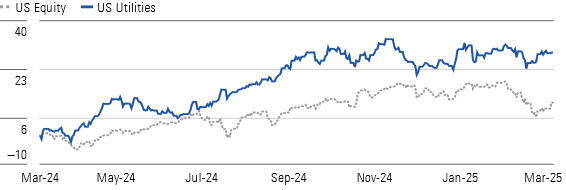

Utilities have outperformed in the year to date as cautious investors seek stability. The Morningstar US Utilities Index is up 4.31% in the quarter, significantly outperforming the broader market and making it the third-best-performing sector behind energy and healthcare. This is a rebound from the fourth quarter, when utilities lost the momentum they built throughout 2024.

Even if utilities continue to outpace the market, we think investors should be prepared for absolute returns well below the 26% they posted in 2024. Even with the big swings in performance over the past three years, these stocks’ annualized return is 8% over that period—the same as the sector’s 40-year average annual return and in line with what we think investors should expect.

Utilities’ strength in the first quarter has left valuations elevated. We consider the sector 8% overvalued after starting the year fairly valued. Utilities’ median 22 P/E ratio is well above the 20-year average. We think this is excessive despite the sector’s better growth prospects and stronger balance sheets than what was seen in past decades.

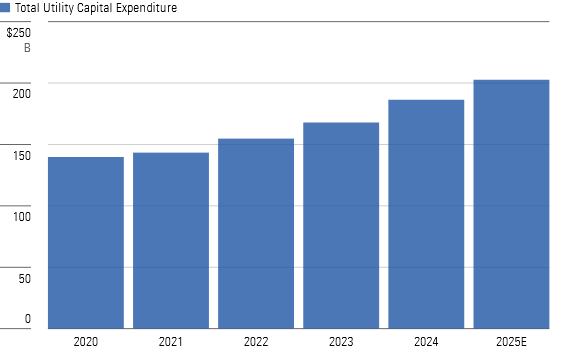

Many utilities have increased their capital investment plans and are entering their largest growth cycles in decades. Realizing this growth will depend on overcoming constraints such as regulatory approvals, supply chain shortages, and construction timelines. Utilities that are successful should be able to increase their dividends and justify their valuations.

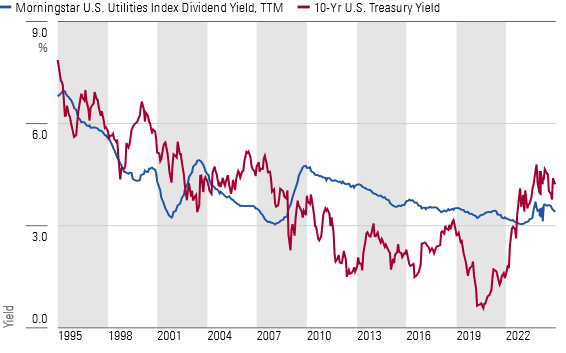

The relationship between interest rates and utilities’ dividend yields has flipped in the past two years. Utilities’ dividend yields are at the largest discount to 10-year US Treasury yields since before the 2008 financial crisis. Historically, this is a bearish signal. However, utilities’ strong underlying fundamentals, such as energy demand growth, capital investment opportunities, healthy balance sheets, and sectorwide dividend increases, could mean the yield discount will persist.

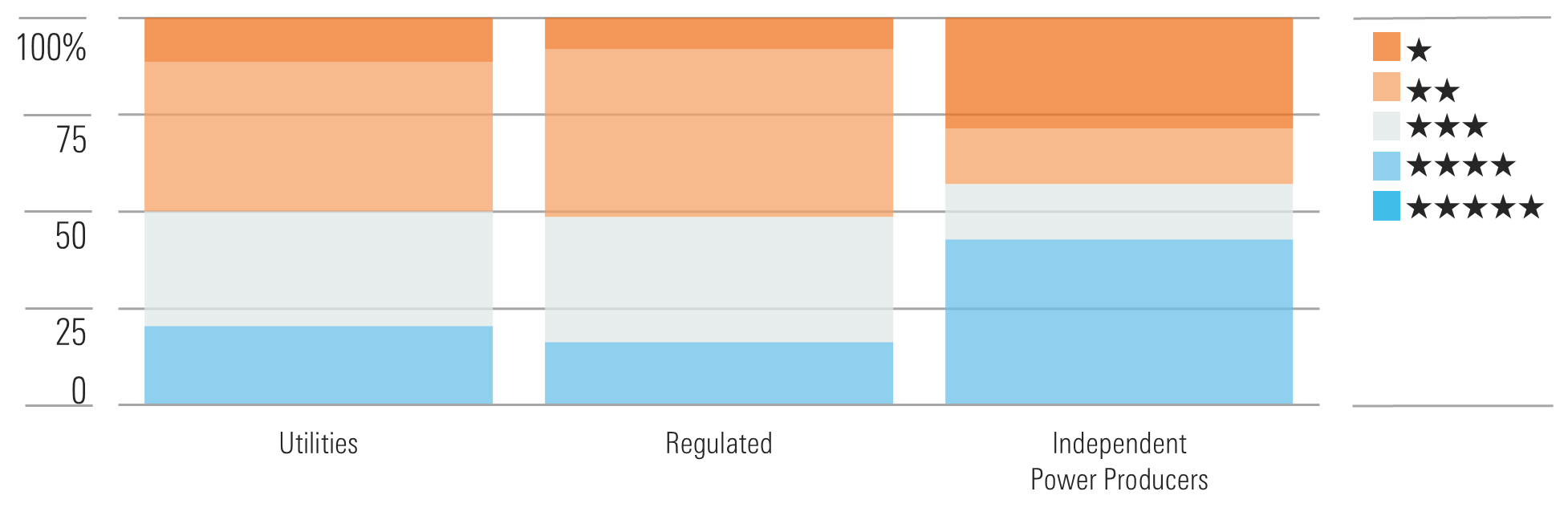

Top Utilities Sector Picks

Duke Energy

Duke Energy DUK has a clear pathway to achieving the high end of management’s 5%-7% annual earnings growth target. Duke’s $83 billion capital investment plan for 2025-29 is focused on clean energy, infrastructure upgrades, and increasing electricity demand. Legislation in North Carolina supports Duke’s investment in the region with above-average returns. Highly constructive Florida offers opportunities for significant solar growth. Duke’s dividend yield is above the sector median, but dividend growth will lag earnings growth until the company’s payout ratio comes down.

Eversource Energy

We think Eversource Energy ES is too cheap for investors to ignore. Eversource will miss out on most of the data center growth excitement, given its Northeast service territory. However, it has plenty of investment opportunities to keep earnings growing at 6% annually, at least through 2028. We think the market is ignoring this growth. Eversource has mostly eliminated its offshore wind exposure and will derive all its earnings from its rate-regulated utilities in 2025. We think the firm can offset regulatory challenges in Connecticut by adding projects in Massachusetts, where regulation is more constructive. A turnaround in Connecticut regulation presents additional earnings and valuation upside.

Evergy

Although the market seems concerned about Evergy’s EVRG growth prospects, we forecast 6% annual earnings growth, in line with most other utilities. Management recently raised its five-year investment budget by 29%, and we think it could go higher, based on electricity demand growth in the Midwest and power generation needs. Alphabet, Meta Platforms, and Panasonic have announced large development plans in Evergy’s service territory. Positive legislative and regulatory developments also could boost earnings and dividend growth.