuz, the world’s most critical oil transit chokepoint. In such conditions, even policy signals from Washington can alter freight rates, insurance premiums and crude price expectations almost overnight.

Why India cannot ignore this development

India imports nearly 90% of its crude oil and is the world’s third-largest importer as well as one of the fastest-growing energy consumers. Unlike many developed economies, where energy demand has plateaued, India’s energy needs will keep rising with industrialisation, urbanisation and expanding mobility. It is this reality that shapes India’s energy choices.

When Russian crude began flowing into India in large volumes after 2022, many in the West viewed it through a geopolitical lens. India saw it as an economic stabiliser during a period of extreme volatility. Russian oil helped moderate inflationary pressures, improved refinery economics and reduced dependence on any single region. It provided supply flexibility at a time of great turbulence in global energy markets. Critics often frame the debate as morality versus commerce. But energy-importing countries rarely have that luxury.

For countries such as India, energy affordability directly affects transport costs, food inflation, fertilizer subsidies, manufacturing competitiveness and household spending. A sustained rise in crude prices quickly spreads through the wider economy.

When sanctions meet market reality

Global oil markets are operating with little room for psychological comfort. The world has already seen disruptions in the Red Sea, attacks on shipping infrastructure, growing military tensions involving Iran, tighter tanker availability and sharply higher war-risk insurance premiums. In such conditions, constraining one of the world’s largest oil suppliers inevitably unsettles markets, even if physical supply losses remain limited at first.

Oil markets react not only to shortages but also to the fear of shortages. That fear alone can drive prices sharply higher. Ironically, this exposes a contradiction at the heart of the western sanctions policy.

The U.S. and Europe want to reduce Russia’s oil revenues. But they also want lower inflation, stable fuel prices and uninterrupted global energy flows. Increasingly, these objectives are colliding with each other. The harder sanctions become, the greater the risk of tightening global supply balances. Once oil prices rise sufficiently, Russia can continue earning substantial revenues despite lower export volumes. In some cases, higher global prices can partially offset the impact of sanctions themselves. This explains why the sanctions policy has repeatedly oscillated between aggressive rhetoric and tactical flexibility. Markets eventually force pragmatism.

The temporary waivers and carve-outs of recent years were not merely signs of policy inconsistency; they reflected energy-market realities. The uncomfortable truth is that the modern global economy still runs overwhelmingly on hydrocarbons. Despite the rapid growth of renewables, oil remains central to transport, aviation, petrochemicals, agriculture and global trade logistics. The world may speak of transition, but it still functions on molecules.

For India, the challenge is even more complex. The Strait of Hormuz remains a major strategic vulnerability, carrying nearly one-fifth of global oil trade. A large share of India’s crude oil and LPG imports transits through these waters. Any escalation in the region could disrupt supplies, raise shipping costs and delay deliveries. This is why Russian crude evolved into something larger than a discounted barrel for Asia. It emerged as a diversification mechanism during a period of growing uncertainty in West Asia.

The larger lesson from these developments is that energy security itself is changing shape. In earlier decades, countries were concerned mainly with access to physical supply. Today, vulnerabilities are far more complex. Energy flows can now be disrupted by shipping restrictions, insurance controls, financial sanctions, tanker blacklisting, payment barriers and maritime security risks. In effect, global energy has become deeply entangled with financial and geopolitical architecture.

India’s long-term energy strategy

This changing landscape has major implications for India’s long-term strategy. India cannot rely indefinitely on opportunistic crude sourcing during crises. The country needs a broader and more resilient energy framework. That means expanding strategic petroleum reserves, diversifying crude sourcing regions, strengthening domestic exploration, improving refining flexibility, accelerating gas infrastructure, expanding alternative energy pathways and reducing dependence on vulnerable maritime chokepoints. At the same time, India will need to preserve strategic autonomy in energy decision-making.

The emerging global order is becoming increasingly fragmented. Energy trade is no longer governed purely by economics; it is increasingly shaped by sanctions regimes, strategic rivalries and competing geopolitical blocs. For major importing countries, excessive dependence on any single geopolitical camp carries long-term risks. India’s approach therefore reflects not neutrality, but realism.

The years ahead are likely to witness repeated tensions between geopolitical objectives and energy-market stability. The world is entering an era in which sanctions, wars, maritime insecurity and supply-chain disruptions may become recurring features rather than temporary exceptions. That makes resilience more important than ideology. In the end, energy systems obey physical realities, not political slogans. Tankers must still move. Refineries must still operate. Economies must still function. Nations that fail to build diversified and resilient energy systems may discover that, in the 21st century, economic sovereignty increasingly depends on the ability to navigate a fragmented and unstable energy world.

Shrikant Madhav Vaidya is former Chairman of IndianOil Corporation Ltd. and an energy strategist

Published – May 25, 2026 12:40 am IST