Nvidia (NVDA +0.90%) is the most valuable company in the world, and there’s little wonder why that is when you see its financials. Demand for its artificial intelligence (AI) chips is through the roof, and those chips are expensive, enabling the company to grow its business at a high rate while also generating fantastic profit margins along the way.

According to analysts at Grand View Research, the AI market will continue to grow at a compounded annual growth rate of 30.6% until 2033, as businesses continue to invest heavily into all things AI-related. It puts Nvidia in an excellent position to continue growing at a fast rate.

Nvidia already became the first company to reach a $5 trillion valuation when it did so last year. Could it also be the first one to reach $10 trillion, perhaps, by the end of the decade?

Image source: Getty Images.

Nvidia still has much more growth ahead

A big reason to stay bullish on Nvidia is that the growth opportunities in AI remain plentiful. And as long as that’s the case, the need for cutting-edge chips will be significant, inevitably leading customers back to Nvidia and to purchasing its top-end chips.

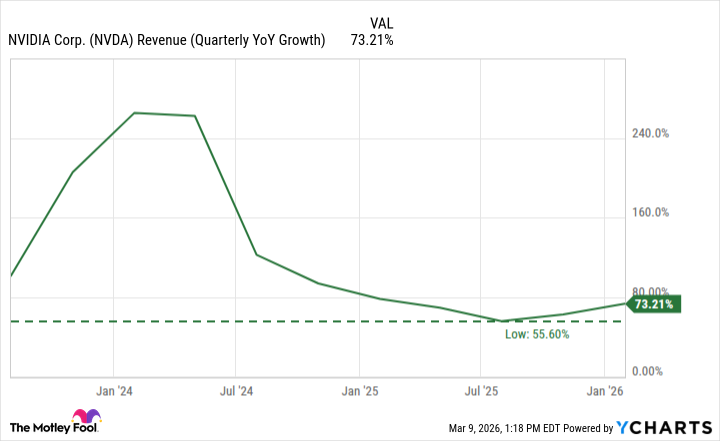

What’s remarkable about the business is that since its business took off due to the emergence of ChatGPT a few years ago and the ramp-up in AI spending, its lowest quarterly growth rate has been just under 56%.

NVDA Revenue (Quarterly YoY Growth) data by YCharts

While most companies would be thrilled with growth of around 50%, for Nvidia, it could send investors into panic mode.

Today’s Change

(0.90%) $1.67

Current Price

$186.43

Key Data Points

Market Cap

$4.5T

Day’s Range

$184.95 – $187.62

52wk Range

$86.62 – $212.19

Volume

1.8M

Avg Vol

177M

Gross Margin

71.07%

Dividend Yield

0.02%

Is a $10 trillion valuation realistic for Nvidia?

Nvidia’s valuation sits at around $4.4 trillion, which means that if it were to get to $10 trillion, it would need to more than double, and rise by close to 130%. To get there by around 2030, or four years from now, that would mean the stock would need to rise by an average of nearly 23% per year.

I think that’s a tall task given the market conditions, uncertainty, plus the fact that Nvidia already trades at 37 times its trailing earnings. It may not be egregiously expensive, but it’s not a dirt cheap stock, either. There’s also the possibility that there’s a pullback in AI spending in the coming years if economic conditions deteriorate.

Nvidia may very well reach a $10 trillion valuation due to the opportunities in AI, but I don’t think it’ll happen within the next four years. It’s still a good stock to own for the long term, but investors shouldn’t set their expectations too high given how far it has already risen in recent years and the challenges ahead.