California’s experiment in climate governance has turned the state’s oil and refining sector into one of the most politically charged energy battlegrounds in the world. A long-standing commitment to environmental targets – culminating in a planned end to oil extraction by 2045 – has collided with the realities of high demand, aging infrastructure, and a shrinking refining base. Oil output has already plunged from 760,000 b/d in 2000 to roughly 250,000 b/d in 2025, while the number of operational refineries has fallen from 20 in 2010 to just 12 today. As output falls and refineries close, the state’s reliance on imported crude and finished products deepens, pushing up prices and eroding market stability, while key suppliers such as Alaska confront a future in which their largest customer is deliberately writing them out of its long-term energy equation.

The main challenge for California’s oil sector stems from the state’s long-standing commitment to persistent environmental and carbon-reduction goals, elevated to its peak under Governor Gavin Newsom. California has long framed emissions policy as economic identity, embodied in its cap-and-trade system – among the world’s largest – capping emissions across 80–85% of the state’s industrial and energy sectors since 2013. Companies must buy or trade allowances to match their emissions, generating a carbon price that has fluctuated between $12 and $38 per ton and raising more than $25 billion for clean-energy and climate projects. Yet criticism has grown over the past decade: an oversupply of allowances and substantial free allocations – including to refineries located near disadvantaged communities – have depressed prices and limited short-term incentives to cut fossil-fuel use, particularly in transportation, the state’s largest source of emissions.

Related: Congress Reopens More of Alaska’s Arctic Refuge to Oil Leasing

The conflict escalated in 2025 when President Trump signed an executive order asserting that California’s cap-and-trade program should not stand, while simultaneously moving to expand federal oil and gas leasing on public and offshore lands, including a plan to re-authorize drilling in Pacific waters and a request for public comment on a new five-year offshore leasing program starting April 2025. Yet federal action does not automatically override the state’s authority over its own energy transition. California maintains control over onshore permitting, refinery zoning rules, its 2045 extraction phase-out, local bans such as those in Santa Barbara County, and the operation of the cap-and-trade system itself. Washington’s leverage is concentrated on federal terrain – offshore leasing, methane rules and disputes over Clean Air Act vehicle-emission waivers – leaving a contested and unresolved regulatory landscape.

California’s official policy now targets a complete end to oil extraction by 2045 under the Newsom April 23, 2021 directive and the CARB (California Air Resources Board, the state’s chief air-quality and emissions regulator) Scoping Plan, with all new fracking permits halted as part of the state’s long-term transition away from fossil fuels. That ambition aligns with and reinforces a multi-decade decline in production driven by geology and economics. Output in August 2025 stood at just 250,000 b/d, down sharply from 760,000 b/d in 2000. Around 70% of the remaining production comes from Kern County’s Elk Hills, Midway-Sunset and Kern River fields, where operators lift very heavy crude (12–14 degrees API) from aging reservoirs already in natural decline. The Los Angeles Basin contributes about 10% of statewide output, but urban encroachment and regulatory constraints continue to shrink its footprint, while offshore Santa Barbara platforms account for roughly 5%, with most legacy units seeing reduced rates of production or already in various stages of decommissioning.

California’s geology is not entirely hostile to continued output – assessments of offshore formations indicate significant undiscovered recoverable resources in the federally administered Outer Continental Shelf. Yet access to those resources is effectively sealed. A permanent moratorium enacted in 1994 blocks new leasing in state waters, and although the federal moratorium imposed in 1982 expired in 2008, no new federal offshore lease sales have taken place since. Today, about two dozen legacy platforms continue operating in federal waters beginning three miles offshore, and about a dozen remain in state waters, but the direction is unmistakably contraction rather than expansion – a gradual wind-down period toward a full closure is in full swing under California’s 2045 extraction phaseout.

Refining is emerging as the next victim of California’s environmental policy, with closures accelerating even though demand remains high: the state still consumes 1.4–1.6 million b/d of petroleum products – 5 to 6 times what it produces. The number of operational refineries has fallen from 20 in 2010 to 12 in 2025, and processing capacity has shrunk from 1.9 million b/d in 2000 to 1.5 million b/d today.

As domestic extraction declines, crude imports have filled the gap. Alaska remains the primary seaborne supplier, delivering Alaska North Slope (ANS, 32 degrees API) crude at a stable rate of around 220,000 b/d according to Kpler data. Nearly all of Alaska’s production is destined for California – only one cargo has gone to South Korea and five to China over the last two years. Ecuador and Brazil have each provided roughly 170,000 b/d over the same period. In recent years, the most notable shift in crude inflows has come from Canada’s expansion into the Pacific Ocean. Since the 590,000 b/d Trans Mountain Expansion pipeline entered service in May 2024, flows of Canadian heavy blends to California have jumped from 30,000 b/d in 2023 to 100,000 b/d in 2025. Some cargoes initially struggled to meet the Total Acid Number (TAN) requirements for California refineries, but volumes have climbed over the past two years.

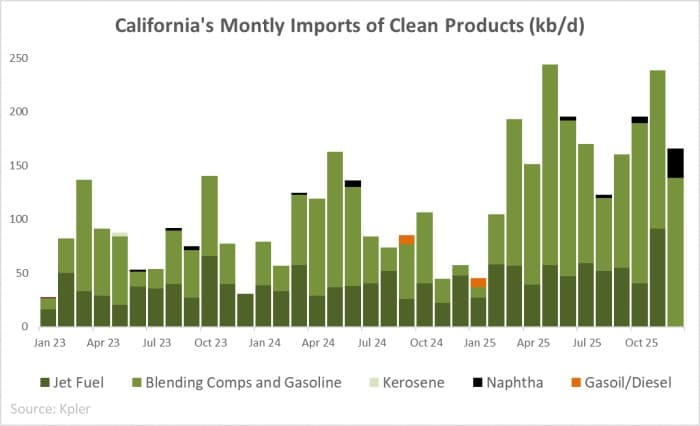

Meanwhile, product imports have escalated as refinery closures accumulate and demand remains among the highest in the country. With the Phillips 66 Los Angeles refinery (140,000 b/d) finalizing its decommissioning operations in October 2025 and Valero’s Benicia refinery (145,000 b/d) scheduled to close in April 2026, California stands to lose 285,000 b/d of capacity in a year. A major explosion and fire on October 2 at Chevron’s El Segundo refinery (responsible for roughly 20% of Southern California’s motor-fuel supply and 40% of jet fuel) exacerbated supply pressures. Jet fuel imports surged to a five-year high of 90,000 b/d in November, largely on the back of sharp increases from Japan. Gasoline imports reached record highs as well, averaging almost 50,000 b/d in 2025, sourced mainly from India, South Korea and more recently Japan.

Refined products economics reinforce these trends. California’s crack spreads are the highest across the US: gasoline prices averaged $4.5 per gallon compared with a $2.9 per gallon US average, and even sparsely populated and remote Alaska averaged $3.7 per gallon. Pricing is heavily shaped by CARBOB, California’s own gasoline formulation standard enforced by the CARB and rules that are far stricter than federal ones.

The result is a structural divergence that is already feeding into the price of fuel. As the state forces refineries offline amidst largely flat demand, imports of jet fuel and gasoline are set to keep rising, and the shrinking number of facilities capable of producing CARBOB will intensify the price pressure. With crude oil output falling, refining capacity diminishing and regulatory standards tightening, higher and more volatile fuel prices are becoming an inevitable feature of California’s market rather than an occasional shock. Crude imports may stall or fall as refining capacity contracts and domestic extraction phases out, undermining supply resilience just as the state becomes more dependent on distant sources of finished oil products.

The same shift poses an equally significant challenge for Alaska, whose crude flows have been almost entirely oriented toward California for decades. The Trump administration’s vision of Alaska as an economic “powerhouse” assumes the arrival of new crude from ConocoPhillips’ Willow project, targeting 180,000 b/d by 2029, and Santos’ Pikka, aiming for 80,000 b/d by 2026. With California gradually withdrawing as a buyer, those barrels will have to find new market outlets. Selling into Asia means longer voyages and higher costs, and previous exports to South Korea and China have been limited, while Beijing is unlikely to emerge as a reliable buyer amid deepening geopolitical and trade tensions. California – once the natural and nearest market for Alaskan crude – is signaling that the future of the North Slope barrels may unfold elsewhere, or probably not unfold at all.

By Natalia Katona for Oilprice.com

More Top Reads From Oilprice.com